Guide to Internal Charging and Special Financial Authorities

More information

Directive:

Terminology:

Hierarchy

1. Date of publication

This guide was published on November 22, 2019.

2. Application, purpose and scope

This guide applies to the organizations listed in section 6 of the Policy on Financial Management.

This guide provides information on:

- internal charging between departments

- special financial authorities that allow for revenues and receipts to be spent from the Consolidated Revenue Fund

This guide supports the Directive on Charging and Special Financial Authorities (the directive) by:

- providing specific information on how to meet the directive's requirements

- recommending best practices for implementing the directive

This guide complements the directive; it does not present new mandatory requirements. Examples and tips are provided for illustrative purposes only and may not apply to all departments or situations.

While this guide does not apply to the establishment of fees as defined under the provisions of the Service Fees Act, section 5 of this guide applies to revenue generated by fees.

3. Overview

Internal charging involves the costing, charging, and recovery of expenditures incurred in the provision of goods or services between departments in the Government of Canada.

Generally, all revenues and receipts must be credited to the Consolidated Revenue Fund. The only exceptions are where departments have special financial authorities, including:

- the department has revenue spending authority (either a revolving fund or vote netted revenues), as shown in Figure 1

- the receipt is special purpose money that is subject to section 21 of the Financial Administration Act

- the receipt can be credited back to the vote under section 39 of the Financial Administration Act

- the receipt is from another department and will be used to deliver a program on behalf of that department (that is, a credit to another government department's suspense account)

Figure 1: mapping of revenues, receipts and recoverable expenditures

Figure 1 - Text version

Figure 1: mapping of revenues, receipts and recoverable expenditures

The figure shows the money received by the government, which is divided into 4 categories:

- Revenues

- Credit of receipts pursuant to section 39 of the Financial Administration Act

- Interdepartmental settlements via other government department suspense accounts

- Special purpose money pursuant to section 21 of the Financial Administration Act

For revenues, if the department has the authority to respend the revenues collected, those revenues are then credited to a revolving fund authority or a vote netted revenue authority.

For the credit of receipts pursuant to section 39 of the Financial Administration Act, a receipt may be credited to the department’s appropriation if the receipt is charged in the same fiscal year as the original disbursement.

For interdepartmental settlements via other government department suspense accounts, a department can recover expenditures from other government departments (legal consultation is recommended).

For special purpose money pursuant to section 21 of the Financial Administration Act, the special purpose money must be deposited in a specified purpose account.

Legend

OGD: other government department

Note: Revolving fund authority and vote netted revenue authority can be granted by an appropriation act pursuant to section 29.1 of the Financial Administration Act. In practice, this is the most common way vote netted revenues are obtained. Revolving fund authority and vote netted revenue authority can also be granted by a department’s enabling statute or, in the case of a revolving fund authority, by the Revolving Funds Act.

4. Types of internal charging

This section provides guidance on the 2 types of internal charging in the Government of Canada and the general requirements for their administration:

- internal charging for enterprise services (subsection 4.1)

- internal charging when collaborating (subsection 4.2)

- administrative requirements for internal charging (subsection 4.3)

4.1 Internal charging for enterprise services

Subsections 4.4 and 4.5 of the directive list the requirements for internal charging for enterprise services.

- 4.1.1Enterprise services

Enterprise services (which include common services) are services offered by departments that have the mandate to provide services to other government departments. Enterprise services may be mandatory or optional. See the Common Services Policy for more information.

- 4.1.2Enterprise service organization

An enterprise service organization (which includes common service providers) is a department or organization designated as a central supplier of specific services to departments.

- 4.1.3Authority to charge

Only enterprise service organizations may provide enterprise services to client departments and charge for them. The authority to charge for enterprise services must also be consistent with the department’s mandate and priorities (see subsection 4.5.1 of the directive). The authority to charge does not automatically authorize the spending of the resulting revenues. Departments must have specific authority from Parliament to spend the revenues collected.

See section 5 of this guide for information on special financial authorities that can be obtained to respend funds.

- 4.1.4Interdepartmental charges for enterprise services

In accordance with subsections 4.4.1, 4.4.2, 4.5.1 and 4.5.2 of the directive, departments must:

- estimate the cost of providing the enterprise service

- ensure that the amount to be charged does not exceed the approved estimate (that is, the estimated cost of providing the enterprise service)

- ensure that fees charged are reasonable (that is, while the estimated costs are the maximum that can be charged, a lower amount can sometimes be considered based on other factors)

- present the costing methodology used and the determination of rates when Treasury Board approval is required

More information is available in the Guidelines on Costing.

4.2 Internal charging when collaborating

Subsections 4.6 and 4.7 of the directive list the requirements for internal charging when collaborating with another department. These requirements apply to any department that provides internal support services as defined in section 29.2 of the Financial Administration Act.

- 4.2.1Internal charging for internal support services under section 29.2 of the Financial Administration Act

Section 29.2 of the Financial Administration Act authorizes the provision and receipt of internal support services between departments. Internal support services are administrative services that:

- support a department or a program

- do not include those delivered directly to the public

Subsection 29.2(4) of the Financial Administration Act defines the following as internal support services:

- human resources management services

- financial management services

- information management services

- information technology services

- communications services

- real property services

- materiel services

- acquisition services

- any other administrative service that is designated by order of the Governor in Council

Certain services may not be provided under the authority of section 29.2 of the Financial Administration Act. Under subsection 29.2(3) of the Financial Administration Act, a department is not authorized to provide services "if, under the authority of an act of Parliament, an order-in-council, or the direction of Treasury Board:

- those services may be provided only by another department or body, including situations where a department or body has been recognized as the sole federal provider of a service. Other departments must obtain the service from the recognized provider or from a source outside the federal government.

- departments are required to obtain mandatory services from enterprise service organizations, in accordance with a Treasury Board policy instrument or decision. Departments that are not enterprise service organizations may not provide these services.

- the department is precluded from providing internal support services."

- 4.2.2Interdepartmental charges for internal support services

In accordance with subsection 4.6.1 of the directive, interdepartmental charges are made to recover incremental costs incurred in providing internal support services to other departments.

In accordance with subsection 4.6.1.1 of the directive, charges may be waived in an agreement if the costs of providing services to a department are minimal.

- 4.2.3Authority to spend revenues

Section 29.2 of the Financial Administration Act does not provide the authority to spend revenues. Departments require legal authority to spend the revenues collected from providing internal support services in order to offset expenditures incurred when providing such services (referred to as revenue spending authority).

Where a department has, or anticipates having, revenues from internal support services, and intends to spend all or part of the revenues but does not have statutory authorityFootnote 1 to do so, the department must obtain annual parliamentary authority to be able to spend all or part of the revenues, in accordance with:

- paragraph 29.1(2)(a) of the Financial Administration Act

- the vote netted revenue requirements defined in the directive

A few departments have statutory authority granted by their enabling act to spend revenues received through the conduct of their operations.

Similarly, subsection 29.1(1) of the Financial Administration Act provides statutory authority for a departmental corporationFootnote 2 to respend revenues received through the conduct of its operations.

Departments seeking to establish a revenue-spending authority for the provision of internal support services may contact their departmental program sector analyst at the Treasury Board of Canada Secretariat for guidance.

- 4.2.4Authority related to personal information

The authority to provide internal support services to, and receive such services from, other departments implicitly gives authority to provide and receive the necessary personal information. Departments should respect the requirements of the Privacy Act and associated privacy policies and directives whenever they share personal information.

4.3 Administrative requirements for internal charging

- 4.3.1Requirement for a written agreement

A written agreement between departments is required before goods or services are provided. A written agreement should normally include the following:

- a description of the services to be provided

- clearly defined roles and responsibilities

- mechanisms for making decisions and resolving disputes

- the period of the agreement and the notice required for withdrawal or termination

- the service levels and performance expectations that have been agreed upon

- the basis for charging for the services provided, the arrangements for invoicing and account settlement, and the information that will be provided to support the charges

- the types of personal information to be collected and disclosed under the agreement and the purposes for which such information will be used (this information is only required when personal information is collected)

- 4.3.2Transparent billing

In accordance with subsections 4.5.4 and 4.7.4 of the directive, invoices to client departments must have sufficient detail to support section 34 certification under the Financial Administration Act.

The information in the invoice must support the delegated authority in verifying and documenting that the work has been performed, the goods have been supplied, or the services have been rendered in accordance with the terms of the agreement (see subsection A.2.2.1.7 of Appendix A to the Directive on Delegation of Spending and Financial Authorities). This information may include:

- a detailed description of the services provided (for example, the specific services provided and items charged along with the dates or periods of time when the services were provided)

- the total amount owing

- a detailed breakdown of the costs of the services (including volume and unit cost where appropriate) and the items charged during the period

- any other relevant information that would help the delegated authority responsible for exercising certification authority verify the information in the invoice (Financial Administration Act, section 34)

5. Special financial authorities

This section provides guidance on the following special financial authorities that allow departments to spend revenues and receipts:

- revolving funds (subsection 5.2)

- vote netted revenues (subsection 5.3)

- special purpose money (subsection 5.4)

- receipts that are respendable (subsection 5.5)

- other government department (OGD) suspense accounts (subsection 5.6)

5.1 Authority to spend revenues

The authority to charge does not automatically authorize the spending of the resulting revenues. Under subsection 4.1.2 of the directive, all revenues must be deposited into the Consolidated Revenue Fund unless a department has specific authority from Parliament to spend the revenues collected. A few departments have statutory authority granted by their enabling act to spend revenues generated through the conduct of their operations.

Under subsection 4.10.3 of the directive, departments seeking a revenue spending authority must ensure that the expenses incurred to provide goods and services are directly related to the revenue generated through the sale of these goods and services. Generally, the authority sought to spend revenues previously deposited in the Consolidated Revenue Fund will reduce the appropriations of the department by the same amount, ensuring that there is no net increase in the draw on the Consolidated Revenue Fund.

To determine which revenue spending authority is most appropriate, departments should refer to Table 1 and contact their departmental program sector analyst at the Treasury Board of Canada Secretariat for guidance.

| Point of comparison | Revolving fund | Vote netted revenue |

|---|---|---|

|

Authority to charge fees |

Authority may be obtained through one of the following:

|

Authority may be obtained through one of the following:

|

|

Authority to spend revenues |

Authority may be established under one of the following:

Departments can generally retain all revenues, but they may be directed to deposit accumulated surpluses (Treasury Board approval required) in the Consolidated Revenue Fund to reduce an excessive authority limit accumulated over past years or if there is no anticipated future use. |

Authority may be established under one of the following:

Departments can generally spend up to 125% of estimated revenues. Departments must request Treasury Board approval to spend any revenues collected above this threshold. |

|

Type of authority |

It is a continuing, non-lapsing authority that allows for payments out of the Consolidated Revenue Fund, in excess of revenues collected, up to a stipulated limit (that is, the drawdown authority). |

It is a lapsing authority that allows revenues to offset related expenditures in the same fiscal year. It must be renewed every year in an appropriation act unless the department has statutory authority. |

|

Scale of operations |

Operations must be:

|

The scale of operations is less important than for a revolving fund. Operations must be distinct from activities funded by appropriations. |

|

Type of demand for goods and services and level of activity |

The demand for services is extremely variable. The objective is to fund fluctuating demands from user groups for goods and services. The level of activity is not fixed. Operations are expected to be self-sufficient and break even over their business cycle. |

There is small to medium fluctuation in the demand for services. |

|

Self-sufficiency |

Operations are completely, or almost completely, self-sufficient. |

Operations are expected to remain within the vote netted revenue authority and be partly self-sufficient. |

|

Multi-year focus for matching revenue with related expenditures |

Revenues are generally applied against expenditures over the revolving fund’s business cycle. Because demand for services is extremely variable, expenditures do not necessarily occur in the same fiscal year as revenues. Flexibility is needed to:

|

Revenues are generally applied against related expenditures incurred in the same fiscal year unless otherwise authorized by legislation. |

|

Reporting requirements |

Accrual accounting, including capitalization of assets, is required. Accrual accounting must reconcile with modified cash accounting for reporting purposes. A cost-accounting system is required. Under subsection 4.8.2 of the directive, financial statements must be prepared annually for each revolving fund. Under subsection 4.8.3 of the directive, an annual assessment of the operational and financial performance of the revolving fund must be conducted. |

Modified cash accounting and a cost-accounting system are required. |

|

Example |

Department A manages a revolving fund and it can respend revenues collected from services provided to Canadians. Revenues do not lapse and remain available to finance ongoing operations, including potential capital acquisitions and temporary deficit situations. |

Department B has vote netted revenue authority to respend revenues generated from the provision of specific internal support services to Department C (for example, human resources management and financial management services). The revenues can only be spent to offset the costs of providing the services that were incurred in that same year. Revenues lapse after the close of the fiscal year in which they were collected. |

5.2 Revolving funds

Subsections 4.8 and 4.9 of the directive list the requirements for revolving funds. These requirements apply to any department that has established a revolving fund that has a statutory drawdown limit through an appropriation act, the Revolving Funds Act, or departmental or program legislation.

Revolving funds are funding mechanisms where revenues remain available to finance continuing operations without fiscal year limitations. In the Government of Canada, revolving funds are used to provide funding for specific purposes where there is continuous authorization by Parliament to make payments out of the Consolidated Revenue Fund. The use of revolving funds is appropriate for substantial, distinct activities that provide client-oriented services where costs can be financed from revenues over a reasonable business cycle.

The statutory drawdown authority essentially provides a line of credit for the revolving fund where aggregate expenditures are less than or equal to the sum of aggregate revenues received and the drawdown authority set in legislation. Interest is charged on the amount of drawdown used, and a repayment schedule should be included in the fund’s business plan.

Activities financed by the fund are maintained separately from the activities financed by appropriations, and costs unrelated to the business of the revolving fund should not be charged to it. The types of costs that can be charged to the fund are often set out in the legislation establishing the fund.

- 5.2.1Establishing a revolving fund

Revolving funds are established by legislation. The legislation may be specific to a department or it may be an amendment to the Revolving Funds Act. In addition, paragraph 29.1(2)(b) of the Financial Administration Act provides authority for a revolving fund to be established or amended through an appropriation act.

There are many conditions that a department should meet before requesting Treasury Board approval to establish a revolving fund (see subsection A.1 of Appendix A to this guide). The following documentation should be submitted for approval by the department:

- a charter document (the operating charter)

- a business plan covering the objectives of the financial and business lines over a period of 3 to 5 years

- a Treasury Board submission seeking approval of:

- authorities for operating the revolving fund

- the terms and conditions for managing it

- appropriate financial statements, including an opening pro forma balance sheet

See subsection A.2 of Appendix A to this guide for more information on the content of the Treasury Board submission.

Under subsection 4.9.1 of the directive, "legislative approval for any matter" involves:

- the establishment and operation of a revolving fund

- changes to the amount of the statutory drawdown for a revolving fund

- changes to the purposes or the scope of operations of a revolving fund

- changes to the net authority used (which requires a source of funds) related to accumulated surpluses or deficits

- the wind-down of operations of a revolving fund (see subsection A.4 of Appendix A to this guide)

Legislation that establishes a revolving fund does 3 things:

- It gives the minister a non-lapsing statutory authority to make expenditures out of the Consolidated Revenue Fund for a purpose specified in the legislation.

- It gives the minister a non-lapsing statutory authority to spend any revenues related to that purpose.

- It sets a limit on expenditures where the aggregate expenditures for the specified purpose never exceed the sum of aggregate revenues and the statutory drawdown authority.

- 5.2.2Reporting requirements

Under subsection 4.8.3 of the directive, departments must conduct an annual assessment of the operational and financial performance of the fund. Departments may be required to submit a multi-year business plan for each revolving fund to the Treasury Board (see subsection A.3 of Appendix A to this guide).

Under subsection 4.8.1 of the directive, departments must keep separate accounts for each revolving fund. Departments should also track their use of statutory authorities to ensure that these accounts are never exceeded.

- 5.2.3Financial statements and financial performance

Under subsection 4.8.2 of the directive, the financial statements of a revolving fund should be prepared in accordance with:

- the "Public Sector Accounting Standards" and the "Public Sector Guidelines" issued by the Chartered Professional Accountants of Canada (login required)

- the Government of Canada Accounting Handbook

Under subsection 4.8.5 of the directive, departments must inform the Treasury Board of Canada Secretariat of any significant change in their operating environment and in the fund’s financial performance (for example, in cases of accumulated deficits).

- 5.2.4Planned changes to a revolving fund

Under subsection 4.9.2 of the directive, departments must obtain Treasury Board approval for planned changes to key operating aspects of a revolving fund, including:

- the scale and materiality of the fund’s activities

- the resources or assets transferred to or from the revolving fund, or the obligations assumed or relinquished by the fund

- the elements of direct or indirect costs to be charged to the revolving fund, or the basis for allocating indirect overhead costs to the fund

- the basis of fee- or rate-setting

- 5.2.5Accumulated surplus or deficit

Under subsection 4.8.4 of the directive, a revolving fund must be self-sufficient over its business cycle. While surpluses or deficits may occur in a given year, these are expected to balance out over a business cycle. Revolving funds are funded through non-lapsing appropriations, providing the flexibility needed to:

- deal with changes in the level and timing of revenues, expenditures and net income

- manage substantial investments in inventory and capital

Surpluses beyond the revolving fund’s business cycle may indicate that clients are being overcharged, while accumulated deficits may indicate that the revolving fund is not self-sufficient or that there are other underlying issues.

The Treasury Board may direct that surpluses be deposited in the Consolidated Revenue Fund if there is no expectation of offset by future deficits or if there are no anticipated uses (for example, investment in systems). The rationale is that the Treasury Board may want to reduce an excessive authority limit that has accumulated over past years.

In cases of accumulated deficits and under subsection 4.8.5 of the directive, departments must inform the Treasury Board of Canada Secretariat of any significant change in their operating environment and in the fund’s financial performance.

5.3 Vote netted revenues

Subsections 4.10 and 4.11 of the directive list the requirements for vote netted revenue (VNR). These requirements apply to any department that has established a VNR authority either under departmental or program legislation, or more commonly, through an appropriation act.

Under subsection 4.10.2 of the directive, VNR authority must be obtained annually from Parliament (for example, through an appropriation act), as it is a lapsing authority.

Under subsection 4.10.1 of the directive, departments must provide vote wordingFootnote 3 to the Treasury Board of Canada Secretariat for inclusion in appropriation acts. Only a few departments have specific statutory authorizations to expend some or all of their revenues on an ongoing basis.

Under subsections 4.10.3 and 4.10.4 of the directive, departments must ensure that:

- revenues offset related expenditures incurred in the same fiscal year that the revenues are received

- any revenues not related to these expenditures are recorded as non-respendable revenue

VNR authority provides an alternative means of wholly or partially funding selected programs or activities that generate revenues. This authority can accommodate fluctuating demands from user groups without jeopardizing the core budget of a department. Normally, using a VNR authority is appropriate where:

- a department performs ongoing activities that generate revenues from established sources internal or external to the government

- fluctuations in the level of revenue-generating activities will lead to corresponding and proportional changes in expenditures and revenues

Under either of the aforementioned scenarios, operations should be aligned to the fluctuating volumes of service in order to ensure the long-term sustainability of the program (for example, high fixed costs for full-time equivalents may increase risk if volumes fluctuate).

VNR authority is also the mandatory mechanism to be used when a department:

- provides internal support services under section 29.2 of the Financial Administration Act and

- seeks to respend the revenues, unless the department has statutory authority to expend revenues

- 5.3.1Treasury Board approval for establishing a VNR authority

Under subsection 4.11.1 of the directive, departments must obtain Treasury Board approval before seeking VNR authority from Parliament via an appropriation act. The Treasury Board submission must identify the specific revenues, activities and programs for which VNR authority is being sought. If approved, vote wording will be included in the appropriate vote of an appropriation act.

The Treasury Board submission should normally include the following:

- how the departmental mandate allows for these revenue-generating activities

- the projected demand for the activity in terms of gross expenditures and revenues over the next 5 years

- the rationale for using revenues as a source of financing for the activity

- the estimated amount of revenue for which VNR authority is sought (the amount may be subsequently adjusted through the annual Estimates process)

- the proposed vote wording to be included in subsequent appropriation acts (this wording should be comprehensive and reflect the Treasury Board approval being sought and any previous VNR approvals obtained)

- whether the revenue-generating activities are partially appropriated

- how the rate setting and the proposed rate structure were determined

More information is available in the Guidance for the Preparation of TB Submissions.

Departments seeking to establish a VNR authority may contact their departmental program sector analyst at the Treasury Board of Canada Secretariat for guidance.

- 5.3.2Rates for pricing purposes

Rates should be set in accordance with the Treasury Board Guide to Cost Estimating, which provide guidance on cost recovery and charging. As part of the Annual Reference Level Update, the basis for setting the rates to be charged in the next fiscal year may be reviewed by the Treasury Board. Changes in rates may require Treasury Board approval, as described in subsection 5.3.5 and shown in Figure 2.

- 5.3.3Recovery of expenditures in the capital vote

Under subsection 4.10.6 of the directive, recovery of capital expenditures:

- must not be recorded against the department’s operating VNR authority

- cannot be respent

- must be recorded as non-tax, non-respendable revenues to be credited to the Consolidated Revenue Fund

- 5.3.4125% rule

At the start of each fiscal year, vote netted amounts are reset and departments provide the estimated amount of revenues to be collected. The 125% rule provides added flexibility to departments by allowing them to generally respend up to 125% of the forecast revenues resulting from volume change, as long as there is a sufficient unencumbered balance.

Under subsection 4.10.5 of the directive, if revenues exceed 125% of the estimated amount in a fiscal year, an authority must be sought and approved by the Treasury Board to offset related expenditures. Departments must consult their expenditures management sector analyst at the Treasury Board of Canada Secretariat and provide a rationale for increasing their VNR authority above 125%.

- 5.3.5Changes to VNR authority

There are several reasons why a department may need to increase or decrease its VNR authority. The mechanism that departments may use to seek approval will depend on the reason for adjusting the VNR authority. The situations below apply to internal charging situations only; Treasury Board approval is required for increases in VNR authority related to increases in external fees.

- Volume change: A department may generally spend up to 125% of the forecast revenues that result from volume change. When a department needs to adjust its VNR authority because of volume change above 125% of its estimated revenues, it must seek approval from the Expenditures Management Sector of the Treasury Board of Canada Secretariat.

- Rate change: If an increase is related to a rate change in optional or mandatory services, the department must seek approval through a Treasury Board submission.

- New activity: If an increase is related to a new activity, the department must seek approval through a Treasury Board submission.

Under paragraph 32(1)(d) of the Financial Administration Act, departments can enter into commitments after the Estimates or the Interim Estimates are tabled in Parliament. The unencumbered balance includes estimated revenues. Departments can also enter into commitments for revenues received in excess of the amount set out in the Estimates or in the supply bill to the Interim Estimates if:

- the revenues have been collected as noted under subsection 4.2.1 of the Guide to Delegating and Applying Spending and Financial Authorities

- there is a sufficient unencumbered balance

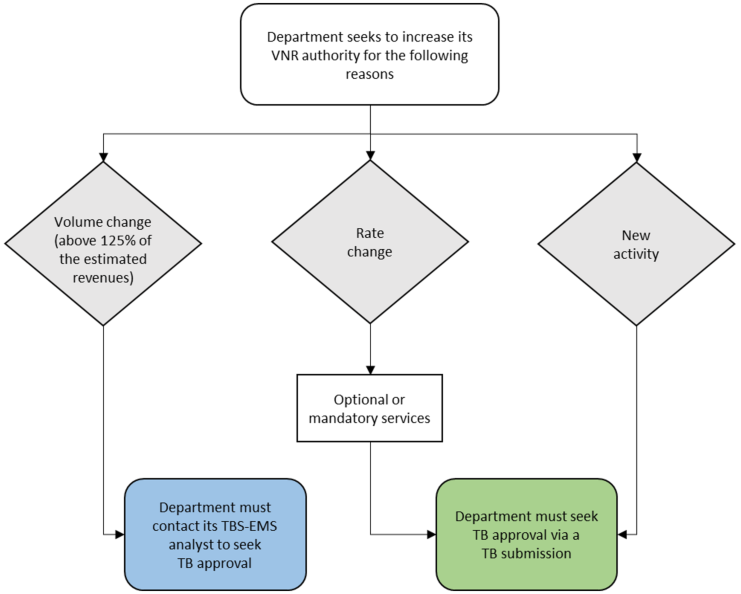

Figure 2: changes to vote netted revenue authority (internal charging only)

Figure 2 - Text version

Figure 2: changes to vote netted revenue authority (internal charging only)

The figure shows the reasons why a department might seek to increase its vote netted revenue authority. The reasons are:

- volume change (above 125% of the estimated revenues)

- a rate change

- a new activity

If the department seeks to increase its voted netted authority because of volume change, the department must contact its Treasury Board of Canada Secretariat Expenditures Management Sector analyst to seek Treasury Board approval.

If the department seeks to increase its vote netted authority because of a rate change, the department must determine whether the service is optional or mandatory and seek Treasury Board approval via a Treasury Board submission.

If the department seeks to increase its vote netted authority because of a new activity, the department must seek Treasury Board approval via a Treasury Board submission.

Legend

TB: Treasury Board

TBS-EMS: Treasury Board of Canada Secretariat-Expenditures Management Sector - 5.3.6Rights and privileges

Where the government goods and services being provided are for rights and privileges, revenues from these activities generally cannot be respent via a VNR authority or a revolving fund. Examples of rights and privileges include permits, licences or other authorizations. In addition, departments cannot respend revenues that exceed the cost of generating those associated revenues.

5.4 Special purpose money

- 5.4.1Special purpose money as described in section 21 of the Financial Administration Act

"Special purpose money" is money received or collected from an outside party (that is, external to the Government of Canada) for a special purpose and deposited in the Consolidated Revenue Fund pursuant to subsection 17(1) of the Financial Administration Act. Under subsection 4.12.1 of the directive, departments must seek approval from the Receiver General before they accept special purpose money. The money may be disbursed only for the purpose specified in the instrument under which it is received (for example, an act, a trust, a treaty or a contract). There is a direct link between monies received and monies disbursed, including any interest that may be authorized.

Special purpose money may be received through partnerships, joint projects, cost-sharing projects or similar arrangements with private sector organizations or other levels of government. Examples of special purpose money include gifts, donations, bequests and endowment funds.Footnote 4

A cost-sharing project is a common undertaking whereby the parties involved agree to participate in carrying out a project. This undertaking may involve the sharing of resources, the purchasing of goods or services, and the hiring of personnel.

Funds deposited in a specified purpose account do not lapse at year-end as the appropriation authorities governing such accounts are statutory authorities (as opposed to annual appropriations) under subsection 21(1) of the Financial Administration Act.

- 5.4.2Recording special purpose money in specified purpose accounts (SPA)

"Specified purpose accounts"Footnote 5 is a broad classification of accounts reported in the Public Accounts of Canada. These accounts are used to record transactions and expenditures payable out of the Consolidated Revenue Fund under statutory authorities established for specified purposes. Special purpose money can be recorded in a SPA only if the Receiver General has approved the creation of the SPA. Special purpose money is recorded as a liability in the Public Accounts.

Special purpose money, regardless of the source, is managed as public money. Accordingly, all regulations, policies and directives relating to the control of receipts and expenditures apply to funds received, credited and paid out for a specified purpose.

There are 2 types of SPAs:

- SPAs that record the receipt and use of special purpose money: These SPAs are usually established operationally and record obligations and expenditures for money received by the Crown for a special purpose, in accordance with:

- paragraph (d) of the definition of "public money" in section 2 of the Financial Administration Act

- subsection 21(1) of the Financial Administration Act

- SPAs that do not record special purpose money: These SPAs may involve joint ventures, partnerships, and insurance and benefit programs, and may only be established by legislation to record transactions and expenditures under specific statutory programs. These SPAs are not within the scope of the directive. More information is provided in Appendix B to this guide.

The goods and services tax (GST) / harmonized sales tax (HST) payable on expenditures charged to SPAs are generally charged to the SPAs instead of to the GST/HST refundable advance accounts (with a few exceptions). More information is provided in subsection 9.1.4 of the Financial Information Strategy Accounting Manual.

More information on the accounting treatment of SPAs is available in the Directive on Accounting Standards: GC 4100 Specified Purpose Accounts.

- SPAs that record the receipt and use of special purpose money: These SPAs are usually established operationally and record obligations and expenditures for money received by the Crown for a special purpose, in accordance with:

- 5.4.3Establishing SPAs

Under subsection 4.12.1 of the directive, departments must obtain approval from the Receiver General to establish a SPA before they accept special purpose money. A SPA to record special purpose money is opened only when all of the following conditions are met:

- There is an authority to receive or collect the funds. The authority under which the money is to be received or collected is the act, trust, treaty, undertaking or contract.

- The special purpose activity is within the department’s mandate, in accordance with subsection 4.13 of the directive.

- A liability or an obligation exists to the outside party to spend money and comply with the provisions of an agreement, a will or other unilateral transaction.

- There is a direct link between the money received or collected from the outside party and the amount to be disbursed, and the purpose for which the money will be disbursed is known at the time of receipt.

- No additional amounts, other than interest, are to be paid by or charged to the federal government as part of the arrangement for the special purpose money.

- No payment of statutory benefits to an outside party is intended or anticipated (for example, a government program is not involved).

When establishing a SPA, the primary financial control objective is to ensure that special purpose money is segregated from all other funds (that is, voted appropriations) and that payments are restricted to third parties or other government departments, in accordance with subsection 4.12.2 of the directive. To maintain control of this unique source of funds and its use, funds must be segregated and accounted for separately from all other sources and uses of spending authority.

To determine whether the establishment of a SPA meets all the requirements, arrangements must be evaluated on a case-by-case basis. To establish a SPA, the department must submit a formal request to the Receiver General, in accordance with Receiver General Directive 2009-2. The request is also shared with the Office of the Comptroller General. Once both parties are satisfied, the request form should be signed by the department’s chief financial officer and resubmitted to the Receiver General for official approval to establish the account.

- 5.4.4Monitoring special purpose money

Departments should undertake periodic reviews and audits of their use of SPAs to ensure that they are established and operated within the scope of departmental authorities and in accordance with the directive. Particular attention should be given to the proper use of authorities and to the legal aspects of contracts, agreements and any other types of arrangements whereby funds would be received for a specified purpose. Other important aspects include the managers’ understanding of the appropriate authorities and their use, and the quality of documentation (for example, legal agreements, accounting records, and training documents for managers).

Adequate internal controls, including monitoring and periodic reconciliation, should be in place. For example, a complete audit trail should be in place to permit the tracing of all transactions related to the SPA. All details about the subsidiary accounts should be kept and reconciled monthly with the total liability balance of the SPA in the Public Accounts of Canada.

- 5.4.5Considerations when using SPAs

- 5.4.5.1Separation between SPAs and appropriated funds

To maintain effective controls on spending, special purpose money must be kept separate from funds that are appropriated by Parliament. Funding sourced from the fiscal framework or approved by Parliament cannot be transferred to a SPA. The unused portion of an appropriation that would otherwise lapse must not be recorded in a SPA. Similarly, funds received and deposited in a SPA cannot be transferred to a department’s voted appropriations.

- 5.4.5.2Use of special purpose money

Special purpose money cannot be transferred to offset expenditures funded by a department’s voted appropriations for day-to-day operations (for example, salaries of indeterminate employees). However, special purpose money can be used to hire consultants or contract personnel if:

- they are specifically hired to carry out the special purpose activity

- payment for these services is charged directly to the SPA and not to the department’s voted appropriations

- 5.4.5.3Cost recovery

Special purpose money should not be used to replace or avoid the authorities required for cost-recovery activities (for example, where fees for goods, services or the use of facilities would normally be charged to an outside party). However, a department that receives special purpose money can use the services of another department that has special revenue spending authority (for example, vote netted revenue or revolving funds) to carry out or supply the special purpose activity.

- 5.4.5.4Interest

Interest on special purpose money deposited in a SPA may be authorized by specific statute or, in the absence of such authority, allowed under subsection 21(2) of the Financial Administration Act, at rates fixed by the Minister of Finance and approved by the Governor in Council.

- 5.4.5.5Administration costs

When authorized by the enabling authority (for example, an act, a trust, a treaty or a contract), administration costs may be charged to a SPA. However, where the legislation or other establishing authority does not authorize the cost of administration to be charged to the account, costs incurred by the department for the administration of the funds held in a SPA must be charged to a departmental appropriation.

- 5.4.5.6Insufficient funds in a SPA

No disbursements should be made from a SPA if there are insufficient funds at the time of payment. Accounts should not go into a negative (debit) balance unless authorized by legislation.

- 5.4.5.1Separation between SPAs and appropriated funds

- 5.4.6Closing a SPA

Under subsection 4.12.3 of the directive, once the purpose for which the funds were received has been realized:

- the balance of the account must be returned to the person who paid it, in accordance with the Repayment of Receipt Regulations

- if, in accordance with the act, trust, treaty or contract, there is no obligation to return the funds, the balance of the account must be transferred to a miscellaneous non-tax revenue account in the Consolidated Revenue Fund

5.5 Receipts that are respendable

Under subsection 4.14 of the directive, receipts must be credited to the Consolidated Revenue Fund as non-respendable revenues unless there is a special financial authority (for example, revolving funds, vote netted revenue or special purpose money).

Receipts may not be credited to a department’s appropriation if they are for revolving funds or if they are special purpose money. However, if a department has vote netted revenue authority and there is clearly stated wording in the authority, receipts can be credited to a department’s appropriation. If the department does not have vote netted revenue authority, receipts may not be credited to the department’s appropriation.

A department may credit receipts to an appropriation for the purposes listed in section 39 of the Financial Administration Act, as described in subsection A.2 of Appendix A to the directive. No additional authorities need to be requested in order to credit the appropriation under section 39.

- 5.5.1Authority to credit an appropriation pursuant to section 39 of the Financial Administration Act

Receipts may be credited to an appropriation if they are charged in the same fiscal year as the related expenditure, advance or payment, and if they apply to one of the following situations, as listed in subsection A.2.2.2 of Appendix A to the directive:

- recovery of an overpayment to a supplier

- recovery of a duplicate payment issued to a supplier

- recovery of an erroneous payment to a supplier

- recovery of delinquent account travel card charges that are paid on behalf of the cardholder by the department and recovered from the cardholder or employee

- repayment of an accountable advance

- repayment of a repayable contribution as described in the Directive on Transfer Payments

- refund from the return of goods

- refund of sales or excise taxes and custom duties

- refund of an advance payment

- refund resulting from the settlement of contractual disputes

- refund resulting from a manufacturer’s rebate, price reduction, volume discount or other price adjustment

- refund resulting from a landlord’s rebate representing cash lease incentive where a government department is a lessee

- payment received further to an indemnification

- payment received following a claim for loss of or damage to a Crown asset

- rebate resulting from contractual arrangements

- reimbursement from an organization for its agreed share of costs further to a cost-sharing arrangement (see subsection 5.5.2)

- repayment of travel expenses such as personal stopovers and side trips, for which charges were included in a departmental invoice but that are the responsibility of the employee or traveller

- repayment by employees of expenses of a personal nature such as cellular telephone charges for which payment was made by the department

- 5.5.2Cost-sharing arrangements with a third party

Departments can enter into cost-sharing arrangements with a third party for various reasons. A third party is any person or organization that is not a department as defined in section 2 of the Financial Administration Act (for example, a municipality, a provincial government, a territory, a university, a person or a private sector organization).

Cost-sharing arrangements are treated on a case-by-case basis. Departments should consult:

- their legal counsel to confirm whether there is an existing legal authority

- Financial Management Enquiries at fin-www@tbs-sct.gc.ca about the appropriate accounting treatment of these transactions

5.6 Other government department suspense accounts

This subsection outlines how financial resources are managed when one department acts on behalf of another. More information on the accounting treatment of other government department (OGD) suspense accounts is provided in subsection 9.9 of the Financial Information Strategy Accounting Manual.

- 5.6.1Administering another department’s program

Under subsection 4.15.1 of the directive, an OGD suspense account may be used only when the administering department is delivering another department’s program or incurs expenditures for another department.

The administering department may not charge payments against an OGD suspense account and recover the funds at a later date. Under subsection 4.15.3 of the directive, a written agreement must be established to ensure that all relevant accountabilities are agreed to before transferring funds to the account. Under subsection 4.15.2 of the directive, an OGD suspense account balance must be zero at the end of the fiscal year, and the administering department must return any surplus funds to the other department. OGD suspense accounts are not allowed to have a negative (debit) balance.

In accordance with subsection 4.16.1 of the directive, senior departmental managers must confirm with the Privy Council Office that the nature, materiality and duration of the planned arrangement do not warrant a change in the machinery of government. Departments may contact their departmental program sector analyst at the Treasury Board of Canada Secretariat for guidance.

6. References

Legislation

- Financial Administration Act, sections 2, 19, 21, 29.1, 29.2, 33, 34 and 39 and subsection 32(1)

- Privacy Act

- Repayment of Receipts Regulations

- Resources and Technical Surveys Act

- Revolving Funds Act

- Service Fees Act

Related policy and guidance instruments

- Common Services Policy

- Directive on Accounting Standards: GC 4100 Specified Purpose Accounts

- Directive on Charging and Special Financial Authorities

- Directive on Delegation of Spending and Financial Authorities

- Directive on Transfer Payments

- Financial Information Strategy Accounting Manual, subsections 9.1.4 and 9.9

- Government of Canada Accounting Handbook

- Guide to Cost Estimating

- Guide to Delegating and Applying Spending and Financial Authorities

- Policy on Financial Management

- Policy on Results

- "Public Sector Accounting Standards" and "Public Sector Accounting Guidelines"Footnote 6

- Treasury Board Submissions

Receiver General

7. Enquiries

Members of the public may contact Treasury Board of Canada Secretariat Public Enquiries if they have questions about this guide.

Individuals from departments should contact their departmental financial policy group if they have questions about this guide.

Individuals from the departmental financial policy group may contact Financial Management Enquiries for interpretation of this guide.

Appendix A: revolving funds

A.1 Conditions for establishing a revolving fund

The following conditions should be met before requesting Treasury Board approval to establish a revolving fund:

- The purposes of the revolving fund and the scope of its activities can be clearly distinguished from other departmental operations

- The goods or services to be provided are primarily for the benefit of identifiable individuals or groups that can be expected to pay for them

- There will be sustained demand for these goods or services

- There is a legal authority to charge for the goods or services

- Revenues and expenses of the proposed fund are closely related, and the fund will be self-sustaining over a business cycle that should normally be no more than 5 years

- A source of funds is established for the statutory drawdown

- Providing the goods and services through a revolving fund will:

- enhance business and financial discipline in the delivery of the goods or services

- support client satisfaction

- ensure reasonable costs

- The scale and materiality of the activities, resource requirements and revenues merit the additional administrative, financial management and reporting costs of a revolving fund

A.2 Content of a Treasury Board submission to establish a revolving fund

A Treasury Board submission to establish a revolving fund should contain the following information:

- a description of the purposes of the revolving fund, including the scope of the goods or services that will be financed by the fund

- a rationale for financing these activities using a revolving fund rather than using appropriations

- the reduction to reference levels, if the department previously funded the goods or services from appropriations

- the managerial and financial benefits arising from the establishment of the fund

- a business plan covering the business cycle of the fund, including pro forma financial statements

- the statutory drawdown requested, based on the business plan, with a schedule showing the projected use and repayment of the drawdown over the business cycle of the fund

- financial and operational performance indicators

- the risks that may impede the success of the fund and proposed approaches to mitigate these risks

- the governance and accountability arrangements for the revolving fund, including the roles and responsibilities of the deputy head, the chief financial officer and other senior departmental managers

- any existing capital assets to be taken over by the fund

- other resources to be transferred to, or obligations to be assumed by, the fund

- a capital investment plan for the fund

- the elements of direct and indirect costs to be charged to the revolving fund and, where appropriate, the basis for allocating indirect overhead costs to the fund

- the basis for fee or rate setting and the proposed initial fees or rates

- the proposed vote wording used to seek parliamentary authority to establish the fund

Where legislative authority to establish a revolving fund is to be obtained through an act other than an appropriation act, the statute wording should provide that amendments to the authority may be enacted through an appropriation act.

A.3 Preparing a business plan for a revolving fund

- A.3.1Introduction

A business plan is a document prepared by management to:

- summarize its operational and financial objectives for the near future

- show how the objectives will be achieved

The plan:

- serves as a blueprint to guide policy, strategy and action

- is continually modified as conditions change and new opportunities or threats emerge

An initial business plan should be submitted to the Treasury Board when authority is sought to establish a revolving fund. The plan should cover the initial business cycle of the proposed fund and should clearly indicate the following:

- the goals that will be pursued using the revolving fund

- how these goals will be met

- how progress will be measured

The business plan for a revolving fund should assure the department’s minister that management:

- has a clear sense of direction for the revolving fund

- is dealing with the appropriate issues

- is managing the fund appropriately

The plan should provide:

- the managers of the fund with objectives that are relevant to current circumstances and clear strategies for achieving those objectives

- the Treasury Board of Canada Secretariat with the operational and financial information needed to assess the ongoing viability of the fund and its impact on the fiscal framework

An updated business plan for the revolving fund may be requested by the Treasury Board of Canada Secretariat every year after the fund is established.

- A.3.2Elements of a business plan

The scale and complexity of revolving funds vary considerably. The content and structure of business plans:

- may reflect these differences

- should address, as appropriate, the following elements and any other elements of the revolving fund considered necessary by management

a. Executive summary: This section should highlight the:

- strategic issues that require attention over the planning period

- fund’s major objectives

- planned strategies to achieve the objectives

- major decisions that management expects to face during the planning period, including key capital projects, new activities and financing plans

The executive summary should bring together all proposals for the use of revolving fund authorities and any other matters that require Treasury Board approval. The rationale for these items should be evident from the business plan.

b. Mandate: This section should describe the purposes of the revolving fund and the legislative or regulatory basis for the fund’s existence, including legislative provisions and related Cabinet decisions.

c. Planning assumptions: This section should clearly identify the key assumptions underlying the business plan.

d. Operating environment: This section should:

- set out the internal and external forces that affect the fund and the way goods and services are delivered

- describe both the present and the predicted environment, based on appropriate data and assumptions

The business plan should address possible future risks, and the actions to be taken to prepare for and manage these risks.

The operating environment should be presented by business line. A business line is a set of products or services provided to a subset of clients. For each business line, the following information should be provided, as applicable:

- Clients and customers: the client group(s) for each major area of goods or services. A profile of major clients should be prepared to help identify their needs.

- Critical professional skills and the processes involved: in specific terms, the type of expertise needed to deliver goods and services.

- Partners and stakeholders: the individuals, groups and organizations that have a vested interest. The plan should describe their activities and their relationship to the revolving fund.

- Market profile: other organizations that are active in the same industry. The plan should indicate potential growth areas or shrinking markets, as well as the rationale for these projections. The plan should compare the strengths and weaknesses of similar organizations.

- Location: the potential advantages or disadvantages of the current location. For example, a location closer to clients may save time and reduce transportation costs.

- Regulatory perspective: the political pressures or changes to regulations that might create opportunities or barriers (for example, environmental legislation).

- Government policies and operations: government policies and operations that affect the fund’s operations (for example, higher operating costs than those borne by the private sector), and any audits, reviews, and governmental or departmental plans that affect the operation of the fund.

- Economic perspective: the economic factors that may affect the goods and services delivered, such as inflation levels, interest rates, exchange rates and international trade agreements.

- Other: any other aspects of the operating environment that would help readers better understand the plan.

e. Objectives, strategies and action plans by business line: This section constitutes the core of the business plan. The plans for each business line for the next 3 to 5 years should be indicated in this section. This section provides information on objectives, strategies adopted to meet these objectives, and associated action plans based on the key planning assumptions and the fund’s operating environment:

- Objectives: specific objectives for each business line over the next 3 to 5 years, linked to the strategies identified for the planning period. Objectives may include statements relating to financial viability or the ability to compete or maintain the asset base.

- Strategies: the chosen strategies and an explanation of how they will help achieve the objectives. For each business line, the anticipated impact of the strategies should be quantified to the extent possible. Strategies may include:

- marketing strategy: initiatives aimed at increasing market share or penetrating specific target markets. For each indicated market, prepare a market forecast covering the planning period.

- financial strategy: actions aimed at containing or reducing costs and establishing revenues needed to cover these costs. If the revolving fund has an accumulated deficit, the business plan should include strategies to become self-sufficient. The business plan should reflect the results of the annual assessment of operational and financial performance required by the Directive on Charting and Special Financial Authorities.

- capital asset strategy: planned major capital expenditures for each business line and their importance in relation to strategic issues and to the objectives identified for the planning period.

- human resources strategy: the human resources issues that will affect each business line over the planning period.

- Action plans: each business line should have an action plan that describes:

- what will be done to meet the objectives

- when it will be done

- who will do it

- how much each action will cost

Separate action plans should be included in the business plan for operations, marketing, management and human resources.

f. Performance measures and targets: Specific operational and financial performance measures and targets should be established for the identified objectives, by business line. These performance measures may include benchmarks and baseline targets. Baseline targets are the standards that the business unit will develop based on previous results. Benchmarks are the targets used by the best performers in the industry and may be useful in setting reasonable baseline targets.

To complete the performance measurement exercise, actual results should be compared with targets or benchmarks. The Policy on Results sets out the fundamental requirements for performance measurement and evaluation.

g. Financial components: These components may include:

- historical financial results: comparative financial statementsFootnote 7 for the last 3 fiscal years, including the:

- statement of operations and net financial position of the revolving fund

- statement of financial position

- statement of authority

- statement of net debt

- projected financial results: the types of pro forma statements required are the same as the historical statements listed above. The pro forma statements must cover the current fiscal year and the next 2 fiscal years. The business plan should fully support the assumptions inherent in the pro forma statements in terms of:

- changes in levels of sales and revenues

- proposed pricing

- capital requirements

- cost management and other aspects

- capital requirements: capital projects proposed for the planning period, funding required by year, and the proposed sources of financing.

A.4 Winding down a revolving fund

When the Treasury Board and the department responsible for a revolving fund’s operation decide to cease its operations, it is necessary to rescind the authority of the revolving fund as of a specific date.

The Treasury Board will approve the decision to close a revolving fund. The decision will identify a closing date in the fiscal year immediately following the fiscal year in which the operations ceased.

When authority to operate a revolving fund has been obtained from Parliament pursuant to the Revolving Funds Act, an appropriation act or other legislation, an authority to discontinue the revolving fund’s operations must be obtained through an appropriation act or an amendment to other legislation.

Financial statements as of the closing date of the revolving fund should be prepared, and a Treasury Board submission to discontinue the revolving fund’s operations should provide the following:

- the costs associated with the wind down

- the alternatives available and a recommendation to continue the services provided, if appropriate

- information and recommendations necessary for the orderly closing of the fund and, in particular, for the disposition of the fund’s assets

Appendix B: specified purpose accounts that do not record special purpose money

Specified purpose accounts (SPAs) that do not record special purpose money are generally established through legislation and include liability accounts or accounts that record revenues and expenditures authorized under statutory programs or for other statutorily specified purposes. Unlike SPAs that record special purpose money, there is generally no direct link between the monies received and the balance of the liability; payments charged to these accounts are based on legislated formulas.

For these SPAs, the authority to open the account is the specific legislation that either expressly creates the account or implies authority for its creation. Through legislation, the government may earmark money for a specified purpose or place restrictions on its use; however, neither action makes the money special purpose money.

Examples of SPAs that are classified as liabilities of the government are the Canada Pension Plan Account and the Superannuation Accounts. These accounts were created by statute to track and record the transactions in legislated programs.

More information on the accounting treatment of these SPAs is provided in the Directive on Accounting Standards: GC 4100 Specified Purpose Accounts.