Archived - Guideline on Cost Estimation for Capital Asset Acquisitions

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

1. Introduction

The Guideline on Cost Estimation for Capital Asset Acquisitions is intended to provide assistance to Government of Canada departments in developing a cost estimate for the acquisitionFootnote 1, construction or development of capital assets; for the betterment of capital assets; or for the acquisition of a group of like assets. It is expected that the level of effort expended to develop a cost estimate will vary with the value of the capital asset and the related risks.

The purpose of this guideline is to:

- Provide guidance on how to develop, report and use cost estimates for decision making; and

- Provide guidance on what cost information should be developed when there is a choice to make between two or more capital assets that meet requirements, or a decision between two or more options for acquiring the use of a capital asset (e.g., purchase, lease or public-private partnership).

2. Effective Date

This guideline takes effect on October 15, 2015.

3. Context

Parliamentarians, ministers, deputy ministers, chief financial officers and senior managers need to make decisions regarding the acquisition of many different capital assets. Understanding the nature of these decisions is essential to determining what cost estimate information should be provided, how the information should be generated, and how it should be evaluated.

In the acquisition of a capital asset, the initial capital outlay is important, but so are the costs associated with the use and ownership of the capital asset over its whole life. These ongoing costs are often greater than the initial outlay and can vary significantly between alternative solutions.

The guidance in this document builds on the principles and steps outlined in the Treasury Board of Canada Secretariat's (TBS) Guide to Costing.

4. Definitions

See Appendix A.

5. Roles of Senior Managers and Chief Financial Officers

Senior Managers

Under the Policy on Financial Management Governance, senior managers (SMs) are responsible for defining program policy direction; accordingly, they have a key role in the development of cost estimates for capital asset acquisitions. This role includes defining the program or operational requirements, defining and articulating framing assumptions, setting ground rules, reviewing assumptions, and ensuring that all affected stakeholders are consulted. SMs are responsible for approving cost estimates and overseeing ongoing management of the capital assets under their control.

When the chief financial officer (CFO) is required to attest to a cost estimate, such as an estimate that is included in a Memorandum to Cabinet (MC) or Treasury Board submission, the responsible SM should ensure the CFO has all of the key information such as framing assumptions, ground rules, cost boundaries, and the whole-of-life cost estimate. The SM should also inform the CFO if changes are made at any point during the acquisition process.

Chief Financial Officers

The role of CFOs in developing cost estimates for capital asset acquisitions includes ensuring that principles and appropriate costing methodologies are used and that risk and uncertainty are clearly described and appropriately reflected in the cost estimates. CFOs also attest to cost estimates contained in MCs or Treasury Board submissions, a responsibility described in the Policy on Financial Management Governance and the Guideline on Chief Financial Officer Attestation of Cabinet Submissions.

When conducting their due diligence reviews, CFOs should ensure that the requested authority limits and funding for acquiring a capital asset take into consideration the level of confidence in the cost estimate. Confidence in cost estimates increases as information improves, risks are assessed, and mitigation strategies are put into place. For this reason, the requested authority limits and funding should account for a higher level of uncertainty in the estimates made earlier in the acquisition process than those occurring later in the process.

Expenditures will vary from an estimate that is not risk-adjusted. A useful point of reference is the fact, expenditures can vary from an un-adjusted rough-order-of-magnitude (ROM) cost estimate by up to 40 per cent, from an un-adjusted indicative estimate by up to 25 per cent, and from an un-adjusted substantive estimate by up to 15 per cent. Should the volatility of the projected expenditures for a specific capital asset acquisition result in a contingency that is above the relevant reference point (i.e., above 25 per cent contingency for an indicative cost estimate), it is important to be able to explain the reasons for the volatility and identify the related financial impacts. When a Treasury Board submission is required, such explanatory information should be included in the Costing Due Diligence and Validation section of the submission.

6. Preparation of Cost Estimates

6.1 General Considerations

The purpose and context in which cost information will be used determines what cost information should be provided; so the type of cost estimate information that is needed will vary.

In the acquisition of a capital asset, the initial capital outlay or capital cost is significant, but so are the costs associated with the use and ownership of the capital asset. In fact, these costs are often greater than the initial outlay, and they can vary significantly between options.

Cost estimates should be routinely reviewed and updated as new information becomes available. During the process of acquiring a capital asset, cost information will progressively improve through inclusion of more reliable information and greater certainty around aspects of delivering the capital asset.

6.2 Developing a Cost Estimate

Developing cost estimate information involves time and effort. When determining which approach to take in developing such information, it is important to weigh the benefits to be gained from the information against the cost to produce it. A cost estimate can be as simple as creating a table of expected annual costs, or as complex as developing a computer model that allows for the creation of multiple scenarios based on multiple assumptions about future cost drivers.

As a first step, it is important to establish the purpose that the cost estimate information is intended to serve (e.g., determining which option to recommend based on a comparison of the life-cycle costs of each option, requesting project authority or expenditure authority, or creating an estimate for investment planning) and to create a cost model with sufficient depth of information to capture the complexity of the situation.

Difficulty arises when estimating future costs, which are usually subject to a level of uncertainty on account of the following:

- Nature of the capital asset;

- Actual versus planned pattern of use of the capital asset over time;

- Type and level of operating costs;

- Need for, and cost of, maintenance activities; and

- Impact of inflation on costs.

To estimate the costs of a capital asset, it is necessary to identify the key activities involved in acquiring and owning the asset. These activities must have the following three characteristics:

- The activity must be clearly defined and result in a cost being incurred;

- The time when the cost of the activity will be incurred must be known; and

- The relationship between the level of activity (e.g., the average number of days a ship will be at sea each year) and the amount of resources that will be consumed must be known.

The choice of cost elements is a reflection of the nature and complexity of the specific capital asset and the factors that determine its cost.

Developing a cost estimate involves:

- Establish the ground rules and assumptions of the cost estimate;

- Develop the cost estimate model;

- Gather data, and populate and document the cost model; and

- Review, analyze and update the cost estimate.

Each of these aspects is described in the following subsections.

6.2.1 Establish the ground rules and assumptions of the cost estimate

Cost estimates are typically based on limited information. Because of the many unknowns, cost analysts need a series of statements that define the conditions on which the cost estimate will be based. These conditions usually take the form of ground rules and assumptions that establish the estimate's scope and baseline conditions.

a. Ground rules

Ground rules are constraints that the cost estimator has been directed to use by the decision maker when developing the estimate. The technical specification for the required capital asset is an example of a ground rule. As each ground rule is developed and approved, a record of its approval along with the supporting rationale should be saved with the project documentation.

b. Assumptions

Framing assumptions – are assumptions that form critical parameters of a project and significantly impact program outcomes such as cost, schedule, and performance. The consequences of an incorrect framing assumption are fundamental and cannot be easily mitigated.

A project's framing assumptions are generally beyond the project team's control. They should be defined, documented and approved to ensure that decision makers clearly understand the impact of these assumptions on the cost estimate. Following are some examples of framing assumptions:

- Prototype design is close to production ready;

- Competitive prototyping will save 5 per cent of the acquisition cost;

- Incremental/open architecture will reduce risk and allow for more efficient upgrades; and

- The project will require minimal modifications to be useable.

General assumptions – are what a cost estimator uses to address any gaps between the ground rules and the information needed to develop the cost estimate. All assumptions, whether established at the outset of the costing exercise or throughout, need to be well documented. Documentation should explain the assumption's rationale and data sources.

Following are examples of general assumptions:

- The cost estimate's base year, the length of time the asset is expected to be in service, and the level of use while the asset is in service;

- Asset requirements by life-cycle phase (e.g., a call centre with the capability of responding to 9,000 phone calls a day, in French or English, with a maximum response time of three minutes);

- Acquisition strategy and schedule, by phase if applicable;

- Schedule or budget constraints;

- Equipment or facilities to be furnished by the government;

- Technology refresh cycles, technology assumptions, and new technology to be developed;

- Effects of new ways of doing business;

- The sustainment strategy as currently understood or assumed (e.g., replacing a ship's engine after a predetermined number of years of service to maintain operational performance); and

- Attrition assumptions (e.g., replacing vehicles from the fleet that are damaged beyond repair when the number exceeds five so that program objectives can continue to be met).

6.2.2 Develop the cost estimate model

The cost estimate model is developed based on the established ground rules and assumptions, as well as on the following key elements.

a. Cost boundary

A cost boundary defines what cost elements are to be included in the cost estimate, as well as the level of detail required. Level of detail is also dependent on external factors such as the maximum time available to develop the cost estimate, the financial means available, the availability of qualified personnel to develop the cost estimate, the availability of experts to provide information, and the availability of data.

The following boundaries need to be considered:

- Definition of the capital asset being acquired and, in particular, the elements to be costed. Stakeholders should be consulted and a consensus reached with them regarding the cost elements that are outside the scope of the cost estimate;

- Timescale to establish which phases are to be included in the cost estimate. For example, will the capital asset be acquired through a phased procurement? Will there be a phased implementation? Are there incremental build standards? What is the forecasted in-service date and the likely operating life of the proposed capital asset or system? Timescale is usually aligned with the timeline for the overarching project.

- Scope of the estimate, which can range from the initial cost of buying a capital asset such as a single piece of equipment (the capital cost) to the total cost to the government to develop, procure, operate, support, and dispose of this capital asset (the whole-of-life cost).

Boundaries and their supporting rationale should be recorded in project documentation.

b. Cost structure

A cost structure is a logical and complete breakdown of the capital asset's requirements such that if the structure is completely populated with accurate data, the total cost estimate will be complete.

A cost structure is developed by deconstructing the life-cycle of the asset into manageable elements (i.e., subsystems, components, services and work packages).

| Level 1 | Level 2 |

|---|---|

| Development of requirements | Research and development |

| Solicitation | |

| Project management | |

| Other items | |

| Acquisition | Primary system development or acquisition |

| Support system development or acquisition | |

| Production system development or acquisition | |

| Contractor services | |

| Other services | |

| Project management | |

| Sustainment and Operations | Operating resources |

| Support resources | |

| Contractor support services | |

| Sustainment office services | |

| Disposal | Disposal planning |

| Disposal activities |

The cost structure for an acquisition project is usually developed in conjunction with the project's work-breakdown structure (WBS) so that the schedule of costs aligns with the schedule of activities required to complete the project. The WBS and associated cost structure should allow for reasonable assumptions that are needed to develop an appropriate schedule for completing the project.

Following are two important elements to consider in developing the project schedule:

- Burn rate – The planned rate at which the project will spend its budget, which can be used to identify when work may need to be adjusted or when efficiencies are not being realized.

- Slack – The amount of time within a project that tasks can be delayed before the project finish date or other tasks are affected. Identification of slack can help plan for the efficient use of resources (e.g., where resources can be moved during certain phases of the project to accommodate the use of slack without impacting the end date).

c. Cost method

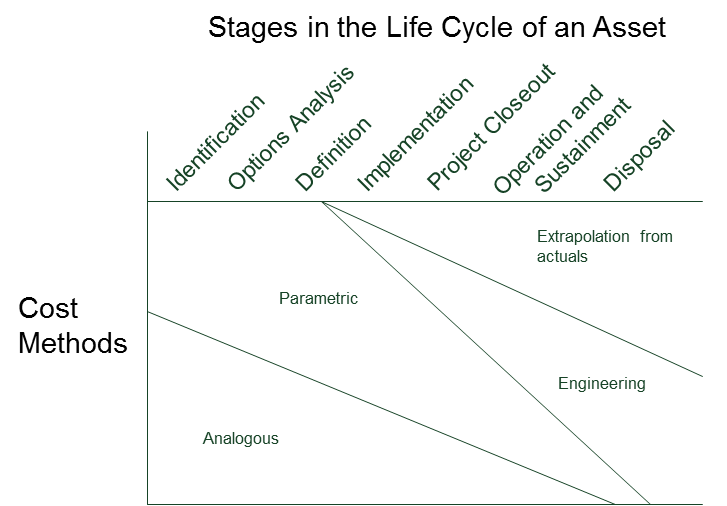

As a leading practice, the costing team should identify the method or methods they propose to apply in estimating the costs for each cost element in the cost structure. The four most common methods are described below along with the circumstances under which each approach might be used.

Analogous cost method

Analogous cost estimating is a technique used to estimate a cost based on historical data for an analogous system or subsystem. In this technique, an existing system, similar in design and operation to the proposed system, is used as a basis for analogy. The cost of the proposed system is then estimated by adjusting the historical cost of the existing system to account for the differences. Such adjustments can be made through the use of factors or scaling parameters that represent differences in size, performance, technology, or complexity.

Analogy relies a great deal on expert opinion to modify the existing system data to approximate the new system. If possible, the adjustments should be quantitative rather than qualitative, avoiding subjective judgments as much as possible. An analogy is often used as a cross-check for other methods.

Parametric cost method

Parametric cost estimating is a technique that uses regression or other statistical methods to develop cost estimating relationships (CERs). A CER is an equation for estimating a given cost element using an established relationship with one or more independent variables. The relationship may be mathematically simple, or it may involve a complex equation (often derived from regression analysis of historical systems or subsystems). CERs should be current, applicable to the system or subsystem in question, and appropriate for the range of data being considered.

Using a parametric method requires access to historical data, which may be difficult to obtain. If the data are available, they can be used to determine the cost drivers and provide statistical results. The data can also be adjusted to meet the requirements of the new program. Unlike analogy, parametric estimating relies on data from many programs and covers a broader range. Confidence in a parametric estimate's results depends on how valid the relationships are between the cost and the physical attributes or performance characteristics. Using this method, the cost estimator must always present the related statistics, assumptions, and sources for the data.

Parametric techniques can be used in a wide variety of situations, ranging from early planning estimates to detailed contract negotiations. It is essential to have an adequate number of relevant data points, and care must be taken to normalize the data set so that it is consistent and complete.

Engineering cost method

Engineering cost estimating is a technique that involves direct estimation of a particular cost element by breaking down the system being costed into lower-level components (such as parts or assemblies), each of which is costed separately for direct labour, direct materials, and other costs. The method builds the overall cost estimate by summing the detailed lower-level estimates—which is why it is sometimes characterized as a "bottom-up" approach.

Engineering estimates for direct labour hours may be based on analyses of engineering drawings and contractor or industry-wide standards. Engineering estimates for direct material may be based on the requirements for raw materials and pre-manufactured parts. The remaining elements of cost (such as quality control or overhead charges) may be factored from the direct labour and material costs. The various discrete cost estimates are aggregated by simple algebraic equations.

The use of the engineering cost method requires extensive knowledge of a system's characteristics and the characteristics of its components, as well as the availability of detailed data.

Extrapolation from actuals

Actual cost estimating is a technique where actual cost experience or trends (from prototypes, engineering development models, or early production items) are used to project estimates of future costs for the same system. These projections may be made at various levels of detail, depending on the availability of data.

To summarize, the approach taken and the cost estimation techniques that are used should take into consideration the following:

- Feasibility of obtaining data;

- Newness of the technology; and

- Stage of the life-cycle analysis.

As illustrated in Figure 1, the costing team uses the analogous and parametric cost methods in the early stages of the acquisition process when information is limited. These methods can be used early on because they rely on the historical cost of a similar asset. The analogous cost method determines the degree of similarity between the existing asset and the new asset. The parametric cost method uses statistical techniques to develop cost estimating relationships. An example would be determining the size of the engine required for a ship of a given weight and using this information to estimate the cost of the engine.

Later in the process, once the asset requirements are defined and more information becomes available, the costing team uses the engineering cost method to estimate the cost of individual components, which can be summarized to produce an overall cost estimate. Toward the end of the process when some costs have been incurred, the team uses the extrapolation from actuals method, which is dependent on having sufficient expenditure data. This method can be used to extrapolate or project a future cost, such as estimating the cost of fuel in the second year of operating a ship, based on fuel consumed in the first year of operations.

Comparing the results of these methods can provide insight into the relative accuracy of the final estimate results.

As the development of an asset progresses, there should be increased confidence in the estimate, due to increased confidence in the underlying data. For this reason, the maturation of a cost model for the project can also be explained by the maturation of the cost methods used, with analogous data at the beginning and engineering data at the end, supported by actual contract costs.

6.2.3 Gather data, populate the cost model and develop the estimate

This component involves collecting and normalizing data, populating the cost estimate model, and developing the baseline estimate.

a. Collecting and normalizing data

Data are gathered from a variety of sources and often come in many different forms. Therefore, they need to be adjusted before being used for comparative analysis or as a basis for projecting future costs. Cost data are adjusted in a process called normalization, which involves stripping out the effects of certain external influences. The objective of data normalization is to improve data consistency so that comparisons and projections are more valid and other data can be used to increase the number of data points. Data are normalized in several ways.

Cost units

The cost estimator needs to understand what the cost represents; therefore, costs may be adjusted for currency conversions or to ensure that they represent only direct labour costs. Further, cost data have to be converted to equivalent units before being used in a data set. That is, costs expressed in thousands, millions, or billions of dollars must be converted to one format (e.g., all costs expressed in millions of dollars).

Sizing units

Sizing units normalize data to common units, such as cost per foot, cost per pound, and cost per software line of code. When normalizing data for unit size, it is essential to define exactly what the unit represents. What constitutes a software line of code? Does it include carriage returns or comments? The main point is to clearly define what the sizing metric is so that the data can be converted to a common standard before being used in the estimate.

Key groupings

Key groupings normalize data by similar purposes, characteristics, or operating environments and by cost type or work content. Programs with similar purposes have similar characteristics, as do programs with similar operating environments. Programs with different purposes or operating environments have different characteristics. For example, transfer payment programs for industry exhibit different characteristics from transfer payment programs for the cultural sector. Costs should also be grouped by type. For example, costs should be broken out by recurring and non-recurring costs, or by fixed and variable costs.

Technology maturity

Technology maturity normalizes data for where a program is in its life cycle; it also considers learning and the effects of the rate of technological change. The first unit of something is expected to cost more than the thousandth unit, just as a system procured at one unit per year is expected to cost more per unit than the same system procured at one thousand units per year.

Technology normalization is the process of adjusting cost data for productivity improvements resulting from technological advancements that occur over time. In effect, technology normalization recognizes that technology continually improves; therefore, a cost estimator must make a subjective attempt to measure the effect of this improvement on historical program costs. For instance, an item developed 10 years ago may have been considered state of the art, and the costs would have been higher than normal. Today, that item may be available off the shelf at considerably less cost.

Technology normalization is the ability to forecast technology by predicting the timing and degree of change of technological parameters associated with the design, production, and use of devices. However, being able to adjust the cost data to reflect where the item is in its life cycle is very subjective because it requires identifying the relative state of technology at different points in time.

Homogeneous groups

Using homogeneous groups normalizes for differences between historical and new program elements in order to achieve content consistency. To do this type of normalization, a cost estimator needs to gather cost data that can be formatted to match the desired cost element definition. This may require adding and deleting certain items to get an apples-to-apples comparison. A properly defined cost structure is necessary to avoid inconsistencies.

b. Populating the cost estimate model

The populated cost estimate model and the related procedure should be:

- Accurate – The populated model should capture costs and CERs that are unbiased and suitable to the purpose. It should properly reflect the risks, the risk mitigation strategies, and any uncertainty in the data.

- Comprehensive – The populated model should align with a cost structure that fully captures the capability of the capital asset. All costs driven by the ground rules and assumptions should be properly documented.

- Replicable and auditable – Cost elements should be fully traceable to the system specifications. The cost estimate should be thoroughly documented, including source data and significance. From the information provided, a reviewer should be able to repeat all calculations and achieve the same results.

- Traceable – Data should be traceable back to source documentation. The cost structure should be aligned to the organizational structure and the way work is conducted.

- Flexible – Estimation techniques should be allowed to vary as the understanding of the asset's capability progresses through the various phases of the project.

- Credible – The model should follow the principles and leading practices of costing to support the delivery of a credible result. This can be further enhanced through the use of independent reviews as part of a quality control process.

- Timely – Results must be available when required. The potential impact of having insufficient time to conduct analysis must be quickly and clearly communicated to decision makers, along with the potential limitations this could bring to the cost analysis.

- Reviewed periodically – Depending on need and affordability, all assumptions, processes, and calculations used to produce the cost information, along with the data sources, could be reviewed at least every two years, or as part of an annual update, to ensure continuing validity.

c. Developing the baseline estimate

The baseline estimate is the estimated cost of the asset without any provision for risk. It is developed as follows:

- The cost of each element is estimated according to the most appropriate cost estimation technique;

- The cost is estimated according to scope of the project and the asset requirements, not according to the budget;

- Cost estimates should be time-phased because program-related costs span many years. Time-phasing recognizes resource requirements that occur over the life of the asset and can vary from year to year;

- It is important that the cost estimate be an unbiased representation of the expected costs of the required asset, aligned with the agreed-upon assumptions and other endorsed documentation; and

- The baseline estimate should be validated using available historical data and independent costing methods. Key information should be documented throughout the modelling process, including the steps taken by the cost estimator to internally validate the model.

6.2.4 Review, analyze and update the cost estimate

Once the cost estimate is completed, it should be reviewed to determine whether there is any uncertainty or risk associated with the costing, or any variations that should be taken into consideration. Some data may require updating based on new assumptions that emerge.

a. Conduct sensitivity analysis

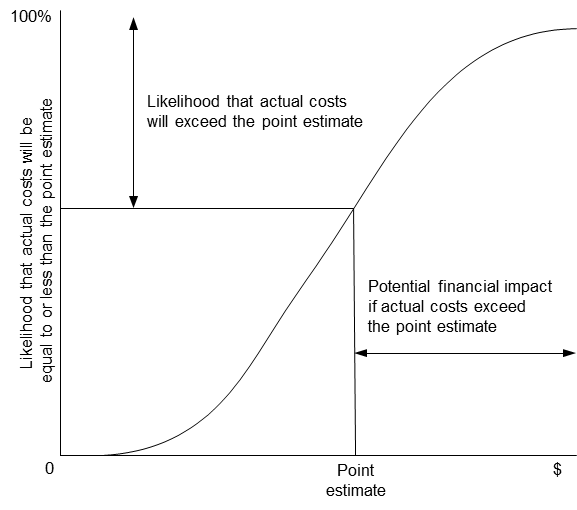

Sensitivity analysis is a useful tool that helps manage uncertainty and project cost risks. It provides a range of costs around a single point estimate that allows for better informed decisions about which risk mitigation strategies would have the most impact.

The following variables could be considered when doing a sensitivity analysis:

- Assumptions;

- Fluctuations in foreign exchange;

- Underpinning indices (i.e., inflation, fuel);

- Effort required to complete key activities; and

- Project schedule.

b. Conduct risk and uncertainty analysis

Decision makers need to be informed of the risks and uncertainties related to the cost estimates that are submitted for consideration. Quantitative risk and uncertainty analysis provides a way to assess variability in a point estimate. Clear and concise statements need to be made about the risks and uncertainties, the probability of an occurrence (i.e., an occurrence of an identified risk such as an increase in the price of steel), and the potential impact of an occurrence on the cost estimate.

Quantitative risk and uncertainty analysis can model such effects as technical changes, slipping schedules, changing requirements, and proposed solutions not meeting user needs. This type of analysis provides a range of potential costs around a point estimate, which is useful to decision makers in conveying the level of confidence in the cost estimate.

The appropriate level of confidence for a risk-adjusted estimate can be defined as follows:

- Cost estimates should provide at least a 50-per cent confidence level. For budgeting purposes, a higher confidence level (from 70 per cent to 80 per cent, or the mean) is now common practice; and

- An appropriate level of contingency should be added to the point estimate in order to derive a risk-adjusted estimate that reflects the risks and the desired level of confidence.

Uncertainty analysis is undertaken so that the probability associated with achieving the cost estimate can be determined. Uncertainty results from three possible sources: limited data, human unpredictability, and errors of observation or measurement.

One form of analysis that may be considered when developing a cost estimate is cumulative probability distribution, more commonly known as an S curve, because it can show the uncertainty of various cost estimates. The S curve can be derived using statistical methodologies such as a Monte Carlo simulation. In the simulation, the cost element probabilities are combined to give an overall project probability distribution. Monte Carlo simulations can be implemented quickly once all the data have been collected.

The S curve is used to analyze how an increase or decrease in the estimated cost affects the probability of being on budget. If the cost estimate is increased, the probability of staying within budget goes up, and the potential financial impact of the estimate being wrong goes down.

a. Document results

Ongoing documentation is a key requirement for cost models. It is a leading practice to document and retain all assumptions, processes, calculations, and decisions that are used in producing cost information.

If data are available, the following are the minimum steps recommended to document results:

- Create an executive summary that provides sufficient explanation for a non-expert to understand the costs and the underlying assumptions;

- Document the model such that another cost analyst unfamiliar with the asset requirement could recreate it quickly and produce the same result;

- Allow documentation to be routinely examined by other members of the costing organization to help ensure that the information remains appropriately updated; and

- Document the degree of uncertainty inherent in the estimate. Risk, sensitivity, and uncertainty should be documented using techniques such as S curves and Monte Carlo simulations, as appropriate.

The documentation should also include information that will allow the cost estimate to be effectively communicated to outside stakeholders, such as relevant contextual information.

d. Provide cost estimate assurance

When required, an independent review of the cost estimate may be conducted or an independent cost estimate (ICE) may be developed. The primary purpose of this step is to challenge an existing cost estimate to ensure that it is robust and reliable, taking into account the phase of the project and the current knowledge.

Best practices in developing a quality ICE include the following:

- The organization or group that develops the ICE is independent from the organization that developed the original cost estimate. The two organizations can be in the same department, but must be independent of each other;

- The independent cost-estimating organization needs to have skilled, experienced cost estimators with sufficient organizational support;

- The same access to data is made available to the independent cost estimator;

- The independent cost estimator is to follow the approved cost estimate approach;

- The independent cost estimator is to produce a stand-alone cost estimate report that is suitable for the intended audience (usually senior management);

- Once the ICE is complete, the project costing team and the independent costing team document any differences and factual errors (if any);

- A final cost estimate correlation report is to be produced and approved by both the independent cost estimator and the project manager, outlining the differences and the reasons for the differences between the estimates;

- The project cost estimate model should then be updated, if required, to accommodate any insights provided by the independent review; and

- The revised cost estimate should be provided to the decision maker.

7. Presentation of Cost Estimates

Once the cost estimate has been created, it must be used within the context of providing cost estimate information and is usually presented in a report for the purposes of a decision (e.g., investment plan, Memorandum to Cabinet, Treasury Board submission, Chief Financial Officer attestation).

The following general information points should be considered:

- A cost estimate report should be developed for the decision maker and should include the outcomes of the cost estimate analysis and any implications (including affordability) for the asset.

- The report should be focused on the decision to be made and contain factual information that is relevant to that decision.

- Cost estimate data presented to decision makers for one decision should be easily traceable to data presented to support earlier or other related decisions.

- Where information has changed from earlier reports, the changes should be explained and supported by a robust audit trail.

a. Report structure

Leading practice is to use a standard cost estimate report structure that brings out the key issues related to the costs presented in a concise, factual, and easy-to-understand manner. The report should not assume that the reader has a detailed understanding of cost estimating principles.

The report should include details that are pertinent to the decision at hand, such as the confidence level in the estimated cost and summaries of analysis such as sensitivity, risk, uncertainty and affordability. Careful attention should be paid to the expression of uncertainty.

b. Reporting level of confidence

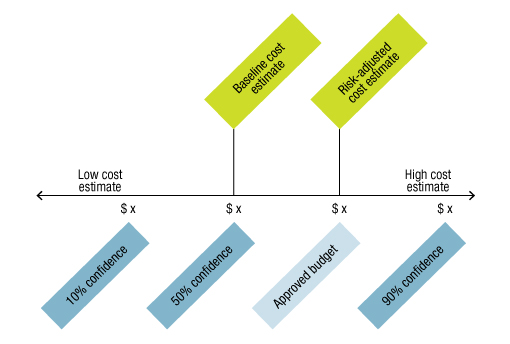

The key focus of interest for senior decision makers is the estimated cost and the level of confidence in the estimate. If data are available, it is recommended that the estimate be presented against a range of confidence levels in order to provide reference points for the decision maker, as in Figure 3.

Figure 3: Presentation of Cost Estimate Uncertainty Using a Range of Cost Estimates

Figure 3 shows how to present a range of cost estimates as an alternative to presenting a point estimate. The range includes low, medium and high cost estimates. For the low cost estimate, the presentation indicates a low level of confidence that the project will be on budget. This contrasts with the high cost estimate, which has a high level of confidence. The baseline cost estimate appears in the middle of the range because it has not been adjusted for risk. The risk-adjusted cost estimate is normally higher than the baseline cost estimate and would be the proposed budget. When presenting a range of cost estimates identify key risks that could lead to higher costs; strategies to manage risks and reduce or contain costs; and key assumptions underpinning the estimate that have not been included in the risk and uncertainty analysis.

Leading practice indicates that if data are available, a three-point cost estimate should be prepared to at least a 50-per cent confidence level.

Management selects the appropriate confidence levels and the reporting period for the various project phases, according to its judgment, taking into consideration other factors such as the purpose for which the cost estimate is to be used, the quality of data available, and other relevant factors.

c. Report period

The time frame for the cost analysis should serve the decision maker and should be determined when establishing the overall purpose of the cost estimate. Typically, the life-cycle cost time frame is from development to disposal. However, shorter periods are appropriate when the decision maker does not require full life-cycle information (e.g., purchase only).

d. Cost estimate report template

The following template for the cost estimate report is recommended:

- Purpose (decision this information will support)

- Context

- Previous decisions (Cabinet and Treasury Board decisions)

- Status (relative to the last decision)

- Cost Estimate Analysis Overview (information to be disclosed)

- Requirements (endorsed statement of asset requirements )

- Boundaries (based on the defined purpose)

- Assumptions (defined and approved)

- Ground rules

- Cost model

- Cost-breakdown structure (within designated boundaries)

- Costing methodology (a description of the methodology, e.g., are estimation techniques appropriate, and are the estimates validated against available historical data?)

- Cost elements (elements with a significant impact are identified)

- Contingency (appropriate amount to mitigate risk and uncertainty)

- Uncertainty (inherent in the estimate)

In cases where the cost estimate is included in a Treasury Board submission that requests project approval or expenditure authority, this information may be incorporated into the project brief.

8. Using Cost Estimates for Decision Making

Cost estimation enhances the ability to make decisions about acquiring a capital asset using information on the cost of the capital asset over its useful life. Decision makers can estimate the total costs to the government in purchasing and using the capital asset and can understand the drivers for differences between options and between alternative ways to acquire the capital asset.

Information generated by the cost estimate of a capital asset supports decision making at various stages of its acquisition:

- Planning and analyzing alternative solutions;

- Selecting preferred option;

- Securing funding; and

- Reviewing predicted outcomes against actual outcomes.

In addition, the cost information can be used in evaluating actual costs against estimated costs to confirm the reliability of the cost estimate and to review the risks associated with the various assumptions. Cost information provides a useful record of the rationale behind the decision to acquire a capital asset, and it can be used to improve similar cost estimation models in the future.

8.1 Deciding whether to undertake an LCCA

A life-cycle cost analysis (LCCA) is required in capital asset acquisitions when the design or procurement selection is between two or more options. The TBS or other central agencies may also require an LCCA to be undertaken in situations where the following conditions exist:

- There is a significant technical risk;

- The capital asset is highly complex; and

- The capital asset is of strategic significance to Canada.

An LCCA provides useful information to support decision making and project monitoring; however, undertaking an LCCA involves creating a cost estimate and information on options that is more complex, time consuming and costly to develop than standard cost estimates. Because of the additional cost and complexity, the benefits of an LCCA should be weighed against its cost before a decision is made to undertake such an analysis, in situations other than those described above.

8.2 Additional cost estimation requirements for conducting an LCCA

When conducting an LCCA, the cost estimate for acquiring the capital asset will require additional actions, including the following.

a. Discounted cost estimate

Discounted cash flows determine the present value of future cash flows. Money received in the future is not worth as much as money on hand today due to the erosion in value caused by inflation. Discounted cash flows also facilitate an evaluation of the costs of competing proposals and provide decision makers with a clear assessment of the financial implications of their decisions.

A discounted cost estimate is developed to support project approval decisions involving the acquisition of capital assets including equipment, information management and information technology hardware and software, and real property.

When developing a discounted cost estimate, use the appropriate rate from the Department of Finance Canada website Consolidated Revenue Fund Monthly Lending Rates for Periods of One Year and Over.

b. Identification of the cost drivers

When comparing the costs of various options for acquiring a capital asset, it is important to understand the differences between the options being considered. Therefore, all cost drivers will need to be considered. Where costs differ between options, the impact of the differences should be explored and captured.

For example, let us say that in Option A, the capital asset costs $100 to purchase and in Option B, the capital asset costs $80 to purchase. Option A requires 20 per cent more staff to manage the capital asset over its useful life than Option B, but Option A's maintenance staff do not need to be as well qualified as Option B's; therefore, the average salary of Option A's staff is 40 per cent less.

When creating the cost estimate, all the differences between the options need to be identified and quantified, and presented in such a way as to allow a thorough understanding of the total cost of the options.

8.3 Limitation of an LCCA

Stakeholders often seek a higher degree of precision in cost estimates for LCCAs than can be substantiated by the information available. Care needs to be taken when estimating the degree of uncertainty or level of confidence in a cost estimate for the purpose of an LCCA—and when communicating this information.

Creating a cost estimate for an LCCA is fundamentally a forecasting activity. The estimate is imprecise due to the unforeseen impact of various future events that may be difficult to quantify at the time the estimate is developed. As more information becomes available, departments should review and update their cost estimates at project milestones and decision points. An updated cost estimate provides information that enables management to effectively monitor a capital asset over its whole life.

8.4 Decision support

When a cost estimate is used to support a Treasury Board or Cabinet decision that involves the conduct of an LCCA to support the selection between one or more options, the submission should include a cost estimate report in the financial appendices or the information may be incorporated into the project brief.

The process of developing a cost estimate is complex and involves the use and generation of a significant amount of information. The report template in section 7 identifies the information that is likely to be significant for a decision maker. However, since each case is unique, the chief financial officer should exercise judgment when determining what is relevant and what to include in the report.

When there are options, the report could analyze:

- Range of alternative solutions for the acquisition of the capital asset;

- Cost drivers behind the alternative solutions;

- Time the capital asset will be required;

- Level and frequency of use; and

- Maintenance or operating arrangements and associated costs.

This type of analysis, combined with the net present value of each option, would support a recommendation. It would also support decisions on funding arrangements.

9. References

This guideline was developed to support the following policy instruments and should be read in conjunction with them:

- Guidance for the Preparation of TB Submissions

- Accounting Standard 3.1 – Treasury Board – Capital Assets

- Accounting Standard 3.1.1 – Treasury Board – Software

- Business Case Guide

- Contracting Policy

- Guideline on Chief Financial Officer Attestation for Cabinet Submissions

- Guideline to Implementing Budget 2011 Direction on Public-Private Partnerships

- Guide to Costing

- Guide to Investment Planning – Assets and Acquired Services

- Guide to Management of Materiel

- Policy on Financial Management Governance

- Policy on Financial Resource Management, Information and Reporting

- Policy on Investment Planning – Assets and Acquired Services

- Policy on the Management of Information Technology

- Policy on the Management of Material

- Policy on the Management of Projects

- Policy on the Management of Real Property

10. Enquiries

For interpretation of this guideline, please contact your departmental financial policy group or the unit within your CFO organization that is responsible for costing.

Financial policy directors, or equivalent, may contact the Secretariat's Financial Management Sector.

For public enquiries regarding this guideline, please contact TBS Public Enquiries.

Appendix A: Definitions

- Capital assets

Tangible assets that are purchased, constructed, developed, or otherwise acquired. Such assets:

- Are held for use in the production or supply of goods, in the delivery of goods and services, or to produce program outputs;

- Have a useful life extending beyond one fiscal year, and are intended to be used on a continuing basis; and

- Are not intended for resale in the ordinary course of operations.

- Capital cost

- The capital outlay associated with acquiring a capital asset, or costs associated with building a capital asset. For more information on the capitalization of assets, refer to Accounting Standard 3.1 – Treasury Board – Capital Assets.

- Contingency

- An amount that is based on the risk and uncertainty inherent in acquiring a capital asset and that is added to a point estimate to provide a risk-adjusted cost estimate. A contingency is not used to account for changes in the project's approved scope.

- Cost

- A resource consumed to achieve a specific objective. When someone is willing to incur certain costs to acquire, consume, or use a good or service, a decision has been made—overtly or otherwise—to consume resources in return for the benefits received from the acquisition or consumption of that good.

- Framing assumptions

- Explicit or implicit assumptions that are central to defining a cost estimate and that would significantly affect program outcomes if they were to change (e.g., "the prototype design is close to production ready"). Framing assumptions are foundational; they are not subordinate, derivative or linked to other assumptions (e.g., a unique aspect of a design or procurement strategy). Since these assumptions are generally beyond the project team's control, any errors in them cannot be easily mitigated or amended. A change in a framing assumption will fundamentally impact the cost estimate of a capital asset.

- Ground rules and assumptions

Basic factors that play a critical part in developing a cost estimate, including the following:

- Specific assumptions, such as the cost estimate's base year, the length of time the asset is expected to be in service, and the level of use while the asset is in service;

- Quality or performance characteristics;

- Market supply, including the use of commercial off-the-shelf products;

- Acquisition strategy and schedule, by phase if applicable;

- Schedule or budget constraints;

- Foreign exchange rate;

- Human resource requirements (e.g., group and level impacts on salary costs);

- Inflation assumptions and discount rates;

- Equipment or facilities to be furnished by the government;

- Technology refresh cycles, technology assumptions, and new technology to be developed;

- Alignment with legacy systems; and

- Sustainment strategy (e.g., replacing a ship's engine after a predetermined number of years of service to maintain operational performance).

- Independent review

- A review of the cost estimate that is done by someone who is independent of the team that did the original costing, but not necessarily outside the department. Such a review could be considered in the lead-up to a decision point. An independent review provides additional assurance that a cost estimate is suitable for the given stage of a project and the asset's overall characteristics.

- Life-cycle cost analysis (LCCA)

- Analysis used by decision makers when a decision is required regarding a selection between options in the acquisition of a capital asset. This involves discounting the whole-of-life costs of the capital assets under consideration and identifying the cost differences between the choices, as well as the drivers for the differences.

- Quality of estimates

The quality of a cost estimate will normally improve from the initial estimation of the cost to acquire a capital asset through to the estimation of costs at the final decision point. The following three terms are used to describe the quality of estimates:

- Rough order of magnitude (ROM)

- An estimate during the preliminary stage of an initiative, based on an initial list of requirements and limited knowledge of underlying risks. The level of confidence in a ROM estimate is relatively low. As the capital asset requirements become more defined, cost estimates can be refined, and their quality increases.

- Indicative estimate

An estimate of sufficient quality and reliability to support a request for project approval. An indicative estimate is expected to:

- Reflect a reasonable preliminary definition of scope, performance objective(s), and schedule;

- Take into consideration preliminary consultations with stakeholders;

- Identify assumptions that could have a significant impact on the financial requirements, and explain the potential impacts;

- Be based on a stated data source that is reliable (such as industry standards or historical data); and

- Include a preliminary assessment of risk and potential risk-mitigation strategies.

- Substantive estimate

An estimate of sufficiently high quality and reliability to warrant approval as a cost objective for the project phase(s) under consideration. A substantive estimate is expected to:

- Reflect a fully defined scope, performance objective(s), and schedule;

- Take into consideration consultations with all key stakeholders;

- Identify assumptions that can have a significant impact on the financial requirements and explain the potential impacts;

- Be based on a stated data source that is reliable (such as industry standards or historical data);

- Reflect a comprehensive assessment of the risks, and include risk-mitigation strategies; and

- Be expressed in terms of a cost per deliverable to support the monitoring and management of costs.

- Residual value

- The estimated amount that the Government of Canada obtains from the disposal of a capital asset after deducting the estimated costs of disposal.

- Whole-of-life cost

All costs associated with the useful life of a capital asset, i.e., planning costs, acquisition costs, maintenance and operating costs, and disposal costs (less residual value). The definitions of the component costs are as follows:

- Planning costs

- Costs associated with planning to acquire or build a capital asset, including costs to design or modify the design of a capital asset to make it fit for a specific purpose.

- Acquisition costs

- Capital cost of a capital asset, including the betterment of an existing asset, plus related ancillary costs expended in the purchase or building of the capital asset (e.g., the Project Management Office costs associated with managing the project to acquire or build the capital asset).

- Maintenance and operating costs

- All costs associated with sustaining and operating a capital asset over its useful life. Maintenance and operating costs could include, for example, planned software upgrades, or the crew for a new ship and the planned fuel and maintenance over the ship's useful life. Implementation costs to put the new capital asset into service should also be considered, as well as the incremental impact on other federal organizations.

- Disposal costs

- All costs associated with the retirement and disposal of a capital asset.

© His Majesty the King in right of Canada, represented by the President of the Treasury Board, 2017,

ISBN: 978-0-660-09749-7