Treasury Board of Canada Secretariat

www.tbs-sct.gc.ca

Common menu bar links

Breadcrumb Trail

ARCHIVED - Department of Finance Canada

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

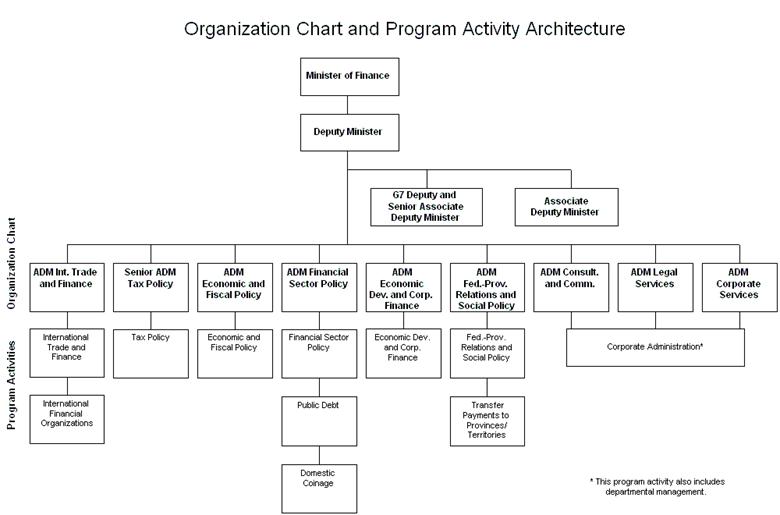

Section III: Supplementary Information

Organizational Information

Governance

The following key committees oversee the Department's governance and decision-making processes:

Executive Committee

Chaired by the deputy minister, the Executive Committee includes the senior associate deputy minister and the assistant deputy minister of each branch. The Executive Committee is responsible for the overall stewardship of the Department and exercises decision-making authority over a variety of matters, including resource allocation and priority setting.

Departmental Coordinating Committee

Chaired by a director general on a rotating basis, this committee provides recommendations to the Executive Committee on policy-related issues that fall within the scope of the Department of Finance Canada's mandate. It has representation from each branch at the director general level.

Management Advisory Committee

This committee is co-chaired by the senior associate deputy minister and the assistant deputy minister, Corporate Services Branch. The Management Advisory Committee makes and reviews recommendations to the Executive Committee. Its mandate covers the examination of department-wide plans, strategies, policies, and issues related to key administrative matters within the Department.

Audit and Evaluation Committee

The Audit and Evaluation Committee (AEC) approves the internal audit plan and associated resources based on a sound assessment of risks facing the Department. The AEC also approves evaluation plans for the Department. At the end of each internal audit and evaluation engagement, the AEC reviews and approves the final reports and associated management action plans and ensures that the results of internal audits and evaluations are incorporated into departmental priority-setting, planning, and decision-making processes. This committee is chaired by the deputy minister and meets on a quarterly or as-needed basis.

Financial Performance

This section provides a summary of the Department's financial performance, which is reported against the Department's 10 program activities. Corporate administration is distributed among the other program activities' operating costs, based on the percentage share of the operating budget in 2006-07.

The majority of the financial tables present a comparison of "Main Estimates," "Planned Spending," "Total Authorities," and "Actual." "Main Estimates" figures indicate the resources requested by the Department at the beginning of the fiscal year in order to deliver the programs for which it is responsible. "Planned Spending" is the amount included in the 2006-07 RPP and indicates amounts planned for by the Department and will include known events since the tabling of the Main Estimates. "Total Authorities" include "Main Estimates" and all other authorities approved for the 2006-07 fiscal year. "Actual" reports on total spending during the year as presented in the 2006-07 Public Accounts of Canada.

The remaining tables in this section report on statutory and other requirements. They include the table on major regulatory initiatives, a report on the response to parliamentary committees, a summary of the sustainable development strategy, and a table on travel policies.

Table 1: Comparison of Planned to Actual Spending (including FTEs)

The following table provides a comparison of the "Main Estimates," "Planned Spending," "Total Authorities," and "Actual Spending" for 2006-07, as well as historical figures for "Actual Spending" for the past two fiscal years.

| 2006-07 | ||||||

| ($ thousands) | 2004–05 Actual |

2005–06 Actual |

|

|||

| Main Estimates |

Planned Spending |

Total Authorities |

Total Actual | |||

|

Tax Policy1, 2 |

31,893 | 30,594 | 30,748 | 31,742 | 33,317 | 30,805 |

|

Economic and Fiscal Policy1 |

15,576 | 14,481 | 14,504 | 14,973 | 15,715 | 14,500 |

|

Financial Sector Policy1, 3, 4 |

20,725 | 20,993 | 20,444 | 21,105 | 173,561 | 101,443 |

|

Economic Development and Corporate Finance1 |

12,096 | 7,540 | 7,755 | 8,006 | 8,402 | 7,799 |

|

Federal-Provincial Relations and Social Policy1, 5 |

11,394 | 14,146 | 16,690 | 17,229 | 18,083 | 14,497 |

|

International Trade and Finance1 |

14,938 | 14,352 | 15,496 | 15,997 | 16,790 | 14,903 |

|

Public Debt6 |

33,869,946 | 33,535,120 | 34,395,000 | 34,395,000 | 34,108,504 | 34,108,504 |

|

Domestic Coinage7 |

63,993 | 127,811 | 83,100 | 83,100 | 135,602 | 135,602 |

|

Transfer Payments to Provinces and Territories8 |

37,746,615 | 44,160,692 | 38,330,000 | 38,631,828 | 38,441,221 | 38,441,221 |

|

International Financial Organizations9, 10 |

1,454,058 | 1,908,470 | 733,340 | 733,340 | 1,150,112 | 1,006,072 |

|

|

||||||

|

Total |

73,241,234 | 79,834,199 | 73,647,077 | 73,952,320 | 74,101,307 | 73,875,346 |

|

|

||||||

|

Less: Non-respendable revenue11 |

6,755,020 | 3,694,155 | N/A | 185,148 | N/A | 4,639,937 |

|

Plus: Cost of services received without charge12 |

17,955 | 12,385 | N/A | 13,205 | N/A | 18,774 |

|

|

||||||

|

Total Departmental Spending* |

66,504,169 | 76,152,430* | 73,647,077 | 73,780,377 | 74,101,307 | 69,254,182 |

|

|

||||||

|

Full-time Equivalents13 |

833 | 813 | N/A | 901 | N/A | 790 |

|

|

||||||

| * Due to rounding, figures may not add to totals shown. | ||||||

|

Notes: 1. Variances between "Total Authorities" and "Actual" includes $4.4 million in operating budget surpluses from Internal Services allocations primarily attributable to frozen funding of technical accounting adjustment for recovery of legal services by the Department of Justice Canada and advertising funds not required for Budget 2007. 2. Tax Policy program activity additional variances between "Total Authorities" and "Actual" are attributable to staff turnover and lower-than-expected costs in relation to the Expert Panel on Disability Savings and delayed negotiations on Aboriginal tax matters. 3. Financial Policy Sector program activity "Total Authorities" includes the following items not included in "Planned Spending": $69 million of Unused authority for payments to depositors of Canadian Commercial Bank, CCB Mortgage Investment Corporation, and Northland Bank pursuant to the Financial Institutions Depositors Compensation Act; $2 million for Payment of liabilities previously transferred to revenues; $5 million for Advances to the Financial Consumer Agency of Canada; and $76 million for Net loss on exchange in relation to re-evaluations of cross-currency swaps. 4. Financial Sector Policy program activity variance of "Total Authorities" to "Actual" is primarily attributable to the $69 million of Unused authority for payments to depositors of Canadian Commercial Bank, CCB Mortgage Investment, and Northland Bank and also includes variances for internal services surpluses an mentioned in 1. above and lower-than-expected costs for the final year of the Financial Action Task Force presidency. 5. Federal Provincial Relations and Social Policy program activity variance of "Total Authorities" to "Actual" is attributable in part to internal services surpluses as mentioned in 1. above and lower-than-expected costs to finalize the work of the Expert Panel on TTF and Equalization. 6. Public Debt program activity variance of "Planned Spending" to "Actual" is attributable to a larger-than-expected decline in the stock of interest-bearing debt. 7. Domestic coinage program activity variances from "Planned Spending" to "Total Authorities" and "Actual" are due to a higher demand for coinage from the economy and the associated higher cost to produce and distribute coinage to meet this higher demand. See Table 6 for a corresponding increase in revenues associated with the sale of domestic coinage. 8. The Transfer Payments to Provinces and Territories program activity "Planned Spending" primarily includes an additional amount not in the Main Estimates of $46,400 thousand for TFF due to data revisions and a $225,428 thousand increase in equalization transfer payments. Details on transfer payments can be found in Table 10 of this report. Variances between "Planned Spending" and "Total Authorities" and "Actual" is primarily attributable to an increase in Alternative Payments for Standing Programs of $182,016 thousand and an increase in Youth Allowances Recovery of $7,787 thousand. 9. The International Financial Organizations program activity "Total Authorities" includes adjustments for the following items not in "Planned Spending": $44,820 thousand for net loss on exchange for international payments;$63,648 thousand for funding available for use from previous years for Payments to the IMF's Proverty Reduction and Growth Facility; $318,270 thousand for issuance and payment of non-interest bearing, non-negotiable demand notes to the International Development Association in accordance with the Bretton Woods and Related Agreements Act; a reduction of $5,595 thousand for a transfer of Vote 5, Grants and Contributions, funding to Foreign Affairs and International Trade Canada; and finally statutory adjustments to reflect a reduction in actual authority required of $3,400 thousand for Payments to the IMF's Poverty Reduction and Growth Facility and $974 thousand for issuance of demand notes to the EBRD, Capital Subscriptions. 10. The International Financial Organizations program activity variance between "Total Authorities" and "Actual" is primary attributable to a lapse of $83,007 thousand in Vote 5, Grants and Contributions, and mainly due to heavily indebted poor countries not meeting the IMF program requirements as per multilateral debt relief initiatives agreed to at the Paris Club and $61,033 thousand of the funding available for use from previous years for Payments to the IMF's Poverty Reduction and Growth Facility. 11. Details of the Non-respendable revenue are listed in Table 6 of this report. 12. Details of the Cost of services received without charge are listed in Table 4 of this report. 13. FTEs has a variance of 111 FTEs from "Planned Spending" to "Actual." This variance is attributable in part to staff vacancies as a result of unexpected leaves (maternity and other), secondments, and employees leaving the Department for positions in the private sector or other departments. Additionally, there was a significant variance in the Public Debt program activity as a result of the Canada Investment and Savings transfer to the Bank of Canada. |

||||||

|

|

||||||

Table 2: Resources by Program Activity

The following table details how resources are used in the 2006–07 fiscal year showing the budgetary and non-budgetary items by program activity.

|

2006–07 ($ thousands) |

|||||||||||||

|

Budgetary |

Plus: Non-budgetary |

||||||||||||

|

Program Activity |

Operating |

Grants |

Contribu- |

Total: |

Less: |

Total: Net Budgetary |

Loans, |

Total |

|||||

|

Tax Policy |

|||||||||||||

|

Main Estimates |

30,865 |

— |

— |

30,865 |

117 |

30,748 |

— |

30,748 |

|||||

|

Planned Spending |

31,859 |

— |

— |

31,859 |

117 |

31,742 |

— |

31,742 |

|||||

|

Total Authorities |

33,434 |

— |

— |

33,434 |

117 |

33,317 |

— |

33,317 |

|||||

|

Actual Spending |

30,805 |

— |

— |

30,805 |

— |

30,805 |

— |

30,805 |

|||||

|

Economic and Fiscal Policy |

|||||||||||||

|

Main Estimates |

14,559 |

— |

— |

14,559 |

55 |

14,504 |

— |

14,504 |

|||||

|

Planned Spending |

15,028 |

— |

— |

15,028 |

55 |

14,973 |

— |

14,973 |

|||||

|

Total Authorities |

15,770 |

— |

— |

15,770 |

55 |

15,715 |

— |

15,715 |

|||||

|

Actual Spending |

14,500 |

— |

— |

14,500 |

— |

14,500 |

— |

14,500 |

|||||

|

Financial Sector Policy |

|||||||||||||

|

Main Estimates |

20,521 |

— |

— |

20,521 |

77 |

20,444 |

— |

20,444 |

|||||

|

Planned Spending |

21,182 |

— |

— |

21,182 |

77 |

21,105 |

— |

21,105 |

|||||

|

Total Authorities |

168,638 |

— |

— |

168,638 |

77 |

168,561 |

5,000 |

173,561 |

|||||

|

Actual Spending |

96,443 |

— |

— |

96,443 |

— |

96,443 |

5,000 |

101,443 |

|||||

|

Economic Development and Corporate Finance |

|||||||||||||

|

Main Estimates |

7,784 |

— |

— |

7,784 |

29 |

7,755 |

— |

7,755 |

|||||

|

Planned Spending |

8,035 |

— |

— |

8,035 |

29 |

8,006 |

— |

8,006 |

|||||

|

Total Authorities |

8,431 |

— |

— |

8,431 |

29 |

8,402 |

— |

8,402 |

|||||

| Actual Spending |

7,799 |

— |

— |

7,799 |

— |

7,799 |

— |

7,799 | |||||

|

Federal—Provincial Relations and Social Policy |

|||||||||||||

|

Main Estimates |

16,753 |

— |

— |

16,753 |

63 |

16,690 |

— |

16,690 |

|||||

|

Planned Spending |

17,292 |

— |

— |

17,292 |

63 |

17,229 |

17,229 |

||||||

|

Total Authorities |

18,146 |

— |

18,146 |

63 |

18,083 |

— |

18,083 |

||||||

|

Actual Spending |

14,497 |

— |

14,497 |

— |

14,497 |

— |

14,497 |

||||||

|

International Trade and Finance |

|||||||||||||

|

Main Estimates |

15,555 |

— |

— |

15,555 |

59 |

15,496 |

— |

15,496 |

|||||

|

Planned Spending |

16,056 |

— |

— |

16,056 |

59 |

15,997 |

— |

15,997 |

|||||

|

Total Authorities |

16,849 |

— |

16,849 |

59 |

16,790 |

— |

16,790 |

||||||

|

Actual Spending |

14,903 |

— |

14,903 |

— |

14,903 |

— |

14,903 |

||||||

|

Public Debt |

|||||||||||||

|

Main Estimates |

34,395,000 |

— |

— |

34,395,000 |

— |

34,395,000 |

— |

34,395,000 |

|||||

|

Planned Spending |

34,395,000 |

— |

— |

34,395,000 |

— |

34,395,000 |

— |

34,395,000 |

|||||

|

Total Authorities |

34,108,504 |

— |

— |

34,108,504 |

— |

34,108,504 |

— |

34,108,504 |

|||||

|

Actual Spending |

34,108,504 |

— |

— |

34,108,504 |

— |

34,108,504 |

— |

34,108,504 |

|||||

|

Domestic Coinage |

|||||||||||||

|

Main Estimates |

83,100 |

— |

— |

83,100 |

— |

83,100 |

— |

83,100 |

|||||

|

Planned Spending |

83,100 |

— |

— |

83,100 |

— |

83,100 |

— |

83,100 |

|||||

|

Total Authorities |

135,602 |

— |

— |

135,602 |

— |

135,602 |

— |

135,602 |

|||||

|

Actual Spending |

135,602 |

— |

— |

135,602 |

— |

135,602 |

— |

135,602 |

|||||

|

Transfer Payments to Provinces and Territories |

|||||||||||||

|

Main Estimates |

— |

— |

38,330,000 |

38,330,000 |

— |

38,330,000 |

— |

38,330,000 |

|||||

|

Planned Spending |

— |

— |

38,631,828 |

38,631,828 |

— |

38,631,828 |

— |

38,631,828 |

|||||

|

Total Authorities |

— |

— |

38,441,221 |

38,441,221 |

— |

38,441,221 |

— |

38,441,221 |

|||||

|

Actual Spending |

— |

— |

38,441,221 |

38,441,221 |

— |

38,441,221 |

— |

38,441,221 |

|||||

|

International Financial Organizations |

|||||||||||||

|

Main Estimates |

349,200 |

376,669 |

725,869 |

— |

725,869 |

7,471 |

733,340 | ||||||

|

Planned Spending |

349,200 |

376,669 |

725,869 |

725,869 |

7,471 | 733,340 | |||||||

|

Total Authorities |

44,820 |

332,018 |

448,505 |

825,343 |

— |

825,343 |

324,768 | 1,150,112 | |||||

|

Actual Spending |

44,820 |

249,011 |

387,472 |

681,303 |

— |

681,303 |

324,768 | 1,006,072 | |||||

|

|

|||||||||||||

* Due to rounding, figures may not add to totals shown.

Note:

1. Respendable revenue for the Department includes amounts received for the sale of documents. During 2006–07, approximately $117 thousand was received and erroneously coded to non-respendable revenue.

See Table 1 for explanations of variances.

Table 3: Voted and Statutory Items

The following table explains the way Parliament votes resources to the Department, including vote appropriations and statutory authorities for both budgetary and non-budgetary items. Parliament approves the voted funding and statutory information is provided for information purposes.

|

2006–07 ($ thousands) |

|||||

|

|

|||||

| Vote or Statutory Item |

Truncated Vote or Statutory Wording |

Main Estimates |

Planned Spending |

Total Authorities |

Total Actual |

|

1 |

Operating expenditures |

93,135 |

96,551 |

102,606 |

89,286 |

|

5 |

Grants and contributions |

404,200 |

404,200 |

398,605 |

315,598 |

|

10 |

Transfer payments to provinces and territories |

0 |

— |

0 |

— |

|

(S) |

Minister of Finance—Salary and motor car allowance |

73 |

73 |

73 |

73 |

|

(S) |

Contributions to employee benefit plans |

12,429 |

12,429 |

11,761 |

11,761 |

|

(S) |

Transfer payment to territorial governments |

2,070,000 |

2,116,400 |

2,118,264 |

2,118,264 |

|

(S) |

Payments to the International Development Association (IDA) |

318,269 |

318,269 |

318,270 |

318,270 |

|

(S) |

Payments to the IMF's Poverty Reduction and Growth Facility (PRGF) |

3,400 |

3,400 |

63,648 |

2,615 |

|

(S) |

Purchase of domestic coinage |

83,100 |

83,100 |

135,602 |

135,602 |

|

(S) |

Public debt—Interest and other costs |

34,395,000 |

34,395,000 |

34,108,504 |

34,108,504 |

|

(S) |

Statutory subsidies |

32,000 |

32,000 |

31,821 |

31,821 |

|

(S) |

Fiscal equalization |

11,282,000 |

11,537,428 |

11,535,064 |

11,535,064 |

|

(S) |

Canada Health Transfer |

20,140,000 |

20,140,000 |

20,139,876 |

20,139,876 |

|

(S) |

Canada Social Transfer |

8,500,000 |

8,500,000 |

8,500,000 |

8,500,000 |

|

(S) |

Youth allowances recovery |

(699,000) |

(699,000) |

(706,788) |

(706,788) |

|

(S) |

Alternative payments for standing programs |

(2,995,000) |

(2,995,000) |

(3,177,016) |

(3,177,016) |

|

(S) |

Payments pursuant to the Halifax Relief Commission Pension Commission Act |

— |

|

18 |

18 |

|

(S) |

Payments to depositors of Canadian Commercial Bank, CB Mortgage Invt. Corp., and Northland Bank pursuant to the Financial Institutions Act |

— |

|

68,572 |

— |

|

(S) |

Payment of liabilities previously transferred to revenue |

— |

|

2,075 |

2,075 |

|

(S) |

Spending of proceeds from the disposal of surplus Crown assets |

— |

|

28 |

— |

|

(S) |

Refunds of amounts credited to revenues in previous years |

— |

|

— |

— |

|

(S) |

Net loss on exchange |

— |

|

120,555 |

120,555 |

|

(S) |

Advances pursuant to section 13(1) of the Financial Consumer Agency Act |

— |

|

5,000 |

5,000 |

|

(L15) |

Issuance and payment of demand notes to the IDA |

0 |

— |

318,270 |

318,270 |

|

(S) |

Issuance of demand note to the EBRD—Capital subscriptions |

— |

— |

— |

— |

|

(S) |

Payments and encashments of notes to the EBRD—Capital subscriptions |

7,471 |

7,471 |

6,498 |

6,498 |

|

(S) |

Issuance of loans to the IMF's PRGF |

— |

— |

— |

— |

|

|

|||||

|

Total* |

73,647,077 |

73,952,321 |

74,101,307 |

73,875,346 |

|

|

|

|||||

* Due to rounding, figures may not add to totals shown.

Table 4: Services Received Without Charge

The following table provides the cost of services received without the change for 2006–07 fiscal year.

|

($ thousands) |

2006–07 |

|

Accommodation provided by Public Works and Government Services Canada |

9,718 |

|

Contributions covering the employer's share of employees' insurance premiums and expenditures paid by the Treasury Board of Canada Secretariat (excluding revolving funds). Employer's contribution to employees' insured benefits plans and associated expenditures paid by the Treasury Board of Canada Secretariat |

4,898 |

|

Salary and associated expenditures of legal services provided by the Department of Justice Canada |

4,158 |

|

|

|

|

Total 2006–07 Services received without charge |

18,774 |

|

|

|

Table 5: Loans, Investments, and Advances (Non-budgetary)

The following table provides details by program activity on non-budgetary items for which the Department is responsible.

|

2006–07 |

||||||

|

|

||||||

| ($ thousands) | Actual 2004–05 |

Actual 2005–06 |

Main Estimates |

Planned Spending |

Total Authorities |

Actual |

|

International Financial Organizations |

|

|

|

|

|

|

|

Issuance and payment of demand notes to the IDA |

230,134 |

318,270 |

0 |

— |

318,270 |

318,270 |

|

Issuance and payment of demand notes to the EBRD—Capital subscriptions |

6,535 |

9,157 |

— |

— |

— |

— |

|

Payment and encashment of notes issued to the EBRD—Capital subscriptions |

9,956 |

15,106 |

7,471 |

7,471 |

6,498 |

6,498 |

|

Issuance of loans to the IMF's PRGF |

19,303 |

89,956 |

— |

— |

— |

— |

|

Financial Sector Policy |

|

|

|

|

|

|

|

Advances pursuant to section 13(1) of the Financial Consumer Agency of Canada Act |

6,000 |

4,500 |

— |

— |

5,000 |

5,000 |

|

|

||||||

|

Total* |

271,928 |

436,990 |

7,471 |

7,471 |

329,768 |

329,768 |

|

|

||||||

* Due to rounding, figures may not add to totals shown.

Table 6: Sources of Respendable and Non-respendable Revenue

The following table identifies the sources of respendable and non-respendable revenue.

Respendable revenue

|

2006–07 |

||||||

|

|

||||||

|

($ thousands) |

Actual 2004–05 |

Actual |

Main |

Planned |

Total |

Actual1 |

|

Tax Policy |

|

|

|

|

|

|

|

Sale of departmental documents |

118 |

— |

117 |

117 |

117 |

— |

|

Economic and Fiscal Policy |

|

|

|

|

|

|

|

Sale of departmental documents |

56 |

— |

55 |

55 |

55 |

— |

|

Financial Sector Policy |

|

|

|

|

|

|

|

Sale of departmental documents |

55 |

— |

77 |

77 |

77 |

— |

|

Economic Development and Corporate Finance |

|

|

|

|

|

|

|

Sale of departmental documents |

31 |

— |

29 |

29 |

29 |

— |

|

Federal-Provincial Relations and Social Policy |

|

|

|

|

|

|

|

Sale of departmental documents |

41 |

— |

63 |

63 |

63 |

— |

|

International Trade and Finance |

|

|

|

|

|

|

|

Sale of departmental documents |

58 |

— |

59 |

59 |

59 |

— |

|

|

||||||

|

Total Respendable Revenue* |

359 |

— |

400 |

400 |

400 |

— |

|

|

||||||

*Due to rounding, figures may not add to totals shown.

Note:

1. Respendable revenue for the Department includes amounts received for the sale of documents. During 2006–07, approximately $117 thousand was received and erroneously coded to non-respendable revenue.

Non-respendable revenue

| 2006–07 | ||||||

|

|

||||||

|

($ thousands) |

Actual 2004–05 |

Actual 2005–06 |

Main |

Planned Revenue |

Total Authorities |

Actual |

|

Tax Policy |

|

|

|

|

|

|

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

21 |

31 |

|

|

|

6 |

|

Adjustments to prior year's payables |

237 |

296 |

|

|

|

64 |

|

Sales of goods and services—Sale of other publications |

26 |

11 |

|

|

|

35 |

|

Fees—Access to information |

2 |

1 |

|

|

|

4 |

|

Other fees and charges—Sundries |

104 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

26 |

— |

|

|

|

11 |

|

Optional Services Revolving Fund |

— |

9 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

3 |

2 |

|

|

|

6 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

Economic and Fiscal Policy |

||||||

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

10 |

15 |

|

|

|

3 |

|

Adjustments to prior year's payables |

111 |

143 |

|

|

|

30 |

|

Sales of goods and services—sale of other publications |

12 |

5 |

|

|

|

16 |

|

Fees—Access to information |

1 |

1 |

|

|

|

2 |

|

Other fees and charges—Sundries |

49 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

12 |

— |

|

|

|

5 |

|

Optional Services Revolving Fund |

— |

4 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

1 |

1 |

|

|

|

3 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

Financial Sector Policy |

||||||

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

10 |

16 |

|

|

|

4 |

|

Adjustments to prior year's payables |

110 |

158 |

|

|

|

43 |

|

Sales of goods and services—Sale of other publications |

12 |

6 |

|

|

|

23 |

|

Fees—Access to information |

1 |

1 |

|

|

|

3 |

|

Other fees and charges—Sundries |

48 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

12 |

— |

|

|

|

8 |

|

Optional Services Revolving Fund |

— |

5 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

1 |

1 |

|

|

|

4 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

Cash and accounts receivable—Cash—Chartered banks |

15,827 |

27,120 |

|

|

|

46,004 |

|

Cash and accounts receivable—Cash—Short-term deposits |

188,087 |

143,420 |

|

|

|

237,066 |

|

Cash and accounts receivable—Cash—Receiver General balance at the Bank of Canada |

34,639 |

41,598 |

|

|

|

68,160 |

|

Foreign exchange accounts—International reserves held in the Exchange Fund Account—Transfer of profit |

1,758,068 |

1,394,534 |

|

|

|

1,765,275 |

|

Foreign exchange accounts—International Monetary Fund—Subscriptions—Transfer of profit |

69,541 |

49,895 |

|

|

|

22,753 |

|

Loans, investments, and advances—Bank of Canada—Transfer of profit |

1,695,959 |

1,735,610 |

|

|

|

1,983,529 |

|

Loans, investments, and advances—Financial Consumer Agency of Canada |

97 |

112 |

|

|

|

166 |

|

Miscellaneous non-tax revenues—Transfer from the following accounts that were unclaimed or outstanding for 10 years or more: Outstanding Imprest Account—Unclaimed cheques |

32,909 |

31,057 |

|

|

|

25,929 |

|

Miscellaneous non-tax revenues—Unclaimed balances received from the Bank of Canada in respect of chartered banks |

3,675 |

3,829 |

|

|

|

3,951 |

|

Miscellaneous non-tax revenues—Mortgage interest premium |

7,171 |

8,836 |

|

|

|

10,517 |

|

Miscellaneous non-tax revenues—Sundries |

134 |

1,551 |

|

|

|

215 |

|

Economic Development and Corporate Finance |

||||||

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

5 |

8 |

|

|

|

2 |

|

Adjustments to prior year's payables |

63 |

75 |

|

|

|

16 |

|

Sales of goods and services—Sale of other publications |

7 |

3 |

|

|

|

9 |

|

Fees—Access to information |

1 |

0 |

|

|

|

1 |

|

Other fees and charges—Sundries |

27 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

7 |

— |

|

|

|

3 |

|

Optional Services Revolving Fund |

— |

2 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

1 |

0 |

|

|

|

2 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

Loans, investments, and advances—Canada Development Investment Corporation—Dividend |

164,000 |

199,000 |

|

|

|

156,000 |

|

Loans, investments, and advances—Petro-Canada—Dividend |

14,817 |

— |

|

|

|

— |

|

Miscellaneous non-tax revenues—Sale of real property to Canada Lands Company Limited |

2,268 |

2,126 |

|

|

|

2,070 |

|

Miscellaneous non-tax revenues—Sale of Crown Corporations |

2,561,657 |

— |

|

|

|

— |

|

Federal-Provincial Relations and Social Policy |

||||||

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

7 |

13 |

|

|

|

3 |

|

Adjustments to prior year's payables |

81 |

122 |

|

|

|

35 |

|

Sales of goods and services—Sale of other publications |

9 |

5 |

|

|

|

19 |

|

Fees—Access to information |

1 |

1 |

|

|

|

2 |

|

Other fees and charges—Sundries |

36 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

9 |

— |

|

|

|

6 |

|

Optional Services Revolving Fund |

— |

4 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

1 |

1 |

|

|

|

3 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

International Trade and Finance |

||||||

|

Refunds of previous years' expenditures—Refund of salaries, goods, and services |

10 |

16 |

|

|

|

3 |

|

Adjustments to prior year's payables |

115 |

152 |

|

|

|

32 |

|

Sales of goods and services—Sale of other publications |

13 |

6 |

|

|

|

17 |

|

Fees—Access to information |

1 |

1 |

|

|

|

2 |

|

Other fees and charges—Sundries |

50 |

— |

|

|

|

— |

|

Public Works and Government Services Canada—Consulting and Audit Canada Revolving Fund |

13 |

— |

|

|

|

6 |

|

Optional Services Revolving Fund |

— |

5 |

|

|

|

— |

|

Proceeds from the disposal of surplus Crown assets |

2 |

1 |

|

|

|

3 |

|

Ottawa Civil Service Recreational Association |

0 |

0 |

|

|

|

— |

|

Public Debt |

||||||

|

Miscellaneous non-tax revenues—Transfer from matured debt outstanding |

4,617 |

4,965 |

|

|

|

2,463 |

|

Domestic Coinage |

||||||

|

Domestic coinage |

110,569 |

212,942 |

|

185,148 |

|

226,843 |

|

Transfer Payments to Provinces and Territories |

||||||

|

Loans, investments, and advances—Federal-provincial fiscal arrangements |

59 |

59 |

|

|

|

59 |

|

Loans, investments, and advances—Municipal Development and Loan Board |

307 |

173 |

|

|

|

42 |

|

International Financial Organizations |

||||||

|

Loans, investments, and advances—United Kingdom—United Kingdom Financial Agreement Act, 1946—Deferred Interest |

1,767 |

1,013 |

|

|

|

335 |

|

Loans, investments, and advances—International Monetary Fund—Poverty Reduction and Growth Facility |

17,393 |

16,874 |

|

|

|

13,679 |

|

Loans, investments, and advances—Thailand Financial Assistance Loan |

— |

— |

|

|

|

— |

|

Net gain on exchange |

70,190 |

88,319 |

|

|

|

74,444 |

|

|

||||||

|

Total Non-respendable Revenue* |

6,755,020 |

3,964,155 |

|

185,148 |

|

4,639,937 |

|

|

||||||

* Due to rounding, figures may not add to totals shown.

Table 7: Resource Requirements by Branch

The following table presents the distribution of resources to the Department by branch.

|

|

2006–07 ($ thousands) |

||||||||||

|

|

|||||||||||

|

|

Program Activities |

||||||||||

|

|

|||||||||||

|

Branch |

Tax Policy |

Economic and Fiscal Policy |

Financial Sector Policy |

Economic Development and Corporate Finance |

Federal- |

International |

Public |

Domestic |

Transfer |

International |

Total |

|

Tax Policy |

|

|

|

|

|

|

|

|

|

|

|

|

Planned Spending |

31,742 |

|

|

|

|

|

|

|

|

|

31,742 |

|

Actual Spending |

30,805 |

|

|

|

|

|

|

|

|

|

30,805 |

|

Economic and Fiscal Policy |

|

|

|

|

|

|

|

|

|

|

|

|

Planned Spending |

|

14,973 |

|

|

|

|

|

|

|

|

14, 973 |

|

Actual Spending |

|

14,500 |

|

|

|

|

|

|

|

|

14,500 |

|

Financial Sector Policy1 |

|

|

|

|

|

|

|

|

|

|

|

|

Planned Spending |

|

|

21,105 |

|

|

|

34,395,000 |

83,100 |

|

|

34,499,205 |

|

Actual Spending |

|

|

101,443 |

|

|

|

34,108,504 |

135,602 |

|

|

34,345,549 |

|

Economic Development |

|

|

|

|

|

|

|

|

|||

|

Planned Spending |

|

|

|

8,006 |

|

|

|

|

|

|

8,006 |

|

Actual Spending |

|

|

|

7,799 |

|

|

|

|

|

|

7,799 |

|

Federal-Provincial |

|

|

|

|

|

|

|

|

|||

|

Planned Spending |

|

|

|

|

17,229 |

|

|

|

38,631,828 |

|

38,649,057 |

|

Actual Spending |

|

|

|

|

14,497 |

|

|

|

38,441,221 |

|

38,455,718 |

|

International Trade |

|

|

|

|

|

|

|

|

|

||

|

Planned Spending |

|

|

|

|

|

15,997 |

|

|

|

733,340 |

749,337 |

|

Actual Spending |

|

|

|

|

|

14,903 |

|

|

|

1,006,072 |

1,020,975 |

|

|

|||||||||||

* Due to rounding, figures may not add to totals shown.

Notes:

1. Financial Policy Sector Branch variance in the Financial Sector Policy program activity is $76 million for Net loss on exchange in relation to re-evaluations of cross-currency swaps in the Financial Sector Policy program activity. Public Debt program activity variance is attributable to a larger-than-expected decline in the stock of interest-bearing debt, as well as a lower-than-expected effective interest rate. The Domestic coinage program activity variance is due to a higher demand for coinage from the economy and the associated higher cost to produce and distribute coinage to meet this higher demand. See Table 6 for a corresponding increase in revenues associated with the sale of domestic coinage.

2. Federal-Provincial Relations and Social Policy Branch variances in the Transfer Payments to Provinces and Territories program activity are primarily attributable to an increase in Alternative Payments for Standing Programs of $182,016 thousand and an increase in Youth Allowances Recovery of $7,787 thousand.

3. The International Trade and Finance Branch variances between planned and actual numbers are attributable to unused Vote 5 funds of $88,602 thousand. Note that $5,594 thousand of this was transferred to Foreign Affairs and International Trade Canada. In addition the expenditure of $44,820 thousand for a net loss on exchange for international payments was not included in planned spending, nor was the non-budgetary vote L10 of $318,270 thousand for the issuance and payment of non-interest–bearing, non-negotiable demand notes to the International Development Association.

Table 8-A: User Fees Act

The following table reports on the user fees administered by the Department.

|

|

|

|

|

2006–07 |

||||

|

|

||||||||

| A. User Fee | Fee Type | Fee Setting Authority |

Date Last Modified |

Forecast Revenue |

Actual Revenue |

Full Cost |

Performance |

Performance Results |

|

Fees charged for the processing of access requests filed under the Access to Information Act |

Other goods and services |

Access to Information Act |

1992 |

8 |

14 |

770 |

Framework under development by the Treasury Board of Canada Secretariat For more information, see http://laws.justice. |

Statutory deadlines met 92% of the time |

|

Planning Years |

||

|

Fiscal Year |

Forecast Revenue ($000) |

Estimated Full Cost ($000) |

|

2007–08 2008–09 2009–10 |

14 14 14 |

972 971 971 |

|

B. Date Last Modified |

||

|

C. Other Information |

||

|

|

||

Table 8-B: Policy on Service Standards for External Fees

Supplementary information on the Policy can be found at

http://www.tbs-sct.gc.ca/rma/dpr3/06-07/index_e.asp.

Table 9: Major Regulatory Initiatives

Supplementary information on progress against the Department's regulatory plan can be found at http://www.tbs-sct.gc.ca/rma/dpr3/06-07/index_e.asp.

Table 10: Transfer Payment Programs (TPPs)

Supplementary information on TPPs can be found at http://www.tbs-sct.gc.ca/rma/dpr3/06-07/index_e.asp.

Table 11: Horizontal Initiatives

In 2006-07, the Department of Finance was the lead department on the following horizontal initiative: Anti-Money Laundering and Anti-Terrorist Financing Regime[3]

Supplementary information on horizontal initiatives can be found at http://www.tbs-sct.gc.ca/rma/dpr3/06-07/index_e.asp.

Table 12: Department of Finance Canada Financial Statements (unaudited) for the year ended March 31, 2007

Statement of Management Responsibility for Financial Statements

Responsibility for the integrity and objectivity of the accompanying financial statements for the year ended March 31, 2007, and all information contained in this report rests with departmental management. These financial statements have been prepared by management in accordance with Treasury Board accounting policies, which are consistent with Canadian generally accepted accounting principles for the public sector.

Management is responsible for the integrity and objectivity of the information in these financial statements. Some of the information in the financial statements is based on management's best estimates and judgment, and gives due consideration to materiality. To fulfil its accounting and reporting responsibilities, management maintains a set of accounts that provides a centralized record of the Department's financial transactions. Financial information submitted to the Public Accounts of Canada and included in the Department's DPR is consistent with these financial statements.

Management maintains a system of financial management and internal control designed to provide reasonable assurance that financial information is reliable, that assets are safeguarded, and that transactions are in accordance with the Financial Administration Act, are executed in accordance with prescribed regulations, within parliamentary authorities, and are properly recorded to maintain accountability of government funds. Management also seeks to ensure the objectivity and integrity of data in its financial statements through careful selection, training, and development of qualified staff, through organizational arrangements that provide appropriate divisions of responsibility, and through communication programs aimed at ensuring that regulations, policies, standards, and managerial authorities are understood throughout the Department.

The system of internal control is augmented by Internal Audit, which conducts periodic audits and reviews of different areas of the Department's operations. In addition, the Chief Audit Executive has free access to the Audit Committee, which oversees management's responsibilities for maintaining adequate control systems and the quality of financial reporting, and which recommends the financial statements to the Deputy Minister of Finance.

The financial statements of the Department have not been audited.

| The paper version was signed by | The paper version was signed by | |

|

Rob Wright, Deputy Minister |

Coleen Volk, Senior Financial Officer |

Department of Finance Canada

Statements of Operations (unaudited)

For the year ended March 31

($ thousands)

|

|

2007 |

2006 |

|

|

Expenses (note 4) |

|||

|

Transfer Payments to Provinces and Territories |

41,674,221 |

40,175,192 |

|

|

Public Debt |

34,108,504 |

33,535,120 |

|

|

International Financial Organizations (recovery) |

190,802 |

(409,967) |

|

|

Domestic Coinage |

128,035 |

125,729 |

|

|

Financial Sector Policy |

65,511 |

17,009 |

|

|

Tax Policy |

36,781 |

33,830 |

|

|

International Trade and Finance |

17,956 |

16,103 |

|

|

Federal-Provincial Relations and Social Policy |

17,719 |

15,522 |

|

|

Economic and Fiscal Policy |

17,325 |

16,121 |

|

|

Economic Development and Corporate Finance |

9,309 |

8,448 |

|

|

|

|||

|

Total Expenses |

76,266,163 |

73,533,107 |

|

|

|

|||

|

Revenues (note 5) |

|

|

|

|

Transfer Payments to Provinces and Territories |

205,063 |

209,105 |

|

|

International Financial Organizations |

36,768 |

613,691 |

|

|

Domestic Coinage |

226,843 |

212,943 |

|

|

Financial Sector Policy |

4,141,384 |

3,391,196 |

|

|

Economic Development and Corporate Finance |

158,070 |

201,126 |

|

|

|

|||

|

Total revenues |

4,768,128 |

4,628,061 |

|

|

|

|||

|

Net cost of operations |

71,498,035 |

68,905,046 |

|

|

|

|||

The accompanying notes form an integral part of these financial statements.

Department of Finance Canada

Statements of Financial Position (unaudited)

As at March 31

($ thousands)

|

|

2007 |

2006 |

||

|

Assets |

||||

|

Financial assets |

||||

| Accounts receivable (Note 6) |

6,777,102 |

7,876,767 |

||

| Coin inventory |

21,829 |

14,262 |

||

| Foreign exchange accounts (Note 7) |

44,178,099 |

40,826,522 |

||

| Investment in Crown corporations (Note 8) |

401,578 |

401,578 |

||

| Other loans, investments, and advances (Note 9) |

5,052,538 |

5,262,273 |

||

|

|

||||

|

56,431,146 |

54,381,402 |

|||

|

Non-financial assets |

|

|

||

|

Tangible capital assets (Note 10) |

3,548 |

3,770 |

||

|

|

||||

|

Total assets |

56,434,694 |

54,385,172 |

||

|

Liabilities |

|

|||

| Accounts payable and accrued liabilities (Note 11) |

4,056,295 |

4,683,538 |

||

| Taxes payable under tax collection agreements (Note 12) |

6,422,333 |

6,012,377 |

||

| Interest payable (Note 13) |

7,407,283 |

7,748,715 |

||

| Notes payable to international organizations (Note 14) |

359,761 |

367,052 |

||

| Matured debt (Note 15) |

108,961 |

126,175 |

||

| Unmatured debt (Note 16) |

411,548,404 |

418,912,371 |

||

| Other liabilities (Note 17) |

124,839 |

208,412 |

||

| Employee severance benefits (Note 18) |

13,604 |

12,995 |

||

|

|

||||

|

Total Liabilities |

430,041,480 |

438,071,635 |

||

|

Equity of Canada (Note 19) |

(373,606,786) |

(383,686,463) |

||

|

|

||||

|

Total liabilities and equity of Canada |

56,434,694 |

54,385,172 |

||

|

|

Contingent liabilities (Note 20) |

|

||

| Contractual obligations (Note 21) |

|

|||

The accompanying notes form an integral part of these financial statements

Department of Finance Canada

Statements of Equity of Canada (unaudited)

For the year ended March 31

($ thousands)

|

2007 |

2006 |

|

|

Equity of Canada, beginning of year |

(393,139,722) |

(395,958,378) |

|

Net cost of operations |

(68,905,046) |

(70,444,533) |

|

Current year appropriations used (Note 3) |

79,834,200 |

73,241,234 |

|

Revenue not available for spending |

(5,173,025) |

(6,835,610) |

|

Change in net position in the Consolidated Revenue Fund (Note 3) |

3,680,289 |

6,839,611 |

|

Services provided without charge by other government departments (Note 22) |

16,841 |

17,954 |

|

|

||

|

Equity of Canada, end of year |

(373,606,786) |

(383,686,463) |

|

|

||

The accompanying notes form an integral part of these financial statements.

Department of Finance Canada

Statements of Cash Flow (unaudited)

For the year ended March 31

($ thousands)

|

2007 |

2006 |

|||||||

|

Operating activities |

|

|

||||||

|

Net cost of operations |

71,498,035 |

68,905,046 |

||||||

|

Non-cash items: |

|

|

||||||

| Amortization of tangible capital assets |

(1,472) |

(1,488) |

||||||

| Amortization of loan discounts |

207,031 |

210,600 |

||||||

| Amortization of debt discounts and premiums |

(6,153,043) |

(5,289,353) |

||||||

| Concessionary portion of other loans, investments, and advances |

(241,856) |

(245,640) |

||||||

| Gain on disposition of securities |

1,715 |

1,740 |

||||||

| Gain on disposal of tangible capital assets |

8 |

- |

||||||

| Unrealized foreign exchange gains and losses |

(4,658) |

(793,466) |

||||||

| Realized foreign exchange gains and losses |

- |

1,000,000 |

||||||

| Services provided without charge |

(18,774) |

(16,841) |

||||||

|

Variations in assets and liabilities: |

|

|

||||||

| (Decrease) increase in accounts receivable |

(1,099,665) |

3,496,740 |

||||||

| Increase in coin inventory |

7,567 |

2,082 |

||||||

| Decrease in accounts payable and accrued liabilities |

626,634 |

2,000,088 |

||||||

|

|

Accounts payable and accrued liabilities |

626,923 |

2,000,053 |

|||||

| Vacation pay and compensatory leave |

320 |

1,101 |

||||||

| Employee severance benefits | (609) | (1,066) | ||||||

| Decrease in interest payable |

341,432 |

201,524 |

||||||

| Increase in taxes payable under tax collection agreements |

(409,956) |

(2,316,393) |

||||||

| Decrease (increase) in other liabilities |

83,573 |

(86,551) |

||||||

|

|

||||||||

|

Cash used in operating activities |

64,836,571 |

67,068,088 |

||||||

|

|

||||||||

|

Capital investment activities |

|

|

||||||

|

|

Acquisition of tangible capital assets |

1,808 |

3,172 |

|||||

|

|

Proceeds from disposal of tangible capital assets |

(566) |

(5) |

|||||

|

|

Cash used by capital investment activities |

1,242 |

3,167 |

|||||

|

Investing activities |

||||||||

|

|

Net advances to (settlements from) the Exchange Fund Account |

2,469,709 |

3,638,475 |

|||||

|

|

Issuance of notes payable to the International Monetary Fund |

(1,680,585) |

(2,645,000) |

|||||

|

|

Encashment of notes payable to the International Monetary Fund |

1,267,000 |

587,000 |

|||||

|

|

Payment of subscriptions to international financial institutions |

- |

6,043 |

|||||

|

|

Issuance of loans receivable |

1,375,401 |

1,586,545 |

|||||

|

|

Repayment of loans receivable |

(1,554,892) |

(1,699,985) |

|||||

|

|

||||||||

|

Cash used by investing activities |

1,876,633 |

1,473,078 |

||||||

|

|

||||||||

|

Financing activities |

||||||||

|

|

Encashment of notes payable to international organizations |

324,768 |

248,898 |

|||||

|

|

Issuance of note payable to international organizations |

(318,270) |

(318,270) |

|||||

|

|

Net proceeds from cross-currency swaps |

(183,919) |

102,487 |

|||||

|

|

Issuance of debt |

(355,819,562) |

(359,223,747) |

|||||

|

|

Repayment of debt |

370,841,475 |

368,987,763 |

|||||

|

|

Net cash provided by the Government of Canada |

(81,558,938) |

(78,341,464) |

|||||

|

|

||||||||

|

Cash used in (provided by) financing activities |

(66,714,446) |

(68,544,333) |

||||||

|

|

||||||||

The accompanying Notes form an integral part of these financial statements.

1. Authority and objectives

The Department of Finance Canada is established under the Financial Administration Act as a department of the Government of Canada.

The Department is headed by the Minister of Finance who has broad responsibility for the management and direction of the Department, the management of the Consolidated Revenue Fund (CRF), and the supervision, control, and direction of all matters relating to the financial affairs of Canada not by law assigned to the Treasury Board or to any other minister.

The goal of the Department of Finance Canada is to foster strong and sustainable economic growth, resulting in higher standards of living and an improved quality of life for Canadians. The core business of the Department is organized into the following program activities:

Transfer Payments to Provinces and Territories: Administers the transfer payments pursuant to statutes and agreements with provinces and territories.

Public Debt: Manages the funding of interest and service costs of the public debt and the issuing costs of new borrowing.

Domestic Coinage: Responsible for the payment of the production and distribution costs for domestic circulating coinage.

International Financial Organizations: Administers international financial obligations and subscriptions.

Tax Policy: Develops and evaluates federal taxation policies and legislation, and provides advice and recommendations for changes aimed at improving the tax system while raising the required amount of revenue to finance government priorities. This program focusses on the following areas: personal income tax, business income tax, and sales and excise tax. The program is also involved with negotiating tax treaties, tax policy research and evaluation, as well as federal-provincial-territorial and federal-Aboriginal tax coordination.

Financial Sector Policy: Provides policy analysis on Canada's financial sector and on the regulation of federally chartered financial institutions; manages the federal government's borrowing program; and provides support regarding Crown corporation and financial market and exchange rate policy.

Economic and Fiscal Policy: Analyzes Canada's economic and fiscal situation, advises on fiscal matters, and provides analytical support on a wide range of economic and financial issues related to the government's macroeconomic policies.

International Trade and Finance: Manages the Department of Finance Canada's participation in international financial institutions (including the IMF, the World Bank Group, the Organisation for Economic Co-operation and Development, and the European Bank for Reconstruction and Development), international groups such as the G7, G20, and the Asia–Pacific Economic Cooperation forum, as well as trade and investment policy issues.

Federal-Provincial Relations and Social Policy: Provides policy and advice on federal-provincial-territorial relations and social policy issues and their economic and fiscal implications.

Economic Development and Corporate Finance: Provides policy and advice regarding financial implications of the government's microeconomic policies and programs, proposals for funding of programs, sectoral policy analysis, and corporate restructuring regarding Crown corporations and other corporate holdings.

2. Significant Accounting Policies

The financial statements have been prepared in accordance with accounting standards issued by the Treasury Board of Canada Secretariat, which are consistent with Canadian generally accepted accounting principles for the public sector.

Significant accounting policies are as follows:

a) Parliamentary appropriations

The Department is financed by the Government of Canada through parliamentary appropriations. Appropriations provided to the Department do not parallel financial reporting according to generally accepted accounting principles since appropriations are primarily based on cash flow requirements. Consequently, items recognized in the Statement of Operations and in the Statement of Financial Position are not necessarily the same as those provided through appropriations from Parliament. Note 3 to these financial statements provides a high-level reconciliation between the two bases of reporting.

b) Consolidation

These financial statements include the accounts of Canada Investment and Savings, a special operating agency that administers retail debt. The accounts of Canada Investment and Savings have been consolidated with those of the Department of Finance Canada and all interorganizational balances and transactions have been eliminated.

The Government of Canada announced the winding up of Canada Investment and Savings as of the end of the fiscal year, March 31, 2007.

Investments in government business enterprises are recorded at cost and are not consolidated.

c) Net cash provided by the Government of Canada

The Department of Finance Canada operates within the Consolidated Revenue Fund (CRF). The CRF is administered by the Receiver General for Canada. All cash received by the Department is deposited to the CRF and all cash disbursements made by the Department are paid from the CRF. Net cash provided by the Government of Canada is the difference between all cash receipts and all cash disbursements, including transactions between departments of the Government of Canada.

d) Change in net position in the CRF

Change in net position in the CRF is the difference between net cash provided by the government and appropriations used in a year, excluding the amount of non-respendable revenue recorded by the Department. It results from timing differences between when a transaction affects appropriations and when it is processed through the CRF.

e) Special drawing rights and foreign currency transactions

A special drawing right (SDR) is an international reserve asset created by the IMF to supplement existing official international reserves of member countries. The value of a SDR is based on a basket of four major currencies: the euro, Japanese yen, pound sterling, and United States (U.S.) dollar. The composition of the basket is reviewed every five years to ensure that it is representative of the currencies used in international transactions and that the weights assigned to the currencies reflect their relative importance in the world's trading and financial systems.

Transactions involving foreign currencies and SDRs are translated into Canadian-dollar equivalents using rates of exchange in effect at the time of those transactions. Monetary assets and liabilities denominated in foreign currencies, and SDRs are translated into Canadian dollars at the exchange rate in effect at the balance sheet date.

Net losses resulting from foreign currency transactions are included in expenses—International Financial Organizations—in the statement of operations.

f) Revenues

Revenues are accounted for in the period in which the underlying transaction or event occurred that gave rise to the revenues:

- Interest on Receiver General bank deposits is recognized as revenue when earned.

- Uncashed Receiver General cheques and warrants and bank account cheques for all departments and agencies are recognized as revenue of the Department of Finance Canada if they remain outstanding 10 years after the date of issue.

- Unclaimed matured bonds are recognized as revenue if they remain unredeemed 15 years after the date of call or maturity, whichever is earlier.

- Unclaimed bank balances are recognized as revenue when there has been no owner activity in relation to the balance for a period of 20 years.

g) Expenses

Expenses are recorded on the accrual basis:

- Transfer payments are recorded as expenses when the recipient has met the eligibility criteria or fulfilled the terms of a contractual transfer agreement or, in the case of transactions that do not form part of an existing program, when the government announces a decision to make a non-recurring transfer, provided the enabling legislation or authorization for payment receives parliamentary approval prior to the completion of the financial statements.

- Public debt charges are recognized when incurred and include interest, amortization of debt discounts, premiums and commissions, and servicing and issue costs.

- Vacation pay and compensatory leave are expensed as the benefits accrue to employees under their respective terms of employment.

- Services provided without charge by other government departments for accommodation, the employer's contributions to health and dental insurance plans, and legal services are recorded as operating expenses at their estimated cost.

h) Employee future benefits

Pension benefits: Eligible employees participate in the Public Service Pension Plan, a multiemployer defined benefit pension plan administered by the Government of Canada. The Department's contributions to the Plan are expensed as incurred and represent the total departmental obligation to the Plan. Current legislation does not require the Department to make contributions for any actuarial deficiencies of the Plan.

Severance benefits: Employees are entitled to severance benefits under labour contracts or conditions of employment. These benefits are accrued as employees render the services necessary to earn them. The obligation relating to the benefits earned by employees is calculated using information derived from the results of the actuarially determined liability for employee severance benefits for the Government of Canada as a whole.

i) Accounts receivable

Accounts receivable are stated at the amounts expected to be ultimately realized. A provision is made for accounts receivable where the ultimate recovery is considered uncertain.

j) Inventory

Coin inventory is valued at the lower of cost and net realizable value, cost being determined by the average cost method.

k) Foreign exchange accounts

Short-term deposits, marketable securities, and special drawing rights held in the Foreign Exchange Accounts are recorded at cost. Marketable securities are adjusted for amortization of purchase discounts and premiums. Purchases and sales of securities are recorded at the settlement date. Write-downs to reflect other than temporary impairment in the fair value of securities are included in foreign exchange revenues on the Statement of Operations and Accumulated Deficit. Canada's subscriptions to the capital of the International Monetary Fund are recorded at cost.

l) Investments in Crown corporations

Investments in the Canada Development Investment Corporation are at cost.

Income from investments in Crown corporations includes dividends from the Bank of Canada and the Canada Development Investment Corporation, which is recognized when declared.

m) Other loans, investments, and advances

Subscriptions and contributions are recorded at cost net of allowances.

The Department of Finance Canada does not make a return on investment and does not expect a return of capital unless it withdraws from an institution, which is unlikely. Since the terms of the subscriptions and contributions are so concessionary that the substance of the transaction is that all or a part of the investment is more in the nature of a grant, the entire investment is recognized, through an allowance, as an expense at the time the investment is made.

Loans and advances are initially recorded at cost and are adjusted to reflect the concessionary terms of those loans made on a long-term, low interest, or interest-free basis and the portion of the loans that are expected to be repaid from future appropriations.

An allowance for valuation is further used to reduce the carrying value of loans, investments, and advances to amounts that approximate their net realizable value.

For loans to national governments, including developing countries, the allowance is determined based on the government's identification and evaluation of countries that have formally applied for debt service relief, on estimated probable losses that exist on the remaining portfolio, and on changes in the economic conditions of sovereign debtors.

For loans and advances to international organizations, an allowance is established based on their concessionary terms and their collectibility.

n) Derivative financial instruments

The Department of Finance Canada enters into interest rate and cross-currency swaps to facilitate the management of its debt structure.

Interest rate swaps are agreements where counterparties exchange fixed- and floating-rate interest payments based on notional principal amounts of a single currency. Cross-currency swaps are agreements where counterparties exchange fixed- or floating-rate interest payments and principal amounts in different currencies.

Interest rate swaps are used to convert fixed-rate debt into variable rates tied to the Banker's Acceptance rates or London Interbank Offered Rates. Cross-currency swaps are primarily used to convert domestic debt to foreign debt to fund foreign currency advances to the Exchange Fund Account. In certain cases, cross-currency swaps are used to convert foreign debt into U.S. dollar debt.

Cross-currency swaps are initially recorded at cost and are translated into Canadian dollars at the exchange rate in effect at the balance sheet date. For cross-currency swaps where domestic debt has been converted into foreign debt, any exchange gains or losses are offset by the exchange gains or losses on foreign currency advances to the Exchange Fund Account. For cross-currency swaps where foreign debt has been converted into U.S. dollar debt, any exchange gains or losses are offset by the exchange gains or losses on the applicable foreign debt.

Interest paid and payable, and interest received and receivable on all derivative financial instruments is included in interest on unmatured debt.

o) Tangible capital assets

All tangible capital assets and leasehold improvements having an initial cost of $10,000 or more are recorded at their acquisition cost. Amortization of tangible capital assets is done on a straight-line basis over the estimated useful life of the asset as follows:

|

Asset class |

Amortization period |

|

Machinery and equipment |

3 to 5 years |

|

Motor vehicles |

3 years |

|

Leasehold improvements |

Lesser of the remaining term of the lease or useful life of the improvement |

|

Assets under construction |

Once in service, in accordance with asset class |

|

|

|

p) Taxes receivable and taxes payable under tax collection agreements

Pursuant to various tax collection agreements, the Canada Revenue Agency administers and collects personal income taxes, corporate income taxes, Harmonized Sales Tax, First Nations Sales Tax, and First Nations Goods and Services Tax on behalf of certain provincial, territorial, and Aboriginal governments and the Department of Finance Canada remits those taxes to the applicable government.

Taxes receivable include taxes collectible by the Canada Revenue Agency on behalf of provincial, territorial, or Aboriginal governments that have not yet been remitted to the Department and are included in Accounts Receivable in the Statement of Financial Position. Taxes payable include taxes that have not yet been remitted by the Department to the applicable provincial, territorial, or Aboriginal government.

Taxes receivable and taxes payable include amounts assessed by the Canada Revenue Agency and estimates of amounts not assessed based on cash received, and include adjustments between estimated taxes receivable and taxes payable from previous years and actual amounts, as well as adjustments from reassessments.

q) Unmatured debt

Premiums and discounts on public debt are amortized on a straight line basis over the term to maturity of the respective debt instrument. The corresponding amortization is recorded as part of public debt charges.

r) Other liabilities

Deposits from Crown corporations that are non-interest bearing and repayable are recorded in "Other liabilities."

The common school funds account was established under 12 Victoria 1849,Chapter 200, to record the proceeds from the sale of lands set apart for the support and maintenance of common schools in Upper and Lower Canada, now Ontario and Quebec.

The foreign claims fund account was established by Vote 22a, Appropriation Act No. 9, 1966 to record the money received from the Custodian of Enemy Property.

The War Claims Fund—World War II account was established by Vote 696, Appropriation Act No. 4, 1952 to record moneys received from the Custodian of Enemy Property or from other sources.

s) Loan guarantees

The allowance for losses on the guarantees of the Canadian Wheat Board and Export Development Canada is determined based on the government's identification and evaluation of countries that have formally applied for debt relief, estimated probable losses that exist on the remaining portfolio, and changes in the economic conditions of sovereign debtors.

t) Contingent liabilities

Contingent liabilities are potential liabilities that may become actual liabilities when one or more future events occur or fail to occur. To the extent that the future event is likely to occur or fail to occur and a reasonable estimate of the loss can be made, an estimated liability is accrued and an expense is recorded. If the likelihood is not determinable or an amount cannot be reasonably estimated, the contingency is disclosed in the Notes to the financial statements.

u) Measurement uncertainty

The preparation of these financial statements requires management to make estimates and assumptions that affect the reported amount of assets, liabilities, revenues, and expenses reported in the Financial Statements. At the time of preparation of these statements, management believes the estimates and assumptions to be reasonable.

The most significant items where estimates are used are contingent liabilities, valuation allowances for loans receivable, discounts on loans receivable, transfer payments to provinces and territories, the liability for employee severance benefits and accruals of taxes receivable, and taxes payable under tax collection agreements. Actual results could differ from those estimated. Management's estimates are reviewed periodically and, as adjustments become necessary, they are recorded in the financial statements in the year they become known.

3. Parliamentary Appropriations

The Department receives most of its funding through annual parliamentary appropriations. Items recognized in the Statement of Operations and the Statement of Financial Position in one year may be funded through parliamentary appropriations in prior, current, or future years. Accordingly, the Department has different net results of operations for the year on a government-funding basis than on an accrual accounting basis. The differences are reconciled in the following tables:

a) Reconciliation of net cost of operations to appropriations used:

|

2007 |

2006 |

|||||||

|

($ thousands) |