Treasury Board of Canada Secretariat

www.tbs-sct.gc.ca

Common menu bar links

Breadcrumb Trail

ARCHIVED - Office of the Superintendent of Financial Institutions Canada

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

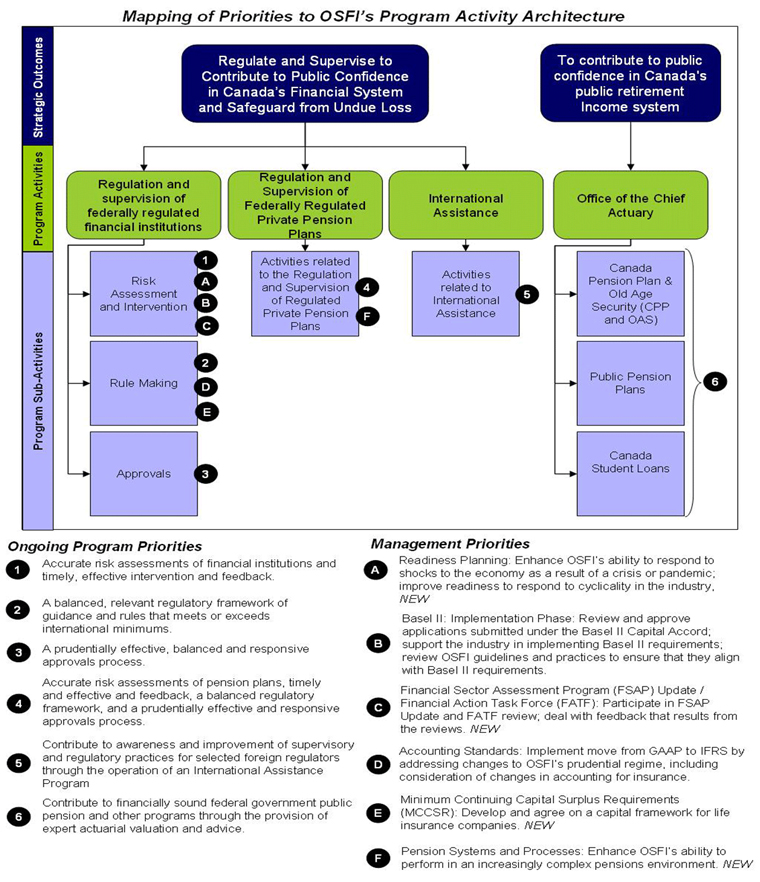

SECTION II: ANALYSIS OF PROGRAM ACTIVITIES BY STRATEGIC OUTCOME

II.1 Strategic Outcomes

Primary to OSFI's mission and central to its contribution to Canada's financial system are two strategic outcomes:

- To regulate and supervise to contribute to public confidence in Canada's financial system and safeguard from undue loss. OSFI safeguards depositors, policyholders and private pension plan members by enhancing the safety and soundness of federally regulated financial institutions and private pension plans.

- To contribute to public confidence in Canada's public retirement income system. This is achieved through the activities of the Office of the Chief Actuary, which provides accurate, timely advice on the state of various public pension plans and on the financial implications of options being considered by policy makers.

II.2 Program Activities

Three program activities support OSFI's first strategic outcome to regulate and supervise financial institutions and private pension plans so as to contribute to public confidence.

-

Regulation and supervision of federally regulated financial institutions (FRFIs)

This program activity is central to the achievement of OSFI's mandate to protect the rights and interests of depositors and policyholders and advance a regulatory framework that contributes to public confidence in the Canadian financial system. The three sub-activities of this program are:- Risk assessment and intervention includes activities to monitor and supervise financial institutions, monitor the financial and economic environment to identify emerging issues and intervene in a timely way to protect depositors and policyholders, while recognizing that all failures cannot be prevented.

- Rule making encompasses the issuance of guidance and regulations, input into federal legislation affecting financial institutions, contributions to accounting, auditing and actuarial standards, and involvement in a number of international rule-making activities.

- Approvals of certain types of actions or transactions undertaken by regulated financial institutions. This covers two distinct types of approvals: those required under the legislation applying to financial institutions and approvals for supervisory purposes.

There is a strong interrelationship among the three parts of this supervisory and regulatory program. The supervisory function relies on an appropriate framework of rules and guidance. In some situations, regulatory approval is required because a proposed transaction may significantly affect an institution's risk profile. Approving such a change involves both a supervisory and regulatory assessment. Supervisory experiences often identify areas where new or amended rules are needed.

As identified in OSFI’s mandate, OSFI must also recognize the need for financial institutions to compete effectively. The sustainability and success of regulated institutions is important for the long-term safety and soundness of the financial system. As a result, OSFI needs to strike an appropriate balance between promoting prudence and allowing financial institutions to take reasonable risks in order to compete and prosper.

- Regulation and supervision of federally regulated private pension plans

This program incorporates risk assessment, intervention, rule making and approvals related to federally regulated private pension plans under the Pension Benefits Standards Act, 1985. -

International Assistance

OSFI supports initiatives of the Government of Canada to assist emerging market economies to strengthen their regulatory and supervisory systems. This program incorporates activities related to providing help to selected countries that are building their supervisory and regulatory capacity. This program is largely funded by the Canadian International Development Agency and is carried out by OSFI directly and through its participation in the Toronto International Leadership Centre for Financial Sector Supervision. This involvement strengthens the financial system regulatory and supervisory regimes in those jurisdictions.

A fourth program activity, the Office of the Chief Actuary, supports OSFI’s second strategic outcome: to contribute to public confidence in Canada’s public retirement income system.

-

Office of the Chief Actuary (OCA)

The OCA provides a range of actuarial services, under legislation, to the Canada Pension Plan (CPP) and some federal government departments, including the provision of expert and timely advice in the form of reports tabled in Parliament. The basic elements of this program include:- Canada Pension Plan and Old Age Security: The OCA estimates long-term expenditures, revenues and current liabilities of the CPP and long-term future expenditures for Old Age Security programs. The OCA also prepares statutory triennial actuarial reports on the financial status of these programs.

- Other Public Sector Pension Plans: The OCA prepares statutory triennial actuarial reports on the financial status of federal public sector employee pension and insurance plans covering the federal Public Service, the Canadian Armed Forces, the Royal Canadian Mounted Police, the federally appointed judges and Members of Parliament.

Since 2001, the OCA also undertakes the actuarial review of the Canada Student Loans Program by evaluating the portfolio of loans and the long-term program costs.

II.3 Monitoring Mechanisms and Performance

OSFI uses various types of performance measures, including industry surveys, peer reviews and internal indicators. For each priority, the reporting is based on the types of monitoring mechanisms used.

Since 1998, OSFI has engaged in a process of periodic, anonymous, independent consultations with industry stakeholders. Generally these are comprised of senior executives and professionals representing the stakeholder group, and are subsequently referred to as “knowledgeable observers”. This provides OSFI with an indication of its performance in program areas, including whether it is providing the guidance and direction necessary to stakeholders.

OSFI's mandate explicitly provides that closures and terminations of the financial institutions it regulates can occur and are not by themselves an indication of OSFI's performance. In considering those that do occur, OSFI assesses how it performed relative to its early intervention mandate in identifying the situation and intervening appropriately.

It should be recognized that OSFI's performance does not constitute the only influence on its strategic outcomes. Indeed, OSFI's legislation recognizes that there are many other factors and stakeholders whose actions or inactions have a large impact on the strategic outcomes. OSFI monitors the external environment to help ensure it has a clear understanding of the influences on its key strategic outcomes and to gain additional insights into the ways by which OSFI itself can continue to contribute to those outcomes.

In 2007-2008, OSFI enhanced its performance measurement framework and performance measures for external reporting to Parliament, Treasury Board and other stakeholders. This framework, comprising measures, indicators, targets and reporting cycles, meets the requirements of the Treasury Board's Management Resources and Results Structure (MRRS) Policy and was embedded into OSFI's 2008-2009 Report on Plans and Priorities. OSFI is implementing, where feasible and appropriate, reporting based on the updated measures from the enhanced framework in this 2007-2008 Departmental Performance Report.

In some cases, data collection against prior measures was discontinued in order to implement OSFI's enhanced measures. In other cases, new measures were developed to support new priorities. Performance measures that are included for the first time in this report are identified as “NEW”.

II.4 Detailed Analysis of Performance

The diagram below illustrates the link between OSFI's priorities and its Program Activity Architecture.

In addition to the above Program Priorities, OSFI has Program Support Priorities which are discussed in Section IV.3.

The following tables provide an assessment of OSFI's performance for the year against its Program Priorities and Management Priorities.

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|||||||||||||

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |||||||||||||

| Program Sub-Activity: Risk Assessment and Intervention | |||||||||||||

| Priority 1: Accurate risk assessments of financial institutions and timely, effective intervention and feedback. (Ongoing) | |||||||||||||

| Description Monitor and supervise financial institutions; monitor the financial and economic environment to identify emerging issues and risks. Intervene in a timely manner to protect depositors and policyholders while recognizing that OSFI cannot eliminate the possibility of failures. |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – Successfully met

2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||

PRIORITY A

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |

| Program Sub-Activity: Risk Assessment and Intervention | |

| Priority A: Readiness Planning (New) | |

Description

|

|

Key Expected Results

|

|

Key Performance Measures / Achieved Results

|

Ratings 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A |

|

Performance Discussion Steps taken during the year in support of this objective include:

Steps planned for the future to improve performance include:

|

|

| Financial Resources and Human Resources: Included in Priority 1 | |

PRIORITY B

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |

| Program Sub-Activity: Risk Assessment and Intervention | |

| Priority B: Basel II: Implementation Phase (Previously committed) | |

|

Description The implementation of the Basel II Capital Accord in Canada is a multi-year initiative. In 2007-2008 the objective of the program was to:

|

|

Key Expected Results

|

|

Key Performance Measures / Achieved Results

|

Ratings

2007-08 –Successfully met |

|

Performance Discussion

Steps taken during the year in support of this objective include

Steps planned for the future to improve performance include: The Basel II program has now moved into the post-implementation phase. Work in the next year will focus on:

|

|

| Financial Resources and Human Resources: Included in Priority 1 | |

PRIORITY C

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |

| Program Sub-Activity: Risk Assessment and Intervention | |

| Priority C: Financial Sector Assessment Program (FSAP) Update / Financial Action Task Force (FATF) (New) | |

| Description Participate in FSAP Update and FATF review and be in a position to deal with any feedback that results from the reviews. |

|

| Key Expected Results OSFI will receive an independent view as to whether it develops, maintains and contributes to a regulatory framework that meets or exceeds international minimums. |

|

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – |

|

Performance Discussion

Steps taken during the year in support of this objective include: FSAP

|

|

| Financial Resources and Human Resources: Included in Priority 1 | |

PRIORITY 2

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|||||||||||||

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |||||||||||||

| Program Sub-Activity: Rule Making | |||||||||||||

| Priority 2: A balanced, relevant regulatory framework of guidance and rules for financial institutions that meets or exceeds international minimums. (Ongoing) | |||||||||||||

| Description Issuance of guidance and input into federal legislation and regulations affecting financial institutions. Contribute a regulatory perspective to accounting, auditing and actuarial standards as required. Contribute to the development of international prudential rule-making. |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||

PRIORITY D

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |

| Program Sub-Activity: Rule Making | |

| Priority D: Accounting Standards: Implement move from Generally Accepted Accounting Principles (GAAP) to International Financial Reporting Standards (IFRS) (Previously committed) | |

| Description Implement the move from Canadian Generally Accepted Accounting Principles to International Financial Reporting Standards by addressing changes to OSFI's prudential regime, including consideration of changes in accounting for insurance. This is a multi-year priority with full implementation expected to be completed by 2011. |

|

Key Expected Results

|

|

Key Performance Measures / Achieved Results

|

Ratings

2007-08 –

2007-08 – N/A 2006-07 – Successfully met 2005-06 – N/A |

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|

| Financial Resources and Human Resources: Included in Priority 2 | |

PRIORITY E

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |

| Program Sub-Activity: Rule Making | |

| Priority E: Minimum Continuing Capital Surplus Requirements (MCCSR) (New) | |

| Description Develop and agree on a capital framework for life insurance companies. This is a multi-year priority with staged implementation expected to begin in 2011. |

|

Key Expected Results

|

|

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – |

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|

| Financial Resources and Human Resources: Included in Priority 2 | |

PRIORITY 3

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|||||||||||||

| Program Activity: Regulation and Supervision of Federally Regulated Financial Institutions | |||||||||||||

| Program Sub-Activity: Approvals | |||||||||||||

| Priority 3: A prudentially effective, balanced and responsive approvals process. (Ongoing) | |||||||||||||

| Description Approvals include those required under the legislation applicable to financial institutions and other approvals for supervisory purposes. |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||

PRIORITY 4

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|||||||||||||

| Program Activity: Regulation and Supervision of Federally Regulated Private Pension Plans | |||||||||||||

| Program Sub-Activity: Activities related to the Regulation and Supervision of Federally Regulated Private Pension Plans | |||||||||||||

| Priority 4: Accurate risk assessments of pension plans, timely and effective intervention and feedback, a balanced, relevant regulatory framework, and a prudentially effective and responsive approvals process. (Ongoing) | |||||||||||||

| Description Incorporates risk assessment, intervention, rule making and approvals related to federally regulated private pension plans under the Pension Benefits Standards Act, 1985. |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

For Measures 2, 3 and 4 above: In 2005, OSFI commissioned independent consultations with pension plan sponsors and professionals. Among sponsors (62%) and professionals (79%), satisfaction with OSFI as a regulator of federal private pension plans was moderately high. Source: Pension Consultation Findings 200510 |

Ratings

2007-08 – Successfully met

2007-08 – N/A 2006-07 – N/A 2005-06 – N/A 2007-08 – N/A 2006-07 – N/A 2005-06 – N/A 2007-08 – N/A 2006-07 – N/A 2005-06 – N/A |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||

PRIORITY F

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|

| Program Activity: Regulation and Supervision of Federally Regulated Private Pension Plans | |

| Program Sub-Activity: Activities related to the Regulation and Supervision of Federally Regulated Private Pension Plans | |

| Priority F: Pension Systems and Processes (New) | |

| Description Enhance OSFI's ability to perform as required in an increasingly complex pensions environment. This is a multi-year priority with full implementation expected in 2010-2011. |

|

Key Expected Results

|

|

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – Successfully met |

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|

| Financial Resources and Human Resources: Included in Priority 4 | |

PRIORITY 5

| Strategic Outcome: Regulate and Supervise to Contribute to Public Confidence in Canada's Financial System and Safeguard from Undue Loss |

|||||||||||||

| Program Activity: International Assistance | |||||||||||||

| Program Sub-Activity: Activities related to International Assistance | |||||||||||||

| Priority 5: Contribute to awareness and improvement of supervisory and regulatory practices for selected foreign regulators through the operation of an International Assistance Program. (Ongoing) | |||||||||||||

| Description This program activity incorporates activities that provide help to other selected countries that are building their supervisory and regulatory capacity. The costs for this program are recovered primarily via a Memoranda of Understanding between OSFI the Canadian International Development Agency (CIDA). |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – Successfully met |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||

| Strategic Outcome: Contribute to Public Confidence in Canada's Public Retirement Income System | |||||||||||||

| Program Activity: Office of the Chief Actuary (OCA) | |||||||||||||

| Program Sub-Activities: Canada Pension Plan & Old Age Security; Public Pension Plans; Canada Student Loans | |||||||||||||

| Priority 6: Contribute to ensuring there are financially sound federal government public pension and other programs. (Ongoing) | |||||||||||||

| Description The OCA provides a range of actuarial services, under legislation, to the Canada Pension Plan (CPP) and some federal government departments. The OCA estimates long-term expenditures, revenues and current liabilities of the CPP and of long-term future expenditures for the Old Age Security (OAS) program, and prepares statutory triennial actuarial reports on the financial status of the Public Sector Pension and Benefits Plans. The OCA also undertakes the actuarial review of the Canada Student Loans Program (CSLP). |

|||||||||||||

Key Expected Results

|

|||||||||||||

Key Performance Measures / Achieved Results

|

Ratings

2007-08 – Successfully met 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A 2007-08 – Successfully met 2006-07 – Successfully met 2005-06 – Successfully met 2007-08 – Successfully met 2006-07 – Successfully met 2005-06 – Successfully met 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A 2007-08 – Successfully met 2006-07 – N/A 2005-06 – N/A |

||||||||||||

|

Performance Discussion

Steps taken during the year in support of this objective include:

|

|||||||||||||

|

Financial Resources ($ millions)

Human Resources (average Full-Time Equivalents, including Internal Services)

|

|||||||||||||