ARCHIVED - Evaluation of the Treasury Board Submission Process

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

Evaluation of the Treasury Board Submission Process

Table of Contents

List of Appendices

- Appendix A: Logic Model

- Appendix B: Treasury Board Submission Process Evaluation Matrix

- Appendix C: Documents Reviewed

- Appendix D: List of Interviewees

- Appendix E: Interview Guides

- Appendix F: ADM Working Session Questionnaire

- Appendix G: Survey Results

- Appendix H: Description of Tools

- Appendix I: Description of EXCO Measures

- Appendix J: Definitions

List of Tables

Table 1: "Standard" vs. "Complex" Submissions- Table 2: Summary of the Evaluation Issues and Questions

- Table 3: List of Interview Group

- Table 4: Survey Response Rates

- Table 5: Assessment of Understanding of the Treasury Board Submission Process

- Table 6: Views on Drafts Submitted That Did Not Require a Treasury Board Submission

- Table 7: Assessment of the Submission Review Process

- Table 8: Survey Respondents' Views on Quality of Secretariat Advice/Interpretation - Review Stage

- Table 9: Comparison of Perceptions of Time Required to Review Treasury Board Submissions

- Table 10: Program Analysts' Perception of Change in Overall Quality of Submissions

- Table 11: Assessment of Documents Submitted for Review

- Table 12: Proportion of Time Analysts Spent on Stages of the Submission Process

- Table 13: Assessment of the Efficiency of the Treasury Board Submission Process

- Table 14: Assessment of Proposed Measures' Potential to Improve Efficiency of the Treasury Board Submission Process

List of Acronyms

| Acronym | Meaning |

|---|---|

| ADM | Assistant Deputy Minister |

| ARLU | Annual Reference Level Update |

| BOSR | Budget Office Systems Renewal |

| CFO | Chief Financial Officer |

| CIO | Chief Information Officer |

| COE | Centre of Expertise |

| DM | Deputy Minister |

| EMIS | Expenditure Management Information System |

| EMS | Expenditure Management Sector |

| ES-0# | Economics and Statistics (employee classification) |

| EX-0# | Executive (employee classification) |

| EXCO | Executive Committee |

| FAA | Financial Administration Act |

| FTE | Full-Time Equivalent |

| GIC | Governor in Council |

| GOS | Government Operations Sector |

| HR | Human Resources |

| MAF | Management Accountability Framework |

| MC | Memorandum to Cabinet |

| OIC | Order in Council |

| PDG | Program Directors Group |

| RDIMS | Records, Documents and Information Management System |

| STS | Submission Tracking System |

| Secretariat | Treasury Board of Canada Secretariat |

Acknowledgements

The Internal Audit and Evaluation Bureau (IAEB) of the Treasury Board of Canada Secretariat would like to thank all the individuals who contributed to this evaluation-interviewees, survey respondents, working session participants, and the Secretariat's Evaluation Committee-for their valuable input and support. The work of Secretariat officials involved in the validation of findings, particularly the Program Directors Group and assistant secretaries from the program sectors, was also appreciated. Finally, IAEB would like to thank the consultants, Government Consulting Services (Public Works and Government Services Canada), who undertook the evaluation, and Mark Schacter, who collaborated in writing the report.

Executive Summary

Introduction

The Treasury Board of Canada Secretariat (Secretariat) is the administrative arm of Treasury Board, a Cabinet committee whose ministers render decisions on the government's management and expenditures. The Secretariat supports Treasury Board ministers in this function and also fulfills the statutory responsibilities of a central government agency. When a federal organization is seeking approval or authority from Treasury Board for an initiative that it would not otherwise be able to undertake or that is outside its delegated authorities,1 it prepares a Treasury Board submission in consultation with the Secretariat.

This evaluation assessed the relevance, effectiveness, and economy of the Treasury Board submission process. Given that the Secretariat is the "owner"; of the Treasury Board submission process, the evaluation paid close attention to the role it plays in contributing to the success of the process. It should be noted that the scope of this evaluation was limited to the current process used to support Treasury Board ministers and did not include an assessment of the process against potential alternative mechanisms for providing this support. A limited review of international practices was conducted as part of the evaluation; however, the review was not sufficiently in-depth to suggest alternative mechanisms for the Secretariat to explore.

The evaluation framework used multiple lines of evidence and complementary research methods to ensure the reliability and validity of the data. The following research methods were used:

(i) document review; (ii) interviews with stakeholders and experts; (iii) a working session with assistant secretaries from the Secretariat and assistant deputy ministers from selected federal organizations; (iv) review of administrative, financial, and statistical data; and (v) a survey of analysts at the Secretariat and in federal organizations. A limitation of the methodology was that Treasury Board ministers could not be interviewed because data collection was undertaken during an election period.

The evaluation covered all steps of the current submission process involving the Secretariat:

- the support that the Secretariat provides to federal organizations;

- guidance developed by the Secretariat, such as that found in A Guide to Preparing Treasury Board Submissions (the Guide);

- the communication of decisions regarding submissions; and

- the tracking of conditions placed on approved submissions.

The evaluation did not include federal organizations' internal processes for preparing Treasury Board submissions. Furthermore, the evaluation covers only "Part A" submissions.2

This is the first formal evaluation of the Treasury Board submission process; therefore, it was not possible to anticipate, at the outset, all the evaluation issues to be addressed and lines of inquiry to be pursued. Because the data-gathering exercise uncovered evaluation issues that were not initially apparent, new lines of evidence were introduced, such as additional document reviews, additional interviews, and validation sessions with Secretariat senior management. The research for the evaluation was conducted between November 2008 and March 2009.

Conclusion

The current Treasury Board submission process is relevant, appears to be effective, and has key strengths; however, some important opportunities exist to improve and enhance its effectiveness and efficiency, which should be addressed through a combination of action and further investigation.

Strengths:

- The submission process is relevant to the government's good public management needs. Determining whether there are other effective and efficient alternatives to accomplish the same outcomes was outside the scope of the evaluation.

- There is widespread belief among stakeholders that the submission process is successful at ensuring that federal organizations present submissions that comply with legislative authorities and Treasury Board policies.

- There is widespread belief among stakeholders that the submission process is successful at ensuring that federal organizations put forth appropriate submissions.

- Treasury Board decisions appear to reflect the advice of the Secretariat to a high degree, which is indicative of Treasury Board's confidence in the quality of that advice.3

Opportunities for improvement:

- There is a need to finalize the logic model for the Treasury Board submission process to support performance measurement, clear communication of the process's ultimate outcome, and further study.

- A majority of federal organizations are satisfied with the support and advice they receive from the Secretariat's program analysts; however, there are specific areas of concern (e.g. consistency of advice).

- The evidence on the quality of draft Treasury Board submissions is mixed.

- The Secretariat does not account for the costs of the submission process.

- The Secretariat's efforts to educate federal organizations and its own staff about the details of the submission process appear to be falling short of their intended results.

- Rather than a shared, centralized system, analysts at the Secretariat use their own private filing systems to manage documentation related to Treasury Board submissions.

Recommendations

Opportunities to improve the Treasury Board submission process fall into three areas:

- finalizing the logic model for the Treasury Board submission process;

- deepening the Secretariat's understanding of certain aspects of the process itself and practices related to it and implementing improvements to the process wherever possible; and

- providing the Secretariat's analysts with more and better tools to enhance the effectiveness and economy of the submission process.

Logic model for the Treasury Board submission process

1. The Secretariat should finalize the logic model for the Treasury Board submission process to support performance measurement, clear communication of the process's ultimate outcome, and further study.

Deeper understanding of the submission process and related practices, leading to improvements

2. The Secretariat should examine in detail, and address where necessary, survey results relating to the advice its analysts provide to federal organizations during the submission process.

3. Secretariat should examine how human resources issues, especially turnover among program analysts, affect the Treasury Board submission process and knowledge management.

4. The Secretariat should account for the costs of managing the submission process-at least for the department if not for the entire public administration.

Development of more and better tools for the submission process

5. The Secretariat should review, and improve where necessary, its professional development, training, and outreach activities related to the Treasury Board submission process.

6. The Secretariat should explore options for a more systematic approach to information and knowledge management in the Treasury Board submission process.

1. Introduction

The Treasury Board is a Cabinet committee of the Queen's Privy Council of Canada. It was established in 1867 and given statutory powers in 1869. The Financial Administration Act (FAA) provides the authority for the Treasury Board to exercise responsibilities in areas relating to general administrative policy in the federal public administration, the organization of the federal public administration, financial management, the review of annual and longer term expenditure plans and programs of federal organizations, the management and development of lands by federal organizations, human resources management in the federal public administration, the terms and conditions of employment, internal audit, and other matters determined by the Governor in Council (GIC).

The Treasury Board is headed by a President, whose formal role is to chair the Treasury Board. He carries out his responsibility for the management of the government by translating the policies and programs approved by Cabinet into operational reality and by providing federal organizations with the resources and the administrative environment they need to do their work.

The Treasury Board of Canada Secretariat (Secretariat) is the administrative arm of the Treasury Board and has a dual mandate: to support the Treasury Board itself, which is a committee of ministers, in rendering decisions on the government's management and expenditures and to fulfill the statutory responsibilities of a central government agency. With respect to the Treasury Board submission process, the Secretariat provides advice and support to Treasury Board ministers in fulfilling their responsibilities as outlined in the FAA and their role of ensuring value for money in government spending through oversight of federal organizations' financial management functions. The Secretariat makes recommendations and provides advice to the Treasury Board on policies, directives, regulations, and program expenditure proposals involving the management of the government's resources. Treasury Board's responsibilities for the general management of the government have an impact on initiatives, issues, and activities that cut across all policy sectors managed by federal organizations and organizational entities.

A Treasury Board submission is required when a federal organization is seeking approval or authority from Treasury Board for an initiative that it would not otherwise be able to undertake or that is outside its delegated authorities. Treasury Board submissions can relate to one or more of the Treasury Board responsibilities outlined in the FAA.

The Treasury Board submission process has never been evaluated; as a key line of business of the Secretariat, it was important to do so. This evaluation assessed the relevance, effectiveness, and economy of the Treasury Board submission process. Given that the Secretariat is the "owner" of the Treasury Board submission process, the evaluation paid close attention to the role played by the Secretariat in contributing to the success of the process. It should be noted that the scope of this evaluation was limited to the current process used to support Treasury Board ministers and did not include an assessment of the process against potential alternative mechanisms for providing this support. A limited review of international practices was conducted as part of the evaluation; however, this review was not sufficiently in-depth to suggest alternative mechanisms for the Secretariat to explore.

The purpose of the evaluation was to assess the relevance, effectiveness, and economy of the Treasury Board submission process, with a focus on the following issues:4

- Relevance-Does the Treasury Board submission process address a demonstrable need, is it appropriate to the federal government, and is it responsive to the needs of Canadians?

- Effectiveness-To what extent has the Treasury Board submission process achieved its expected outcomes?

- Economy-Does the Treasury Board submission process consume the minimum amount of resources required to achieve its expected outcomes?

The research for this evaluation was conducted between November 2008 and March 2009.

2. Background

(a) Change Agenda

The Change Agenda, an initiative launched in 2007, is the Secretariat's plan for building management excellence across the federal government by refocusing its relationship and the manner in which it conducts business with other federal organizations. Through the Change Agenda, it is expected that the Secretariat will demonstrate leadership in management excellence, while taking a more strategic and less transactional approach to federal organizations. The efficiencies gained from such an approach would allow for a greater focus on higher value-added activities, would improve relationships with federal organizations, and would result in better advice to Treasury Board ministers. Although not a subject of this evaluation, the Change Agenda is integral to the Treasury Board submission process because it addresses how the Secretariat's business is conducted.

(b) Treasury Board submissions

Treasury Board submissions are one of the three main documents, besides Memoranda to Cabinet (MC) and GIC submissions, that support the formal decision-making process in government.

Legislation, Treasury Board policies, or other Cabinet decisions usually establish the requirements for Treasury Board approval.5 While Treasury Board submissions may relate to any of the Treasury Board responsibilities outlined in the FAA, typical examples of submissions include seeking:

- authority to allocate resources previously approved by Cabinet or included in the federal budget;

- authority to make grants or contributions or approval of terms and conditions of grant and contribution programs;

- recommendations of approval of orders in council (OIC) with resource or management implications;

- authority to carry out a project or initiative the costs of which would exceed a minister's delegated authority;

- authority to enter into a contract above or outside a federal organization's or minister's authority; or

- exemption from a Treasury Board policy.

It should be noted that the Treasury Board submission process has many links to the government's budget, Estimates, and supply processes. For instance:

- Federal organizations are required to develop Treasury Board submissions to obtain approval of the specific authorities and resources required to implement initiatives announced in the federal budget.

- Key elements of many Treasury Board submissions are requests for spending authority to be included in the Main and Supplementary Estimates, which are the mechanisms for seeking supply from Parliament.

- The recent renewal of the expenditure management system and the associated Treasury Board submissions requesting authority to carry out the results of the strategic review exercises and reallocate resources from low-priority and low-performing programs to higher priorities are also linked to the budget, Estimates, and supply processes.

Treasury Board submissions are divided into "Part A" and "Part B" submissions. All Treasury Board submissions (including strategic reviews) are considered "Part A" submissions with the exception of OICs requiring Treasury Board recommendation. "Part B" submissions are therefore those with OIC attached. As a result, the process, procedures, and relevant actors for "Part A" and "Part B" submissions differ. While OICs are legislative instruments, Treasury Board submissions are a mechanism used by a legal body, Treasury Board.

(c) Current Treasury Board submission process

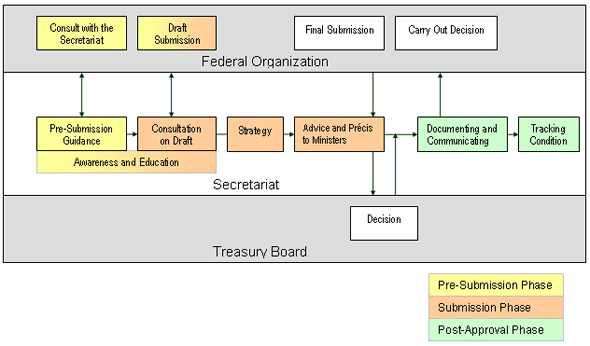

What is generally referred to as the "Treasury Board submission process" in fact incorporates three phases: pre-submission, submission, and post-approval (depicted in Figure 1).

The pre-submission phase begins when a federal organization contacts the Secretariat either to seek guidance on whether a submission is required or to give notice that it intends to make a submission. Even when a federal organization is simply giving notice of its intent to put forth a submission, the Secretariat may provide its advice on whether or not the submission is in fact necessary. Strictly speaking, there is no Treasury Board submission at this point. Nevertheless, the evaluation-reflecting general practice within government-treats the related activities as being part of the submission process.

The submission phase covers the period between when a decision is taken by the federal organization to prepare a submission and the point at which the submission is considered at a Treasury Board meeting. This phase includes the draft submission stage in which program analysts, along with their managers, act as the single window to provide advice to representatives of federal organizations, including advice from Centre of Expertise (COE) analysts. It also includes the final submission stage in which a pr�cis is prepared and discussed at the Strategy Committee, a senior governance body chaired by the Secretary of the Treasury Board. The Strategy Committee, which is part of Secretariat-wide due diligence and oversight, enables the provision of considered, coherent, and consolidated advice to Treasury Board ministers. The committee meets frequently and reviews all submissions and associated risk assessments and advice.

The submission is then presented to the Treasury Board for consideration and approval. At this point, Secretariat advice on risks and considerations is also presented to ministers.

The post-approval phase covers actions taken by the Secretariat following approval of a submission, such as communicating the decision to the federal organization, communicating conditions (if any) attached to the submission, and monitoring these conditions.

Figure 1: Treasury Board Submission Process

As noted earlier, the Change Agenda is integral to the Treasury Board submission process. The Secretariat in fact performs several of the roles described in the Change Agenda throughout the submission process. In the pre-submission phase, the Secretariat assumes its enabler role when providing the federal organization with guidance and advice. In the submission phase, the Secretariat challenges the submission. However, once a submission is ready to be presented to Treasury Board, the Secretariat shifts to its support role, providing the best advice and recommendations to Treasury Board ministers. This shift in the Secretariat's role is necessary in the Canadian federal government model6 because the Secretariat both assists the client department in drafting the submission and ensures that the assistant secretary presenting the submission to Treasury Board is well-equipped with the best possible advice to support the recommendation.

The Treasury Board submission process is a deliberate and iterative process, at times involving intensive discussion and negotiation between the Secretariat and federal organizations as well as discussion within the Secretariat itself. Given the Secretariat's single-window approach, much of the process is coordinated by the Secretariat program sector that is responsible for the federal organization's portfolio7 and remains the primary point of contact.

While the program analyst plays the lead role in relation to the client department, many Secretariat sectors, apart from the related program sector (e.g. the Expenditure Management Sector (EMS), the Office of the Comptroller General (OCG), and various policy centres), typically get involved in reviewing draft submissions and formulating advice to Treasury Board ministers. Analysts from these sectors, COE analysts, play a substantially different role than program analysts: they review and provide feedback on the sections of a submission that pertain to their area of expertise and policy mandate.

Following review of the submission, the program analyst drafts a pr�cis, which is essentially the Secretariat's opinion and advice meant for Treasury Board ministers. The pr�cis includes a summary of the federal organization's request, risk assessment against pre-established risk criteria (which are described in the Guide8), and a recommendation to Treasury Board to either approve, not approve, or approve with conditions the proposals put forth in the submission.

Upon consideration of the Treasury Board submission and Secretariat advice, Treasury Board ministers may attach further conditions to a submission beyond those proposed by the Secretariat or may request follow-up from the federal organization or the Secretariat on a particular issue. For example, a condition may relate to the time frame in which to conduct a formal evaluation of a program.

How risk is handled in the Treasury Board submission process

The Guide states that federal organizations should "provide details of specific risks that need to be managed, measures proposed to mitigate those risks, and any residual risks." Beyond this, it becomes the responsibility of Secretariat analysts9 to assess submissions based on a standardized risk framework that includes the following general risk categories:

- complexity of implementing the proposed program;

- robustness of the organization's structures, accountabilities, and management regimes to successfully deliver the proposal;

- previous issues encountered or current issues that will be raised by proceeding with the proposal; and

- financial risk of proceeding with the proposal.

Before preparing the pr�cis, the Secretariat assigns a risk rating-low, medium, high, or very high-to each of these categories as well as an overall risk rating to the submission. The risk ranking is discussed by Secretariat senior management at the strategy meeting and adjusted if required. It serves to frame Secretariat recommendations and advice to Treasury Board ministers.

(d) Treasury Board submission process - One element in a larger process

The Treasury Board submission process is one element in a larger process that involves federal organizations obtaining approval to undertake new initiatives or to continue with existing ones. The following description of this larger process is simplified and does not pretend to cover all cases; however, it is adequate for setting the Treasury Board submission process within the larger context.

Federal organizations undertake their own process of policy development through research and consultation, both internally and interdepartmentally, and ensure that any proposed initiative supports one or more of its substantive policy objectives and is consistent with its mandate. At the end of this developmental process, the sponsoring minister seeks approval for the new initiative. The primary document used for this purpose is the MC. The MC is the vehicle through which the minister proposes and explains the organization's new initiative to Cabinet, including related options and considerations, and obtains its approval.

The MC gives Cabinet an overview of the proposed new initiative's objectives and financial implications and of the links between the recommended course of action and the government's policies and objectives. It includes a communications plan. Central agencies such as the Privy Council Office (PCO), the Department of Finance Canada, and the Secretariat all have roles to play in the MC process.

PCO is responsible for the MC process and it advises the federal organization on, among other things, whether the aims of the initiative described in the MC are consistent with government priorities. The Department of Finance Canada supports PCO by providing advice and guidance on the MC's fiscal information to ensure that it fits with the government's fiscal priorities. The Secretariat, in its supporting role, helps ensure that the implementation requirements are realistically stated, that the MC includes appropriate accountability and transparency provisions, that it is consistent with Treasury Board policy, and that it makes appropriate linkages between the proposal and other existing programs and federal organizations.

A Cabinet policy committee considers the MC and recommends whether the proposal should be referred to Cabinet for ratification. The MC may either be fully approved as presented, approved in principle, postponed pending clarification, or approved with changes. After the MC has been ratified by Cabinet, the sponsoring federal organization develops a Treasury Board submission to obtain the specific authorities10 needed to implement Cabinet's decision.

The fundamental distinction between an MC and a Treasury Board submission is that, while an MC focuses primarily on the policy rationale and overall funding for a new policy or program initiative, the Treasury Board submission provides details on program design, specific costs, expected results and outcomes, and program delivery and implementation. The Treasury Board submission transforms policy rationale and objectives into a program that will achieve those objectives. It details how the federal organization will carry out the policy initiative; why the proposed method of implementation is the best one; how the proposal ensures accountability and transparency; what the expected outcomes and deliverables are, as per the organization's Management, Resources, and Results Structure (MRRS); and how the federal organization will conduct monitoring, performance measurement, and evaluation to ensure the program is meeting its policy objectives. This includes progress reports on outcomes, projected efficiency, timelines, and cost targets. The Treasury Board submission may also seek approval for expenditure authority, contract authorities, or transfer payment authorities.

3. Scope of the Evaluation

The scope of this evaluation was limited to the current submission process and did not include an assessment of the process against potential alternative mechanisms for providing this support. A limited review of international practices was conducted as part of the evaluation; however, this review was not sufficiently in-depth to suggest alternative mechanisms for the Secretariat to explore.

The evaluation covered all steps of the current submission process involving the Secretariat:

- the support that the Secretariat provides to federal organizations;11

- guidance developed by the Secretariat, such as that found in A Guide to Preparing Treasury Board Submissions (the Guide);

- the communication of decisions regarding submissions; and

- the tracking of conditions placed on approved submissions.

The evaluation did not include federal organizations' internal processes for preparing Treasury Board submissions. Furthermore, the evaluation covers only "Part A" submissions. MCs, GIC submissions, and the federal budget, though outside the scope of the evaluation, were considered to the extent that they provided contextual information.

Canada's Economic Action Plan

The evaluation's planning and data collection phases were already completed at the time Canada's Economic Action Plan was announced in late January 2009. As a result, implementation of this stimulus package could not be included within the scope of the evaluation.

4. Contextual Issues

(a) Volume and complexity of submissions

Between 2004 and 2009 (September to August calendar), an average of 804 Treasury Board submissions were made each year. It should be noted that the Secretariat itself usually accounts for the largest number of Treasury Board submissions among all federal organizations given that it acts as both a department and the management board of the federal public service. As such, some of the Secretariat's submissions are to seek approval or amendments to Treasury Board policies or are related to Treasury Board's role as employer.

As shown in Table 1, the Secretariat's program sectors, with the exception of the International Affairs, Security and Justice Sector, reported a higher incidence of "standard" submissions than "complex" ones.12 Though in the minority, figures for complex submissions are nevertheless significant.

| Program Sector | % Standard | % Complex |

|---|---|---|

| Social and Cultural | 54.9 | 34.3 |

| Economic | 48.7 | 38.1 |

| International Affairs, Security and Justice | 41.7 | 53.2 |

| Government Operations (program side) | 66.0 | 29.9 |

| Overall Average | 54.2 | 38.4 |

Evaluation participants described standard submissions as follows:

- clear and straightforward;

- low risk;

- having a relatively simple policy context;

- written by federal organizations that have a track record of relatively problem-free submissions; and

- involving stakeholders with a relatively common set of interests and priorities.

Complex submissions were said to involve one or more of the following:

- wide-ranging proposals;

- multiple or unclear accountabilities;

- requests for exemptions from government policies;

- significant legal issues;

- outstanding policy issues;

- horizontal initiatives involving multiple federal organizations;

- complicated governance mechanisms;

- relatively large amounts of public funding;

- sensitive media considerations; and/or

- implications for a range of regions and/or jurisdictions across the country.

(b) Logic model for the Treasury Board submission process

No logic model had previously been developed for the Treasury Board submission process. A logic model is essential to this (and to any) evaluation, because it describes the consensus among key stakeholders on the intended outcomes of the Treasury Board submission process. A consensus view on outcomes is the touchstone against which the evaluation must be conducted. Relevance, effectiveness, and economy cannot be assessed in a vacuum; rather, these terms only have meaning in relation to the ultimate outcome of the submission process.

It was therefore necessary for the evaluation team to develop a logic model that would provide the necessary foundation for the evaluation. Consultations were held to gather information on the intended outcomes of the Treasury Board submission process. The evaluation team interviewed 19 individuals from areas across the Secretariat who deal with Treasury Board submissions, including analysts and senior analysts, directors, and an assistant secretary. In addition, two working sessions were held with Secretariat analysts to develop and validate the logic model and evaluation matrix that had been developed by the evaluation team. The consensus among this group was that the ultimate outcome of the submission process was to support Treasury Board in making decisions that contributed to ensuring that programs and spending are aligned with the government's priorities.

Consultation with senior management provided another perspective. Participants in the Assistant Deputy Minister (ADM) Working Session observed that ensuring alignment of new initiatives with the government's priorities is the intended outcome of the MC process rather than the Treasury Board submission process. They suggested that the purpose of the Treasury Board submission process was to provide federal organizations with the resources and authorities needed to achieve the social and economic outcomes desired by Cabinet and to ensure that the programs delivered demonstrated value for money. This proposed ultimate outcome appears to be consistent with the Secretariat's documentation and communications about its expected results. The statement is consistent with the Secretariat's strategic outcome: "Government is well managed and accountable, and resources are allocated to achieve results." This ultimate outcome is also consistent with the expected results outlined in the Secretariat's 2008-09 Departmental Performance Report (DPR): "allocation of resources so that they are aligned with the government's priorities and responsibilities, thereby ensuring that federal programs are effective and efficient and provide value-for-money." The link to broader outcomes (e.g. social and economic) is captured in the DPR's reference to "alignment of government's priorities and responsibilities."

Given that the Treasury Board submission process is not limited to either a single Secretariat subactivity or one organization within the Secretariat, instead crossing a number of organizations, including the program sectors, EMS, and many policy Centres of Excellence, it is perhaps not unexpected that a logic model for the process did not exist before the evaluation and that the ultimate outcome of the Treasury Board submission process was therefore not defined. That said, the evaluation found that there is a sound basis for articulating the outcome, particularly from the strategic outcome and expectations articulated in the Secretariat's DPR. The need for a final logic model, including the ultimate outcome, is addressed in the Conclusion section of this report.

For the purposes of the evaluation, outcomes of the Treasury Board submission process were based on analysis of the information gathered from the consultation sessions as well as information found in documentation on the submission process. The Guide was examined, and while it is very detailed in terms of how to do Treasury Board submissions, it is less explicit about why they must be done. Nevertheless, it was possible to make inferences about the ultimate outcome based on other statements found in the Guide. The Guide's clearest statement about the ultimate outcome of the submission process is as follows:

The Treasury Board submission transforms policy rationale and objectives into a program that will achieve those objectives. It details how the federal organization will carry out the policy /initiative; why the proposed method of implementation is the best one; how the proposal contributes to government-wide aims such as accountability, transparency, and interoperability of information; what the expected outcomes and deliverables are, as per the organization's Management, Resources, and Results Structure (MRRS);13 and how the federal organization will conduct monitoring and evaluation to ensure the program is meeting its policy objectives. This includes progress reports on outcomes, projected efficiency, timelines, and cost targets.

Although reference may be made to the MC and Cabinet decisions, it is generally unnecessary to repeat the policy rationale in a submission. The submission must nevertheless be consistent with the Cabinet decisions.14

In other words, questions of policy rationale and intended social and economic outcomes (or "objectives") are dealt with in the MC (as was suggested by participants in the ADM Working Session). The Treasury Board submission deals with more detailed questions of program design and implementation. It is therefore reasonable to infer that the ultimate value or outcome of the submission process has to do with ensuring that the initiative in question is well designed in relation to the policy rationale described in the MC and in terms of its implementation arrangements and its reporting, accountability, and control mechanisms. The evaluation team therefore proposed the following as the ultimate outcome for the Treasury Board submission process:

Program implementation serves the policy outcomes defined by Cabinet in the most economical manner possible and satisfies the government's obligations for transparency, accountability, and prudence.

It was not possible to validate this proposed ultimate outcome with an appropriate cross-section of stakeholders. The evaluation team therefore recognizes that it is simply a place holder for the purposes of the evaluation.

On the other hand, the other elements of the logic model proposed by the evaluation team-the immediate and intermediate outcomes and the outputs-do reflect the common view within the Secretariat.

The involvement of the Secretariat in the submission process consists of six major components, as outlined in the logic model developed by the evaluation team for the purposes of the evaluation (Appendix A; see also Figure 1):

- raising awareness about the Treasury Board submission process among both Secretariat analysts and personnel in federal organizations;

- providing guidance to federal organizations before they enter into the submission process;

- reviewing and providing advice or consulting on draft submissions put forward by federal organizations;

- drafting the submission pr�cis and preparing for the Treasury Board meeting;15

- documenting and communicating the Treasury Board decision; and

- tracking implementation of conditions that Treasury Board may have placed on its approval decision.

The activities identified in the middle row of Figure 1 should lead to the outcomes indicated in the logic model developed by the evaluation team:

- Secretariat analysts and the personnel in federal organizations who are involved in preparing Treasury Board submissions having an increased understanding of Treasury Board submissions and related policies;

- content of submissions being consistent with relevant authorities and policies;

- Treasury Board decisions on the submissions put forth being well informed; and

- post-decision procedures being in place to follow through on the Treasury Board decision (e.g. communication to EMS, tracking of conditions, communication to federal organizations).

The foregoing outcomes are expected to result in high-quality Treasury Board submissions. These in turn are expected to contribute, ultimately, to federal organizations' effective implementation of programs that serve the government's desired policy outcomes in the most efficient possible manner while also fulfilling the government's obligations for transparency, accountability, and prudence.

5. Evaluation Issues and Methodology

Table 2 presents the evaluation issues and questions that were derived from the logic model developed by the evaluation team. The detailed evaluation matrix, which outlines the indicators and data sources used to address the evaluation questions, is presented in Appendix B.

| Evaluation Issue | Evaluation Questions |

|---|---|

| Relevance |

|

| Effectiveness |

Short Term

|

| Economy |

|

(a) Data sources and methods

The evaluation framework uses multiple lines of evidence and complementary research methods to ensure the reliability and validity of the data. The following research methods were used:

- document review;

- interviews with stakeholders and experts;

- a working session with assistant secretaries from the Secretariat and ADMs from selected federal organizations (ADM Working Session);

- review of administrative, financial, and statistical data; and

- a survey of analysts at the Secretariat and in federal organizations.

Each of these methods is described in more detail below.

Document review. Three main types of documents were reviewed during the evaluation:

- general background documentation (e.g. documents describing the Treasury Board submission process’s history, rationale, and legislative framework);

- documents specific to the submission process (e.g. the Guide and other related documents, such as the Analyst Survival Guide, and information on relevant committees, branches, and other groups involved in the process); and

- past studies (e.g. research specific to the Treasury Board submission process, international studies).

For the full list of documents reviewed, please see Appendix C. Note that the evaluation did not review or assess Treasury Board submissions and pr�cis for quality.

Interviews. Twenty-six interviews were completed (Table 3 and Appendix D). Interviewees included

- program analysts and COE analysts:18

- program analysts are the main point of contact for a submission; and

- COE analysts represent sectors within the Secretariat (e.g. Chief Information Officer Branch, Corporate Services Sector, EMS) and provide policy advice to program analysts.

- representatives from 12 selected federal organizations that put forward a Treasury Board submission within the last five years. Four interviews were conducted with federal organizations that fall into each of the following categories:

- occasional submitters (less than one submission per month);

- moderate submitters (one to two per month); and

- heavy submitters (three or more per month).

- external stakeholders, meaning individuals who are close to but not directly involved in the Treasury Board submission process (e.g. individuals from the Privy Council Office and from the Department of Finance Canada).

| Interview Group | Number of Interviews |

|---|---|

| Program analysts and COE analysts | 11 |

| Representatives from federal organizations | 12 |

| External stakeholders | 3 |

| Total | 26 |

All interviews were conducted by telephone. Interviewees were sent an interview guide (see Appendix E) before the interviews were conducted.

Survey. A survey was administered over the Internet to program analysts, COE analysts, and representatives of federal organizations that put forward a Treasury Board submission in the last five years. A total of 547 individuals were asked to complete the questionnaire; 220 useable responses were received, for an overall response rate of 40% (see Table 4).19

| Survey Group | Total Sent | Received | Removed | Total Kept | Response Rate | Confidence Interval |

|---|---|---|---|---|---|---|

| Program analysts | 135 | 60 | 0 | 60 | 44.4% | 95% � 9.5% |

| COE analysts | 181 | 66 | 0 | 66 | 36.5% | 95% � 9.6% |

| Federal organizations | 231 | 99 | 5 20 | 94 | 40.7% | 95% � 7.8% |

| Total | 547 | 225 | 5 | 220 | 40.2% |

All of the Secretariat's program analysts were invited to participate in the survey. They were also asked to provide contact information for all COE analysts they had consulted for advice on Treasury Board submissions during the last five years. Furthermore, the program analysts were asked to provide contact information for the individuals in federal organizations (including the Secretariat) that put forward a submission within the last year. Federal organizations were encouraged to forward the survey to any individual within the organization who had been involved in the Treasury Board submission review process.

Survey results are provided in Appendix G.

Working session with ADMs. A two-hour working session was conducted to gather qualitative information on the relevance, effectiveness, and economy of the Treasury Board submission process. Assistant secretaries from the Secretariat and selected ADMs responsible for corporate and/or strategic planning as well as selected departmental chief financial officers (CFO) from federal organizations were invited to participate. The issues to be discussed during the session (see Appendix F) were provided to the participants in advance.

Administrative, financial, and statistical data. Administrative, financial, and statistical data were gathered for the purpose of assessing the effectiveness and efficiency of the submission process. The evaluation team worked with the Treasury Board Submission Centre to review data related to Treasury Board submissions and to gain a greater understanding of the Submission Tracking System (STS). The evaluation team also reviewed data from the Management Accountability Framework (MAF) database.

Costing. Evaluating economy requires an analysis of the costs involved throughout the submission process. A costing exercise was undertaken; however, because direct costs related to Treasury Board submissions are not tracked separately, only the level of effort of some participants involved in the submission process was available. Section 6(c)(i), "Resources allocated to the submission process," therefore does not identify an estimated cost for the process.

Related international practice: The evaluation team undertook a limited review of submission process models used in other international jurisdictions.21 Given the cursory nature of this review, the evaluation team could not draw conclusions on the appropriateness of other models compared to the Canadian context. Findings from this review are therefore not presented in this report, though some interesting information was discovered during the review. For example, the role played by the Secretariat's assistant secretaries-whereby they present a federal organization's submission to Treasury Board-may be unique internationally. As is the case in the Canadian federal model, Secretariat equivalents in other jurisdictions are responsible for logistical and technical functions related to sessions of Cabinet, strategic and work planning, policy advice, legal functions, some monitoring functions, and their own internal management functions.22 They scrutinize material presented to Cabinet, ensuring that legal and policy considerations have been accounted for within structured submissions. In six of ten surveyed Organisation for Economic Co-operation and Development (OECD) countries,23 the Secretariat equivalent prepares a recommendation on how the submission should be handled in the Cabinet-level meeting. In these jurisdictions, however, it is the deputy minister of the submitting organization who presents the submission at the Cabinet-level meeting and not the equivalent of a Secretariat assistant secretary. Assistant secretary equivalents can therefore focus their attention on submissions that are most strategic or sensitive or for which their recommendation runs counter to that of the submitting organization.

Other information. Once the data were collected and analyzed, information gaps were discovered in a few key areas. To fill these gaps, the following methodologies were used:

- Review of additional human resources (HR), financial, and statistical data—The evaluation team reviewed additional HR and financial data to gain further insight into the cost of the Treasury Board submission process. Documentation on program sector boot camps was also reviewed.

- Interview with a senior advisor from the Secretariat—The evaluation team met with a senior advisor who has extensive knowledge of and experience with the submission process and its related management tools and structure.

- Working sessions with program directors—Four sessions were held with the Secretariat’s Program Directors Group (PDG) to validate findings. In addition, assistant secretaries from the program sectors reviewed the final draft of this report.

- Interviews with Expenditure Management Information System (EMIS) business analysts—The intent of the meetings was to gain additional knowledge and a greater understanding of the Secretariat's Budget Office Systems Renewal (BOSR) Project and the change management work that occurred during implementation of EMIS.

(b) Limitations of the evaluation

Time frame. A federal election was called shortly after the evaluation was launched. Not long after the election, Parliament was prorogued. These events delayed approval for the opinion research to be conducted for the evaluation; consequently, the time available to perform the research was limited. Another consequence of the election and subsequent prorogation was that the evaluation team could not interview Treasury Board ministers regarding the support they receive through the Treasury Board submission process.

Logic model. While the evaluation team believes that the ultimate outcome proposed in the logic model it developed is a valid description of the purpose of the Treasury Board submission process and therefore a valid basis for the evaluation, it was not possible to validate the ultimate outcome with an appropriate cross-section of stakeholders.

Review of performance measurement data. Performance data have not been collected on all aspects of the Treasury Board submission process. For instance, data are not collected on the extent to which the Treasury Board submissions officially submitted by federal organizations are actually required, or their compliance with policies and processes, and on the extent to which Treasury Board decisions reflect recommendations in the pr�cis. In the absence of this information, the evaluation team was unable to assess the quality of submissions and pr�cis. The evaluation therefore relied more heavily on survey and interview data to assess the effectiveness of the process.

Administrative data. Limited administrative data were available on the submission process and its results. Furthermore, as noted in the Treasury Board of Canada Secretariat Audit of Leave and Overtime (2008),24 some overtime data are not reliable, thereby limiting the extent to which the evaluation team could use such data to assess the amount (and related costs) of overtime claimed by program analysts in connection with Treasury Board submissions. In addition, other administrative data such as the number of days between the Treasury Board decision and the issuance of the decision letter would have provided additional lines of evidence.

Surveys and interviews. Given the highly variable nature of Treasury Board submissions, it stands to reason that the submission process experience would differ significantly from one submission to the next. More interviews would have provided better data on the effect of variations in a submission's size, scope, value, and complexity. The evaluation methodology attempted to address this limitation by inviting individuals from all federal organizations to participate in the Web-based survey. The results of the survey were cross-validated with the interview responses.

Costing methodology. Cost information to support a complete and accurate costing of the Secretariat's involvement in the Treasury Board submission process was not available.

Single-window approach to service delivery. Because the Secretariat uses a single-window approach for submissions, in which program analysts and their directors or executive directors are the point of contact for representatives from federal organizations, interaction between COE analysts and representatives from federal organizations is extremely limited. As a result, despite COE analysts having a clear role and contribution at the pre-submission and draft stages of the submission process, representatives from federal organizations may not be fully aware of the extent of this role. This may have led to the evaluation's greater focus on program analysts.

While there are some limitations with the evaluation methodology, multiple lines of evidence were used to draw conclusions about the Treasury Board submission process, strengthening the reliability and validity of the evaluation results. Despite the limitations, the methodology meets the requirements of the Treasury Board Policy on Evaluation and associated standards.

6. Findings

(a) Relevance

Does the Treasury Board submission process address a demonstrable need, and is it appropriate to the federal government?

The Treasury Board submission process aligns well with the Secretariat's strategic outcome: "Government is well managed and accountable, and resources are allocated to achieve results."25 This strategic outcome is consistent with the responsibilities of Treasury Board ministers as set out in the FAA and therefore speaks to the role of the Secretariat in providing advice and recommendations to Treasury Board ministers through the Treasury Board submission process. The need for a Treasury Board submission process to support ministers is particularly relevant, given the recent focus on responsible spending and the renewal of the expenditure management system, which includes the strategic review of the direct program spending of all departments and agencies of the Government of Canada to reallocate funds from low-priority and low-performing programs to higher priorities.

The Guide states the following:

Improving the quality of information and accountability for results are key elements of the new approach to managing spending across government. The new approach supports managing for results by establishing clear responsibilities for departments to better define the expected outcomes of new and existing programs. It supports decision making for results by ensuring that all new programs are fully and effectively integrated with existing programs and by reviewing all spending to ensure efficiency, effectiveness, and ongoing value for money. Finally, it supports reporting for results by improving the quality of departmental and government-wide reporting to Parliament.26

This excerpt describes the "demonstrable need" that the Treasury Board submission process is meant to address. Essentially, for good management of public programs, the government requires rules, practices, and processes that:

- establish clear responsibilities for federal organizations to define expected outcomes;

- ensure all new programs are well integrated with existing programs;

- ensure all spending is consistent with the government’s commitment to achieving efficiency, effectiveness, and value for money; and

- improve the quality of departmental and government-wide reporting to Parliament.

In assessing relevance, the key evaluation issue is therefore whether or not the Treasury Board submission process is capable of meeting these requirements. The question of whether it actually meets these requirements is addressed under the assessment of effectiveness. The question of whether, and to what extent, other processes or mechanisms would be capable of meeting these requirements is outside the scope of this evaluation.

The documents reviewed for this evaluation, as well as the interviews conducted, point to the conclusion that the Treasury Board submission process is relevant to the government's "demonstrable needs" for good public management. As noted above, the submission process aims to ensure that minimum standards are met with regard to:

how the federal organization will carry out the policy initiative; why the proposed method of implementation is the best one; how the proposal contributes to government-wide aims such as accountability, transparency, and interoperability of information; what the expected outcomes and deliverables are, as per the organization's Management, Resources, and Results Structure (MRRS); and how the federal organization will conduct monitoring and evaluation to ensure the program is meeting its policy objectives. This includes progress reports on outcomes, projected efficiency, timelines, and cost targets.27

According to the interviews, general perceptions about the purpose of the submission process broadly correspond to this formal description from the Guide.

This formal description of the Treasury Board submission process is well aligned with the government's stated needs for good public management.

(b) Effectiveness

To what extent has the Treasury Board submission process achieved its expected outcomes?

Ideally, this evaluation would assess the effectiveness of the Treasury Board submission process in relation to its impact on the ultimate outcome in the logic model that the evaluation team developed for the purposes of the evaluation, i.e. "program implementation serves the policy outcomes defined by Cabinet in the most economical manner possible and fulfills the government's obligations for transparency, accountability, and prudence." However, attempts to link the Treasury Board submission process directly to this ultimate outcome would face data-gathering and methodological challenges that could not be addressed within the evaluation's scope and its time and resource constraints. The evaluation's assessment of the effectiveness of the Treasury Board submission process is therefore focused on the immediate and intermediate outcomes specified in the logic model developed by the evaluation team. If the evaluation finds that the Treasury Board submission process is generally effective in contributing to these outcomes, then it would be reasonable to conclude that the submission process is also making a significant contribution to the ultimate outcome.

The evaluation therefore focused on the following questions:

- Have federal organizations and Secretariat employees demonstrated, over the years, an increased understanding of the elements of Treasury Board submissions, policies, and processes?

- Does the Secretariat offer services that enable federal organizations to put forth draft submissions that comply with Treasury Board authorities, policies, and directions?

- Does the Secretariat’s review process for Treasury Board submissions ensure that they comply with government authorities and policies?

- Are Treasury Board decisions well-informed and consistent with the advice, guidance, and recommendations of Secretariat analysts?

- Are mechanisms in place to ensure Treasury Board decisions are carried out?

- What is the level of quality of Treasury Board submissions?

(i) Understanding of the Treasury Board submission process (evaluation question 1)

The majority of survey participants in all three categories (83.3% of program analysts, 76.9% of COE analysts, and 83% of representatives from federal organizations) believed they had a strong understanding of the Treasury Board submission process. There was no correlation between the length of time respondents had been in their job and their perception of their own understanding of the process.

Survey respondents rated their counterparts' understanding of the Treasury Board submission process less favourably than they rated their own (Table 5). For example, 83% of federal organization respondents believed they had a strong understanding of the process, whereas less than 50% of the program analysts surveyed agreed that this was true. There was a similar divergence of opinion between program and COE analysts within the Secretariat. Each group identified a need for more training for the other.

| % Agreed | Program Analysts | COE Analysts | Federal Organization Respondents |

|---|---|---|---|

| I have a strong understanding of the Treasury Board submission process. | 83.3 n=60 |

n/a | n/a |

| I have a strong understanding of the elements of Treasury Board submissions, policies, and processes. | n/a | 76.9 n=65 |

83.0 n=94 |

| The federal organizations I work with have demonstrated, over the years, an increased understanding of the elements of Treasury Board submissions, policies, and processes. | 48.3 n=58 |

n/a | n/a |

| Program analysts I work with have demonstrated, over the years, an increased understanding of the elements of Treasury Board submissions, policies, and processes. | n/a | 50.0 n=62 |

n/a |

Notwithstanding the above, it should be noted that among the 12 interviews conducted with federal organizations, all 4 federal organizations with high submission rates believed that their analysts had a strong understanding of the Treasury Board submission process. Results were mixed among federal organizations with moderate and low submission rates; they indicated that the level of understanding varied depending on the analyst assigned to them.

HR and survey data showed that approximately two-thirds of program analysts had been in their position for two years or less, which may at least partially explain the external perceptions about program analysts' understanding of the submission process.

(ii) Quality of Secretariat tools, support, and services (evaluation questions 2 to 5)

Training. To assess the Secretariat's tools, support, and services, the evaluation team examined documentation on the boot camps held for program analysts and its guidance document on Treasury Board submissions, A Guide to Preparing Treasury Board Submissions. Furthermore, the evaluation team asked whether courses on the Treasury Board submission process were taken from the Canada School of Public Service.

The Secretariat offers program sector boot camps, which have received positive overall ratings and are considered useful in terms of providing a general overview of what program analysts should know. However, in the participant feedback forms that are completed following the boot camps28 and in interviews, Secretariat analysts indicated that the boot camps are not offered often enough and their duration (two days) does not allow for sufficient coverage of the Treasury Board submission process. As one boot camp participant noted, "could… have more hands-on training."

Evaluation participants also indicated that:

- The Secretariat's Guide to Preparing Treasury Board Submissions is viewed as a useful tool.

- The Canada School of Public Service offers courses on the Treasury Board submission process. Although only a third or fewer federal organization representatives attended them, the majority found the courses to be useful. Those who did not attend the courses indicated cost and waiting lists as being the main barriers.

- The Secretariat itself offers learning events on the Treasury Board submission process to federal organizations. Some of the Secretariat's sectors offer them as frequently as four times per year. A detailed examination of these was not undertaken.

Relationship between Secretariat analysts and federal organizations. Survey results demonstrated that efforts are being made to foster a positive working relationship between program analysts and federal organizations. Almost all of the program analysts surveyed (91.6%) reported that they maintain regular contact with federal organizations regardless of whether a submission is currently being developed or processed. All of the program analysts interviewed stated that they have positive and productive relationships with federal organizations. It is worth noting, however, that when asked how they would characterize this relationship, Secretariat analysts did not refer to the three roles-enabler, challenger, and champion-defined in the Change Agenda.

Federal organizations, for their part, indicated that their relationships with program analysts were generally good or had improved. Nearly all federal organization respondents said they knew whom to consult at the Secretariat with respect to their submissions.

Appropriateness29 of Treasury Board submissions put forward. Secretariat analysts have a role to play at the pre-submission stage when federal organizations are considering proceeding with a submission. At the outset, federal organizations may want early feedback to confirm the directsion of their intended submission or to confirm that a submission is in fact necessary. According to the interviews, 58% of federal organizations seek pre-submission assistance, especially when the submission is complex or perceived as higher risk.30 Advice provided by the Secretariat at the pre-submission stage is intended (among other things) to help federal organizations make informed decisions about whether or not to put forth a submission. The assumption is that in the absence of such advice, federal organizations would proceed with a greater proportion of unnecessary submissions, creating a burden on the Secretariat and Treasury Board and reducing the efficiency of the submission process. The appropriateness of submissions was therefore regarded as an indicator of the suitability and quality of the services the Secretariat provides at the pre-submission stage.31

Secretariat analysts were asked about the appropriateness of submissions (Table 6 32).33 Approximately 40% of the program analysts surveyed responded that they received draft submissions at the pre-submission stage (for preliminary guidance) for initiatives that did not in fact require a submission. The views of COE analysts were similar.

| Was the Secretariat consulted prior to sharing? | COE analysts | Program analysts |

|---|---|---|

| n = sample size | n=29 | n=24 |

| Yes | 44.8 | 62.5 |

| No | 10.3 | 25.0 |

| Do not know | 44.8 | 12.5 |

| Were any drafts submitted? | COE analysts | Program analysts |

|---|---|---|

| n = sample size | n=65 | n=58 |

| Yes | 10.8 | 19.0 |

| No | 36.9 | 55.2 |

| Do not know | 52.3 | 25.9 |

Secretariat analysts were also asked how often federal organizations put forward draft submissions for formal consideration (as opposed to simply seeking informal feedback on a preliminary draft). At this stage, a much smaller proportion of analysts (19% of program analysts and 10.8% of COE analysts) felt that inappropriate drafts were submitted. The reported drop in unnecessary submissions between the stage at which the Secretariat is providing preliminary guidance and the stage at which a submission is formally put forward suggests that the Secretariat is having a positive impact on reducing the number of inappropriate submissions.

Accuracy, consistency, usefulness, and timeliness of Secretariat advice. Interviewees identified factors they believed had a positive or negative impact on the consistency, accuracy, and timeliness of the advice the Secretariat provides to federal organizations during the submission process.

Factors seen by interviewees as having a positive impact:

- Secretariat analysts having sufficient time to review submissions and understand their context;

- scheduling of weekly teleconferences between the Secretariat and federal organizations;

- availability of both formal and informal validation processes for the submission (i.e., draft submission for formal consideration as opposed to seeking informal Secretariat feedback on a preliminary draft); and

- within federal organizations, availability of a quality assurance process and a database to track advice provided by the Secretariat.

Factors seen by interviewees as having a negative impact:

- high turnover rate among program analysts;

- federal organizations' lack of direct access to COE analysts and lack of information about COE analysts' time requirements to review submissions (as stated in an interview, "The process seems to break down when an analyst needs to consult other analysts....

I received one set of advice and then after the second draft, I received conflicting advice when it went to a different group."); and - program analysts' workload and the consequent limitations on their availability to review submissions (according to one individual, "Capacity...in...TBS, particularly with the new requirements imposed on the TBS analysts such as strategic review, is an important challenge within the Treasury Board submission process. The strategic reviews have created a whole new workload but not been accompanied by new staff.").

Survey respondents were asked whether the submission review process ensures that Treasury Board submissions comply with government authorities and policies. A large majority of respondents from each of the groups agreed that it did (Table 7).

However, when survey respondents were asked whether the services provided by analysts enable federal organizations to put forth draft submissions that comply with Treasury Board authorities, policies and directions, there was a divergence of opinion. The federal organization representatives and program analysts had very similar agreement percentages to the ones for the above question and as shown in Table 7, whereas only 49.2% of COE analysts agreed. This divergence could be a function of program analysts acting as the single point of contact for federal organizations and COE analysts not always being consulted at the pre-submission stage.

Secretariat advice and guidance to federal organizations. Survey results (Table 8) show that the majority of survey respondents from federal organizations agreed that Secretariat analysts were providing consistent, accurate, useful, and timely advice. For those who disagreed, consistency and timeliness of advice had the lowest levels of agreement for both representatives of federal organizations and program analysts. Specifically:

- Slightly over half (55.3%) of the survey respondents from federal organizations agreed that the advice of program analysts is consistent at the submission review stage. Another 27.7% indicated that this is not the case, while the remaining respondents from federal organizations answered neutrally or did not know. The responses of program analysts had a slightly higher level of agreement, with 62.7% indicating that advice was consistent.

- Similarly, 54.3% of representatives of federal organizations agreed that Secretariat analysts were providing timely advice at the review stage, while 22.3% did not agree.

- Almost two-thirds of federal organization representatives agreed that the advice provided by Secretariat analysts is accurate and useful.

It is important to note that the issues around timeliness and consistency of advice are recognized internally by the Secretariat, not only by federal organizations.

Consultations with senior management highlighted the value of the Secretariat's work with federal organizations during the pre-submission stage. However, the following areas were identified as needing improvement:

- Clarity of process requirements—Some federal organizations are unclear as to what is specifically required in their submissions and why this varies from one submission to the next (e.g., at what point a document is considered a "first draft");

- Interpretation of process rules and guidelines—Some federal organizations experienced frustration because of situations where the rules and guidelines of the submission process were being strictly enforced, though not always according to their spirit and intent (e.g. fast-track vs. urgent or late submissions);

- Working relationship between the Secretariat and federal organizations—Pre-submission work could be improved through a strengthened working relationship between program analysts and federal organizations; and

- Accessibility of COE analysts—It was noted that federal organizations' lack of direct access to COE analysts may in some cases inhibit their ability to prepare high-quality draft submissions.

Adequacy of time for input into submission documents. The time required to complete the submission review process can vary greatly depending on a submission's characteristics. The Guide advises federal organizations to allow at least six weeks34 for the submission process and cautions that it is not unusual for the process to last more than six weeks. Survey results (Table 9) indicate that the process normally takes 8 to 10 weeks. This suggests that the Guide sets up unrealistic expectations, which could lead to a frustrating experience for someone who is new to the process.35

Secretariat analysts were asked for their views on whether they had enough time to review draft submissions properly. While not a majority, a significant number of program analysts and COE analysts (42.5% and 49.2%, respectively) said that they did not have enough time.

Participants in the ADM Working Session argued that the fast-track system used by the Secretariat to give priority handling to certain submissions is another factor affecting the time available to Secretariat analysts to review submissions.36 They said that it causes uncontrollable delays for submissions that are not fast-tracked. In discussions with Secretariat senior management, however, it was noted that there is no formal system for fast-tracking submissions. It is nevertheless true that certain submissions may receive priority treatment on an ad hoc basis due to urgent situations that require them to "jump the queue." It is at the discretion of the President of the Treasury Board to determine when a submission should receive priority handling; the decision is normally taken following negotiation with the minister responsible for the submission. Consultations between Secretariat officials and sponsoring federal organizations regarding time sensitivity of their proposals are held regularly; however, decisions regarding priority handling are not normally shared with the federal organizations whose submissions may be displaced as a result.

Extent to which Secretariat analysts' input is reflected in final Treasury Board submissions. Most Secretariat analysts stated that their advice is included in final submissions that go forward to Treasury Board. Some noted that, if their advice was not included, they might recommend that conditions be placed on the submission or a remark be included in the pr�cis. Survey results were similar, with 86.6% of program analysts and 71.2% of COE analysts responding that they felt their advice was reflected in the final submission.

This was confirmed with federal organization representatives, who stated that they include all or almost all of the comments provided by Secretariat analysts. Some noted that if they are in disagreement with the advice, they consult further to resolve the issue. A small minority (18.0%) of federal organization representatives stated that they include Secretariat comments due to time pressures and the perceived power of the Secretariat and not because they are in agreement with them.

Extent to which Treasury Board final decisions reflect Secretariat recommendations. Once the program analyst is satisfied that the submission is complete, he or she prepares a pr�cis that includes recommendations to Treasury Board. The recommendations are discussed and agreed to at the Secretariat's Strategy Committee, which is chaired by the Secretary and includes the participation of assistant secretaries from across the Secretariat. A presentation based on the pr�cis is then made to Treasury Board by the appropriate assistant secretary. Although the Secretariat has no authority over Treasury Board's decisions, the decisions normally reflect its recommendations. Data from the survey of program analysts suggest that Treasury Board decisions are consistent with the Secretariat's recommendations 82.2% of the time.

Information management. Once Treasury Board makes a decision, the Secretariat records the decision and formally advises the deputy minister of the sponsoring organization within fifteen calendar days. Although program analysts have no formal requirement to do so, they will normally advise the federal organization verbally of the Treasury Board decision as a matter of courtesy. This is usually done as soon as possible, generally the day after the Treasury Board meeting.37 While most federal organizations did not have an issue with the timeliness of the communication of Treasury Board decisions, it should be noted that one-third of federal organization representatives did not agree that Treasury Board decisions are communicated to them in a timely manner.

Of the program analysts and COE analysts interviewed, many indicated that they use their own private filing system for Treasury Board submissions. Most keep a hard copy of the decision for a period of time, after which the documents are archived or sent to the Treasury Board Submission Centre. Some analysts did mention using the Records, Documents and Information Management System (RDIMS),38 but most program analysts stated that RDIMS is difficult to use. Senior managers observed that a central repository for submission-related information would greatly facilitate their work.