Treasury Board of Canada Secretariat

www.tbs-sct.gc.ca

Common menu bar links

Breadcrumb Trail

ARCHIVED - Office of the Superintendent of Financial Institutions Canada

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

SECTION I: OVERVIEW

I.1 Message from the Superintendent

I am pleased to present the Departmental Performance Report (DPR) for the Office of the Superintendent of Financial Institutions (OSFI) for the period ending March 31, 2008.

This report focuses on the benefits of OSFI's contribution to Canadians and to Canada’s financial and economic strength. It concentrates primarily on our two strategic outcomes: to regulate and supervise financial institutions and private pension plans so as to contribute to public confidence; and to contribute to public confidence in Canada's public retirement income system. Both strategic outcomes support the Government of Canada’s desired outcomes of strong economic growth and income security for Canadians. In addition, OSFI’s technical assistance program, which helps emerging market economies improve their financial institution supervisory systems, supports the government’s priority for a safe and secure world through international co-operation.

This past year was a tumultuous one for the financial sector, beginning with a downturn in the U.S. sub-prime mortgage market and quickly spreading to financial markets around the globe which are inextricably linked. Capital and credit markets seized up, some large financial institutions in other countries were taken over, and around the world losses were very real.

Canada’s banks entered this period very well capitalized, which has helped them weather the storm relatively well to date; however, there have been some losses at Canadian banks which, in some cases, were significant. As well, there was a major problem in the Canadian non-bank asset-backed commercial paper (ABCP) market. The ABCP issue led to significant public discussion over the year regarding liquidity lines to ABCP conduits and OSFI's role. We explained that we are responsible for assessing bank solvency, that OSFI capital rules apply to Canadian banks only (and not to other companies at the centre of the non-bank ABCP market or to the mainly foreign banks they dealt with), that our capital rules were prudent and necessary for bank solvency, and that securities commissions have a mandate to protect investors in ABCP securities.

Change is constant, and the financial landscape will continue to shift in ways that are not fully predictable at this time. That is why cushions are so important, and why OSFI focuses on capital, liquidity and stress testing at financial institutions. As well, in the spring of 2007, OSFI placed more focus on enhancing our ability to identify risks. Initiatives have included the creation of an internal Emerging Risk Committee and more interaction with international supervisors, so as to better assess the impact of changing risk on financial institutions and pension plans.

One of OSFI's priorities has been the successful implementation of the Basel II Capital Accord. The revised Basel Capital Framework (Basel II) became effective for Canadian banks on November 1, 2007. It will play a key role in strengthening risk management practices at banks. Efforts are now underway by the Basel Committee to update parts of Basel II for which capital was insufficient, based on knowledge gained as a result of the recent turmoil.

The Accounting Standards Board (AcSB) has decided that publicly accountable enterprises will be required to move to International Financial Reporting Standards (IFRS) as of 2011. IFRS implementation is an ongoing priority for OSFI to ensure consistent reporting for the purpose of reliable comparisons and effective monitoring of issues of safety and soundness. Work, both domestically and internationally, towards the implementation of IFRS is ongoing, and OSFI will continue to add a Canadian voice in international efforts to develop guidance related to the IFRS regime. Beginning in 2008-2009, OSFI will conduct extensive consultations with federal financial institutions regarding the effects of adopting IFRS, so as to work towards a smooth implementation.

Another of our priorities is to revise the current Minimum Continuing Capital and Surplus Requirements (MCCSR) regime to reflect IFRS developments, and to adopt more risk-based approaches as was done for banks under the Basel Accord, after consultation with the life insurance industry.

Reviews performed by the Office of the Chief Actuary (OCA) indicate that Canada has a public pension system that is expected to be sustainable and affordable well into the future. During 2007-2008, the OCA released Actuarial Study Number 6 on the Optimal Funding of the Canada Pension Plan (CPP) which examined the current funding approach of the Canada Pension Plan in terms of its optimality compared to other funding approaches. This, and future studies, seek to ensure the actuarial soundness of Canada's public retirement system.

In its regulation of private pension plans, OSFI has begun a review of its existing systems and processes with an eye to increasing efficiency and effectiveness. While there is minimal volatility in the private pension sector currently, we must continue to be vigilant and knowledgeable about techniques to manage the potential risks volatility can pose.

Looking ahead, we will continue to work to maintain our strong international reputation, as confirmed by an International Monetary Fund Financial Sector Assessment Program (FSAP) Report released in February. A major achievement in 2007-2008, the FSAP report noted that Canada's “financial stability is underpinned by…strong prudential regulation and supervision.” OSFI will also face the effects of a softening global economy, which will have an impact on the financial institutions and private pension plans that OSFI oversees. OSFI's initiatives to enhance risk identification, as well as an announced ten percent increase in human resources will help ensure we are prepared to deal with any issues.

Virtually all of OSFI's revenues are derived from industry. Because OSFI places significant reliance on the internal processes of the financial institutions it regulates, OSFI's costs are generally lower than regulatory bodies that do not use such systems. OSFI will continue to hire and retain the staff necessary to address the complex issues inherent in the financial services environment, and to better enable us to monitor and assess risk in the financial institutions and pension plans we regulate.

OSFI will continue to play a pivotal role in the Canadian financial services industry, and to assess and measure our performance to retain and enhance our reputation as a world leader in financial regulation and supervision. I am confident that we will continue to contribute to the confidence Canadians rightly have in their financial system.

I.2 Management Representation Statement

I.3 Summary Information

I.3.1 OSFI's Reason for Existence

Mandate

OSFI's legislated mandate, established in 1996, is to:

- Supervise federally regulated financial institutions and private pension plans to determine whether they are in sound financial condition and meeting minimum plan funding requirements respectively, and are complying with their governing law and supervisory requirements;

- Promptly advise institutions and plans in the event there are material deficiencies and take, or require management, boards or plan administrators to take, necessary corrective measures expeditiously;

- Advance and administer a regulatory framework that promotes the adoption of policies and procedures designed to control and manage risk; and

- Monitor and evaluate system-wide or sectoral issues that may impact institutions negatively.

In meeting this mandate, OSFI contributes to public confidence in the financial system.

OSFI's legislation also acknowledges the need to allow institutions to compete effectively and take reasonable risks. It recognizes that management, boards of directors and plan administrators are ultimately responsible for setting strategy and managing the financial institutions and pension plans, and that they can fail.

The Office of the Chief Actuary (OCA), which is an independent unit within OSFI, provides actuarial services to the Government of Canada.

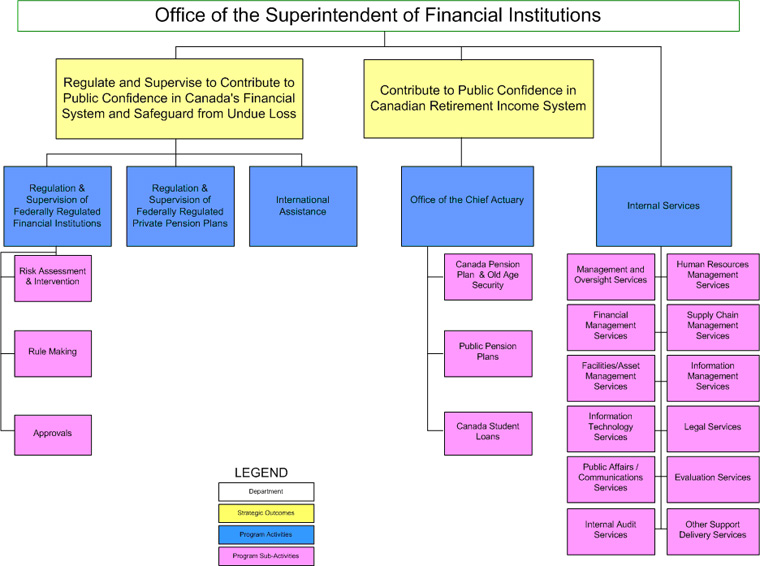

I.3.2 Program Activity Architecture

I.3.3 Total Financial and Human Resources

The tables below identify OSFI's financial and human resources, planned and actual, for the 2007-2008 fiscal year. OSFI's actual number of average full-time equivalents (FTEs) for the year was 459 or two less than planned and 13 more than the previous year1.

2007-2008 Financial Resources ($ millions)

| Planned | Authorities | Actual |

| $90.5 | $90.5 | $85.7 |

2007-2008 Human Resources (Average Full-Time Equivalents)

| Planned | Actual | Difference |

| 461 | 459 | 2 |

I.3.4 Priorities2

| Name | Type | Performance Status |

| Management Priorities | ||

| A. Readiness Planning | New | Successfully met |

| B. Basel II | Previously committed | Successfully met |

| C. Financial Sector Assessment Program (FSAP) / Financial Action Task Force (FATF) | New | Successfully met |

| D. Accounting Standards | Previously committed | Successfully met |

| E. Minimum Continuing Capital Surplus Requirement (MCCSR) |

New | Successfully met |

| F. Pension Systems and Processes | New | Successfully met |

| G. Integration of Human Resources Planning into Business Planning | New | Successfully met |

| Ongoing Program Priorities | ||

| 1. Risk Assessment and Intervention | Ongoing | Successfully met |

| 2. Rule Making | Ongoing | Successfully met |

| 3. Approvals | Ongoing | Successfully met |

| 4. Regulation and Supervision of Federally Regulated Private Pension Plans | Ongoing | Successfully met |

| 5. International Assistance | Ongoing | Successfully met |

| 6. Office of the Chief Actuary (OCA) | Ongoing | Successfully met |

| Ongoing Program Support Priorities | ||

| 7. High quality internal governance and related reporting. | Ongoing | Successfully met |

| 8. Resources and infrastructure necessary to support supervisory and regulatory activities. | Ongoing | Successfully met |

I.3.5 Program Activities by Strategic Outcome

| Expected Results | Performance Status | 2007-2008 ($millions) |

Links to the following priorities | ||

| Planned Spending |

Actual Spending |

||||

Strategic Outcome 1: To regulate and supervise to contribute to public confidence in Canada's financial system and safeguard from undue loss. |

|||||

| Program Activity 1.1 Regulation and Supervision of Federally Regulated Financial Institutions |

|||||

|

Accuracy of risk assessment and early intervention; effective support and facilitation for Basel II implementation. | Successfully met | $53.5 | $51.4 | Management Priorities A, B, C and G |

|

Balanced regulatory framework; prudent capital rules and regulatory reporting and alignment with other jurisdictions. | Successfully met | $14.7 | $14.2 | Management Priorities D, E and G |

|

Prudentially sound and responsive approvals process. | Successfully met | $7.7 | $7.2 | Management Priority G |

| Program Activity 1.2 Regulation and Supervision of Federally Regulated Private Pension Plans (Ongoing Program Priority 4) |

Accuracy of risk assessment and early intervention. | Successfully met | $6.5 | $5.8 | Management Priorities F and G |

| Program Activity 1.3 International Assistance (Ongoing Program Priority 5) |

Improved supervisory and regulatory practices for foreign regulators. | Successfully met | $2.0 | $2.0 | Management Priority G |

Strategic Outcome 2: To contribute to public confidence in Canada's public retirement income system. |

|||||

| Program Activity 2.1 Office of the Chief Actuary (Ongoing Program Priority 6) |

Expert and timely actuarial valuations and advice. | Successfully met | $6.1 | $5.1 | Management Priority G |

Note: Internal Services, per OSFI's Program Activity Architecture (PAA) are considered part of every Program Activity and are linked to OSFI's ongoing Program Support Priorities 7 and 8.

I.4 Summary of Departmental Performance

I.4.1 Operating Environment

OSFI was created in 1987 through the enactment of the Office of the Superintendent of Financial Institutions Act (OSFI Act). The OSFI Act provides that the Superintendent is solely responsible for exercising the authorities provided by the financial legislation, and is required to report to the Minister of Finance from time to time on the administration of the financial institutions’ legislation. The Superintendent periodically appears before various House of Commons and Senate Committees.

The Office of the Chief Actuary (OCA) was created within the organization as an independent unit to effectively provide actuarial and other services to the Government of Canada and provincial governments who are Canada Pension Plan (CPP) stakeholders. The Chief Actuary is solely responsible for the content and the actuarial opinions in reports prepared by the OCA. The Chief Actuary periodically appears before various House of Commons and Senate Committees.

Key Partners

OSFI works with a number of key partners. Together, these organizations constitute Canada's network of financial regulation and supervision and provide a system of depositor and policyholder protection.

| Regulatory and Supervisory Framework Roles | |

| Government Organization | Role |

| Department of Finance |

|

| Canada Deposit Insurance Corporation |

|

| Bank of Canada |

|

| Financial Consumer Agency of Canada |

|

| Financial Transactions and Reports Analysis Centre of Canada |

|

OSFI collaborates with provincial and territorial supervisory and regulatory agencies, as necessary, and with private-sector organizations and associations, particularly in rule making.

OSFI plays a key role in international organizations such as the Basel Committee on Banking Supervision, the Joint Forum, the Financial Stability Forum, the International Association of Insurance Supervisors, the Integrated Financial Supervisors, the Association of Supervisors of Banks of the Americas, the International Actuarial Association, and the Groupe des superviseurs bancaires francophones.

Regulated Entities

OSFI is the primary regulator of financial institutions and private pension plans operating in Canada under federal jurisdiction. OSFI supervises and regulates all federally incorporated or registered deposit-taking institutions, life insurance companies, property and casualty insurance companies, and federally regulated private pension plans. These 1,809 organizations managed a total of $3,823 billion of assets (as at March 31, 2008).

Federally Regulated Financial Institutions and Private Pension Plans and Related Assets

| Deposit- Taking Institutions | Life Insurance Companies | Property and Casualty Companies | Federally Regulated Private Pension Plans | Total | |

| Number of organizations | 151 | 112 | 196 | 1,350 | 1,809 |

| Assets | $3,103 billion | $479 billion | $109 billion | $132 billion | $3,823 billion |

OSFI also undertakes supervision of provincially incorporated financial institutions on a cost recovery basis under contract arrangements with some provinces. Additional details may be found on OSFI's Web site under About OSFI/ Who We Regulate.

Cost Recovery

OSFI recovers its costs from several revenue sources. OSFI is funded mainly through asset-based, premium-based or membership-based assessments on the financial institutions and private pension plans that OSFI regulates and supervises, and a user-pay program for selected services.

OSFI also receives revenues for cost-recovered services. These include revenues from the Canadian International Development Agency (CIDA) for international assistance; revenues from provinces for which OSFI does supervision of their financial institutions on contract; and revenues from other federal agencies for which OSFI provides administrative support.

Overall, OSFI recovered all its expenses for the fiscal year 2007-2008.

The Office of the Chief Actuary is funded by fees charged for actuarial services relating to the Canada Pension Plan, the Old Age Security program, the Canada Student Loans Program and various public sector pension and benefit plans, and by a parliamentary appropriation.

For further information, refer to OSFI's Annual Report, which is published on OSFI's web site under Organization / Reports/ Annual Reports.

I.4.2 Context

Financial and Competitive Environment

Credit market issues dominated the global financial landscape in 2007. The environment has been difficult, particularly for global banks, and the adjustment period could be prolonged.

Starting in the summer of 2007, accumulating losses on U.S. subprime mortgages triggered widespread disruption to the global financial system. Large losses were sustained on complex structured securities. Institutions reduced leverage and increased demand for liquid assets. Many credit markets became illiquid, hindering credit extension. More than eight months after the start of the market turmoil, the balance sheets of financial institutions remain burdened by assets that suffered declines in value and are further affected by vanishing market liquidity. While Canadian banks have not been immune from these developments, as a group they have faired relatively well.

Overall, the financial performance of the major Canadian banks for 2007 was relatively strong, however, a few banks took material write downs and were pressured to bring securitized assets back on their books, both in the fourth quarter of 2007 and the first quarter of 2008.

When the turmoil in the asset-backed commercial paper (ABCP) markets began in August 2007, OSFI moved to assess the impact on all federally regulated institutions (and pension plans). Very few institutions OSFI oversees had material exposure to non-bank ABCP, which was the most affected. In terms of the size of the non-bank market, according to figures provided in the Bank of Canada's December 2007 issue of the Financial System Review, non-bank asset backed commercial paper, as at July 2007 comprised about $35 billion, versus a total ABCP market of $116 billion.

Average return on equity for major Canadian banks in 2007 was 21.2%, down from a high of 23.2% in 2006. The average ratio of total capital to risk-adjusted assets was 11.9%, well above the Bank for International Settlements’ 8% minimum threshold and OSFI's 10% target. These high levels of capital provide a buffer against future adverse economic or financial developments.

With overall strong capital and returns, the life insurance industry was in a healthy position at the close of 2007-2008; however, it faces challenges associated with softening global growth, corrections in equity markets and the possibility of an extended low interest rate environment. Average return on equity was 13.4%, down modestly from 13.7% the year before. OSFI's supervisory target ratio for Minimum Continuing Capital and Surplus Requirements (MCCSR) for Canadian companies is set at 150%. The average MCCSR ratio for Canadian life insurers in 2007 was 218%, significantly above OSFI's target ratio, indicating a well capitalized industry.

After several years of strong operating results, the property and casualty (P&C) insurance sector is starting to show signs of stress. Although 2007 industry results were strong, most indicators pointed to a year-over-year decline in performance. Industry return on equity was 16.1%, down from 20.3% the previous year. A principle measure of profitability for the industry is the combined ratio, which measures claims expenses to premium income – a result under 100% indicates that premium income exceeds claims expenses (before associated investment returns). In 2007, the combined ratio increased from 88.6% to 91.9%. Although increasing, the result indicates that the core business of the P&C industry continues to operate profitably.

Favourable market conditions through 2006 and into 2007 lessened funding pressures for many private pension plans going into 2007. The downward pressure on long-term interest rates appeared to ease. However, at year-end the liability discount rate was only marginally higher than a year earlier, and with the emergence of market turbulence in mid-2007, average investment returns for 2007 as a whole were very modest. The returns were characterized by wide divergence across individual plans, depending on their investment strategy and asset mix. As a result of these developments, funding pressures on pension plans have not disappeared.

Policy Environment

Work has begun at both the industry and regulatory level in Canada and globally to analyze lessons learned, and to develop guidance and processes that would restore stability and investor confidence in the financial marketplace. Canadian government agencies met regularly to discuss impacts on industry and institutions, and the Bank of Canada extended liquidity to the system.

The Superintendent worked with international colleagues to draft the Financial Stability Forum (FSF) report on Enhancing Market and Institutions Resilience. The G7 Finance Ministers and Central Bank Governors established the FSF in 1999 to promote international financial stability through enhanced information exchange and international cooperation in financial market supervision and surveillance.

The FSF report includes over 60 recommendations that have been endorsed by the G-7 Finance Ministers, and covers key issues such as capital and liquidity for banks, as well as the need for more transparency. Much has already been done by central bankers, regulators and accounting standard setters to identify the causes of the global market turmoil, and to identify what should be done, but the implementation of the FSF report recommendations will take considerable effort and will go a significant way toward strengthening the global financial system. OSFI is currently working with other regulatory agencies to implement these recommendations in Canada.

Revisions to Financial Institutions Legislation

An Act to amend the law governing financial institutions and to provide for

related and consequential matters received Royal Assent in March 2007.

While the bulk of its provisions have been implemented, in 2007-2008 OSFI

continued to work closely with the Department of Finance on the development of

regulations in the context of the implementation of certain aspects of the Act.

Anti-Money Laundering and Anti-Terrorism Financing Initiatives

Extensive changes to the Proceeds of Crime (Money Laundering) and Terrorist

Financing Act were enacted by Parliament in 2007-2008. Most of the

regulatory changes are to take effect in June 2008. OSFI amended its assessment

methodology to take these new requirements into account.

I.4.3 Overall Performance

Despite new challenges presented by volatility in the global markets, in 2007-2008 OSFI was nonetheless successful in meeting the expectations flowing from all of its priorities. In addition to six ongoing priorities, OSFI's 2007-2008 Report on Plans and Priorities (RPP) identified seven management priorities. While a detailed analysis of OSFI's performance against all priorities is found in Section II, the following highlights some of OSFI's accomplishments for the reporting period.

Management Priorities

OSFI's ability to achieve its mandate depends on the timeliness and effectiveness with which it identifies, evaluates, prioritizes, and develops initiatives to address areas where its exposure to risk is greatest. In the RPP for 2007-2008, OSFI had identified several external and internal risks, and throughout the year took steps to address these risks.

Readiness Planning

OSFI took steps to ensure it can respond adequately to shocks as a result of a

crisis or a pandemic, and cyclicality in the industry. Among other steps, OSFI:

surveyed business resumption plans of federally regulated financial

institutions; completed resource analysis and planning to enable OSFI to address

the growing risk profiles across the industries it regulates; conducted a

table-top exercise with OSFI senior executives to test their command and control

structure while relocated to a simulated backup Emergency Command Centre.

Basel II Capital Accord

The revised Basel Capital Framework (Basel II) became effective for Canadian

banks on November 1, 2007. OSFI gave approval to a number of banks to operate

under the Advanced Internal Ratings Based approach under Basel II, and assisted

smaller deposit-taking institutions to transition successfully to the

Standardized approach for credit risk. OSFI also reviewed its practices to align

with Basel II requirements, specifically by revising Capital Adequacy

Requirements (CAR) Guidelines to incorporate a number of clarifications raised

by industry, and by issuing relevant advisories to update the CAR Guidelines in

response both to market developments and to accounting, legislative and other

changes.

Accounting

The Canadian Accounting Standards Board has decided to adopt International

Financial Reporting Standards (IFRS) by 2011 as the basis for financial

reporting by public companies in Canada. This will have a significant impact on

both OSFI and the institutions it regulates. OSFI developed a detailed project

plan and team to guide internal implementation efforts as well as to help assess

the effects moving to IFRS will have on institutions and the need for new or

modified guidance from OSFI. OSFI also worked closely with key national and

international organizations to present its views on these issues.

Minimum Continuing Capital Surplus Requirement (MCCSR)

OSFI continued its efforts towards the adoption of revised MCCSR rules by

working with the life insurance industry through the MCCSR Advisory Committee

(MAC) to develop and incorporate more advanced risk measurement techniques into

the MCCSR. Also through MAC, OSFI issued a paper outlining the vision for a new

more risk-sensitive capital framework for life insurers. The MCCSR Advisory

Committee's draft vision paper may be found on OSFI's website under

Regulated Entities / Life Insurance Companies and Fraternals / Drafts and

Consultation Papers.

Financial Sector Assessment Program (FSAP) Update / Financial Action Task

Force (FATF) Mutual Evaluation

During 2007-2008, OSFI participated in two important reviews. The International

Monetary Fund (IMF) conducted a Financial Sector Assessment Program (FSAP)

Update of Canada, and the FATF conducted an assessment of Canada's anti-money

laundering and anti-terrorist regimes. The IMF's FSAP report on Canada found

OSFI to be compliant with all four Core Principles of Supervision assessed and

noted that the Canadian financial sector is strong and its major banks would be

able to withstand sizeable shocks to the financial system. The FATF mutual

evaluation report recognized the good supervisory coverage of the banking and

federally regulated trust companies by OSFI. The FATF mutual evaluation report

(MER) also recognized OSFI's role in Canada's anti-money

laundering/anti-terrorism financing (AML/ATF) regime as being effective.

People Risks

Attracting, motivating, developing and retaining skilled staff is a top priority

for OSFI, particularly the ability to attract and retain staff whose skills are

in demand in an increasingly complex and dynamic financial sector. OSFI took

steps to put in place better long-range, integrated planning, including the

creation of a new supervisory team based in Ottawa to assist the Toronto-based

Financial Institutions Group in managing the workload created by the growing

risk profiles across OSFI's regulated industries, and new positions for

2008-2009 to increase capacity and complement targeted technical skills in

anticipation of emerging risks. OSFI also continued to recruit specific subject

matter experts.

Pension Systems and Processes

The external environment for pensions includes increasingly complex work and

more litigation. This demands greater skill on the part of OSFI staff who

require the support of an upgraded pensions information system. OSFI refined its

internal processes to improve efficiency and timeliness of pension approvals,

and initiated Information Technology system enhancements to further support

approval processes. OSFI also continued development of a new risk assessment

framework for pension plans, to be followed by enhancements to the pension IT

system to support efficient supervisory processes.

Ongoing Program and Support Priorities

In 2007-2008, OSFI's risk and intervention activities were largely driven by developments in the market place. As a result, a major focus for OSFI was on managing the impact of volatile credit and financial markets on federally regulated financial institutions’ (FRFIs) liquidity and capital levels. In addition to working with international colleagues to draft the Financial Stability Forum report on Enhancing Market and Institutional Resilience, and the Basel Committee on Banking Supervision's announced steps to strengthen the resilience of the banking system,OSFI was proactive in intervening with several institutions in order to improve risk management and governance practices. OSFI also maintained up-to-date risk profiles of all federally regulated financial institutions – a low or moderate Composite Risk Rating was assigned to 94% of all rated institutions for 2007-2008.

OSFI continued to evolve the regulatory framework for financial institutions it supervises. Some of the key achievements for this year were: updates to guidelines and advisories related to the measurement of capital and capital adequacy of banks and trust and loan companies; engaging in discussions with the life insurance industry on how to update the current approach to measuring life insurance regulatory capital requirements for the new accounting standards that cause material changes to balance sheet items used in the measurement of risks captured in the requirements; and releasing Guideline E-17, renamed as Background Checks on Directors and Senior Management of Federally Regulated Entities (FREs). Guideline E-17 is consistent with international developments and with regulatory standards in comparable foreign jurisdictions.

To align with, and respond to, the changing external environment for pensions, OSFI continued a review of the pension risk assessment framework begun in 2006-2007 in order to strengthen the risk-focused approach to pension supervision and to direct our resources most effectively. In addition, OSFI worked with the Department of Finance to develop legislation and regulations for phased-in retirement, and added resources and introduced more streamlined processes to improve timeliness of its pensions approvals process while ensuring complex transactions are carefully considered.

In the international arena, OSFI continued its work with foreign regulators and sharing its expertise in improvement of supervisory and regulatory practices in many countries. Significant inroads made into African nations last year were strengthened as close working relationships developed with Ghana, Nigeria and Malaysia to support these jurisdictions’ transition to risk-based supervision for financial institutions. As well, CIDA's performance review of OSFI's International Advisory Group (IAG) indicated that training workshops were seen to be useful and that there have been generally sustainable impacts on capacity building in countries where IAG has established continuing relationships.

Finally, OSFI, through the Office of the Chief Actuary (OCA), continued to provide its expert actuarial valuation and advice to the Federal Government for sound financial management of the Public Sector Pension and Insurance Programs. The OCA completed actuarial reports on the Canada Pension Plan, the Canada Student Loans Program, the pension plans for the Members of Parliament and Federally Appointed Judges, and on the benefit plan financed through the Royal Canadian Mounted Police (dependants) Pension Fund. These reports provide actuarial information to decision-makers, Parliamentarians and the public, increasing transparency and confidence in the retirement income system. An external peer review – the CPP Actuarial Review Panel – confirmed that the 23rd CPP Actuarial Report met high professional standards and was based on reasonable assumptions to provide sound actuarial advice to Canadians.

Internal Audits and Reviews

OSFI has an independent internal audit function that objectively reviews, monitors and analyzes OSFI's key activities. During 2007-2008, a number of reviews were completed in which areas for improvement were identified. Internal audit reports, which include a management response, are posted on OSFI's website under Organization / Reports / Internal Audit Reports.

The Internal Audit Report on the Staffing Process indicated that the staffing framework is fundamentally sound, but identified areas where certain policies, guidance, and processes needed improvement to ensure the staffing action activities and files fully support the decisions made. In response to these recommendations, an improvement program was implemented to address all concerns identified.

The Internal Audit Review Report on OSFI's Planning Activities and Processes presented an assessment of OSFI's current planning process and tools, and recognized the significant enhancements that OSFI implemented or initiated during the 2008-2011 planning cycle. A multi-year improvement program was established to address the report's findings and recommendations.

A review of the Financial Institutions Group – Deposit Taking Institutions (FIG-DTI) assessed whether the supervision of the institutions in this group was risk-focused and whether the resulting risk assessments were reasonable and well supported. The report concluded that FIG-DTI staff demonstrated a sound understanding of the business activities of their institutions and rated inherent risks in these activities. However, the review found that the application of the methodology requires improvement in a number of areas. An improvement program has been developed.

The objective of a review of the Supervision Support Group Credit Risk Department was to assess whether OSFI's Supervisory Methodology and related practices were consistently applied in the supervisory process followed by the Credit Risk Department (CRD) in supporting the supervisory teams' examination of their credit activities. An improvement program has been established to address the recommendations flowing from the review.

Informing Canadians

OSFI remains committed to informing Canadians about its activities and plans, and to contributing to a dialogue on key issues facing the financial sector and pension plans.

In 2007-2008, OSFI made public several reports and published its external newsletter, The Pillar, three times. OSFI served some 1,215,595 visitors to the Web site; handled 12,916 public enquiries; responded to 102 enquiries from Members of Parliament, and replied to 149 enquiries from representatives of the news media.

OSFI is recognized as an international model for prudential regulators and receives many requests to address conferences and other events. In response, the Superintendent and other senior OSFI officials delivered over 35 presentations to industry and regulatory forums across Canada and internationally. The Superintendent also made presentations to Parliamentary Committees including the House of Commons Standing Committee on Finance and the Senate Standing Committee on Banking, Trade and Commerce. Most speeches and presentations are available on OSFI's Web site under Organization / Speeches.