Guideline on the Attribution of Internal Services

1. Introduction

The purpose of this guideline is to provide a common approach to calculating the cost of delivering a government program that includes an attribution of internal service costs.

The attribution of internal services to programs is a key step to producing historical program cost information. In calculating historical program cost information, departments may wish or may be required to include program expenditures as reported in the department's PAA plus an attribution of the department's internal service expenditures to each program.

Historical program cost information does not provide departments with a constant metric that would substantiate new funding requests on its own merit. Instead, historical program costs can provide information to support the department in understanding the costs of their programs and serve as a reasonable starting point for a discussion about resource requirements and cost drivers.

Cost Driver: Is an operational metric that varies in direct relation to the quantity of internal services that are consumed by a program. A common cost driver is FTEs. For example, the quantity of human resources management and information technology services that are consumed by a program often varies in direct relation to the number of employees in the program.

The production of historical program cost information described in this section is not mandatory, does not affect the recording requirements defined in Section 6, and does not affect the reporting of expenditure information by PAA in the Reports on Plans and Priorities, Departmental Performance Reports and the Public Accounts of Canada.

2. Effective Date

This guideline is effective on February 29, 2016.

The content of this guideline was originally issued as appendix C of the Guide on Internal Services Expenditures: Recording, Reporting and Attributing in April 2014. Appendix C was removed to avoid confusion between the Internal Services accounting requirements described in the rest of the Guide, and the content of the appendix which described an approach to costing a government program that included Internal Service costs.

3. Roles and Responsibilities

The chief financial officer (CFO) is accountable for ensuring that the methodology used by a department to produce historical program cost information is consistent with these guidelines and the Secretariat's Guidelines on Costing. The CFO is also responsible for supporting senior departmental managers in the production and analysis of historical program cost information.

Senior departmental managers are responsible for ensuring that historical program cost information is produced in a manner consistent with direction from the CFO. Senior departmental managers are also responsible for ensuring that their managers collaborate with internal service managers and the chief financial officer's organization during the production of historical program cost information in order to ensure the information is complete and accurate.

4. Principles for Producing Historical Program Cost Information

The following generally accepted management accounting principles should be used when producing historical program cost information.

- Consistency

- It is essential that historical program cost information is produced in a consistent manner. If there is a change in the department's PAA or in the way it produces the historical program cost information, the nature and rationale for the change should be documented and the impact of the change identified and quantified. Depending on the nature and significance of the change, the department should consider recalculating prior years' historical program cost information when required.

- Cost-effectiveness

- Since an investment of resources is required to produce historical program cost information, there should be a balance between the cost to produce the information and the value of the information.

- Materiality

- When establishing the methodology for attributing internal service costs to a specific program, materiality should be a consideration.

- Reasonableness (i.e., perceived fairness)

- It is important that program managers and internal service managers understand the methodology used and any compromises made to ensure that the methodology is cost-effective. They need to perceive that the resulting attribution of costs is reasonable and fair.

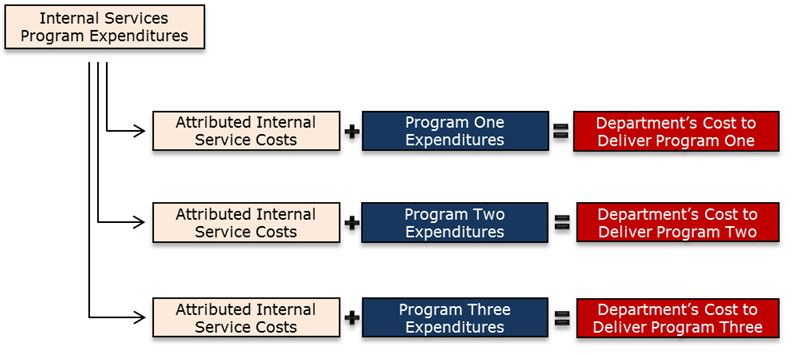

5. Attribution of Internal Service Costs

The production of historical program cost information is based on the department's existing expenditure data (i.e., charges to the department's appropriation). Expenditure data should be compiled according to the department's PAA, as presented in Section 6.

After the expenditure data has been gathered, Internal Services program costs are attributed to other programs in order to determine the department's cost to deliver each specific program.

The cost of internal services is attributed to other programs through the two-step process described below. The process can be used to attribute internal service costs to a program, sub-program or sub-sub-program, depending on the level of detail required.

First Step: Direct Attribution of Internal Service Costs

The direct attribution process involves identifying internal service costs that were incurred solely to support a specific program.

Example 1: A promotional campaign in support of a specific program is being conducted. In this case, the communications services costs associated with the salaries of the employees assigned to work on the campaign and the contract costs with media outlets would be directly attributed to the program.

The principle of materiality is an important consideration when identifying internal service costs for direct attribution. When an internal service cost is incurred to support a specific program and is material, it should be directly attributed to that program. If the cost is not material, it would be more cost-effective to attribute the cost indirectly through a cost pool, as described in the second step. Determining whether a cost is material requires professional judgment and, when required, should involve the Office of the Chief Financial Officer.

Example 2: In many organizations, the cost of human resources activities to support the regular staffing of vacant positions is small enough to be considered immaterial. In this case, it would be more cost-effective to group these costs with other similar costs in a cost pool and then attribute them across all other programs.

After all material internal service costs are directly attributed to a program, the remaining internal service costs are attributed across all programs in the second step.

Second Step: Cost-Pool Attribution of Internal Service Costs

In order to efficiently attribute the remaining internal service costs to the other programs, the remaining costs should be accumulated into one or more cost pools.

Cost Pool: Is a grouping of homogeneous or like costs. Costs are like each other when they vary for similar reasons and at similar rates. For the sake of efficiency, costs are accumulated into cost pools to facilitate the attribution process and to accommodate different methods of attribution.

The following considerations apply when establishing cost-pool attribution methodologies:

- Generally, the number of cost pools should be kept to a minimum.

- Many internal service costs vary in direct relation to the number of employees; therefore, these costs could be grouped into a single cost pool, and the pool would be attributed based on the number of employees in each program.

- Some internal services do not vary in relation to the number of employees, such as legal services and communications services. The consumption of these internal services may be tracked using different metrics that provide a reasonable basis for attributing these costs (e.g., hours worked per file).

- Some organizations track operational data that relate directly to the consumption of internal service resources. For example, departments may track the number of external inspections performed. If departments know the relationship between the number of inspections and the level of internal service support required, they can use the number of inspections to attribute the relevant pool of costs. Documented operational data that relate directly to internal service consumption are an effective basis for attributing internal service cost pools.

- The number of cost pools and the attribution methodology should take into consideration whether the amounts are material and whether the subsequent production of historical program cost information will be cost-effective.

- Only one method of attribution should be used for each cost pool.

- If there are residual internal service costs that have no identifiable relationship with other programs, or that are immaterial, they should be included in the largest internal service cost pool (i.e., based on dollar value). Including residual costs in the largest cost pool will minimize the possibility that they could distort program costs.

6. Producing Historical Program Cost Information

The following diagram illustrates how to produce historical program cost information.

Methodology

When departments are developing their methodology for producing historical program cost information, the key considerations are as follows:

- The methodology is consistent with the guidance on attribution of internal service costs presented in the section Attribution of Internal Service Costs of this appendix;

- It uses expenditure data that reconciles at the program level to the department's Program Activity table in Volume II of the Public Accounts of Canada. It does not include services provided without charge by other departments and services that are centrally funded;

- The methodology is internally consistent. For example, when a cost pool of internal services is attributed to specific programs on the basis of the number of FTEs, the cost pool should be attributed to all levels of the PAA on the same basis;

- It is documented, endorsed by the CFO and periodically reviewed. If a review results in changes to the methodology, then the changes, a rationale for the changes, and their impact should be documented; and

- The methodology produces information at the lowest level of the PAA. If program cost information is required at a higher PAA level, the higher-level cost information should be a summary or roll-up of the lower-level cost information.

For an example of how to produce historical program cost information, see the final section of this appendix, Example for Producing Historical Program Cost Information.

Other considerations

While financial management systems are capable of recording expenditures in a department's general ledger, not all systems can support the extraction and analysis of this data to produce historical program cost information. In such cases, departments may need to produce and maintain information about the attribution of internal service costs and the resulting historical program cost information outside of their financial management system. In all cases, extracted data should be traceable back to the initial expenditure data in the general ledger. In the long term, the objective is to have departments produce and retain this information in their financial management system.

When historical program cost information is based on expenditure data for an incomplete fiscal year, the user should be provided with comparable information from previous fiscal years. In light of variations that may occur between a single point in time during the year and the fiscal year-end, it is recommended that in addition to partial-year analysis and comparable information from previous years, an explanation be provided for any material variations caused by timing.

7. Producing More Granular Historical Cost Information

When there is a requirement to produce historical cost information for activities that represent a component below the lowest level of an organization's PAA, the information should be produced in a manner that is consistent with the methodology used to attribute internal service costs to other programs.

The output should also be the same. The process for producing more granular information involves producing separate information on the internal service costs incurred to support the more granular activity, as well as a record of the expenditures for the specific activity itself.

8. Analyzing Historical Program Costs

Analyzing program costs at a single point in time is of limited value. Analyzing and understanding when, how and why program costs have changed over time is a strong basis for effective resource management at all levels of government. It provides a valuable understanding for why resources have been consumed in delivering a program.

The analysis of historical program cost information provides valuable insights into the relationship between costs, activity levels and program characteristics. Generally, the relationships between cost and activity are described as variable, fixed or step. These distinctions are important to a manager's understanding of their costs. Appendix A provides definitions of these three terms.

With knowledge of historical program costs, managers are in a stronger position to effectively manage day-to-day operations because they understand the financial implications of their decisions. They are able to:

- Explain why the internal service costs of one program are different from another; and

- Identify opportunities for cost-containment, where the costs of one program exceed the costs of a comparable program.

This knowledge is a good basis for starting to plan program changes, to understand the potential resource implications of various options and to estimate the cost of implementing the recommended option.

9. Context That Explains Cost

In addition to producing historical program cost information (the cost figures described in the section Production of Historical Program Cost Information of this appendix), departments should compile, analyze and report on relevant contextual information to assist users in understanding the historical program cost information they receive. Contextual information is relevant if it offers insight into the cost of a program or can help explain why the cost of one program is more or less than the cost of another program.

Relevant contextual information could include operational data such as the number of staff or the number or complexity of transactions. This context is relevant if a change in the numbers can impact the cost of a program. Context could also include qualitative information that describes the characteristics of a program, such as program delivery that is decentralized versus centralized. Such qualitative information can help explain unique cost elements.

10. Enquiries

Please direct enquiries about this guideline to your departmental headquarters. For support on this guidance, departmental headquarters should contact:

Financial Management Sector

Office of the Comptroller General

Treasury Board of Canada Secretariat

Ottawa ON K1A 0R5

For public enquiries regarding this guideline, please contact TBS Public Enquiries.

Annexe A : Definitions

- Activity (activité)

- An operation or work process internal to a program that uses inputs to produce outputs (e.g., training, research, construction, negotiation, or investigation).

- Cost Driver (facteur de coût)

- Is an operational metric that varies in direct relation to the quantity of internal services that are consumed by a program.

- Cost Pool (regroupement de coûts)

- Is a grouping of homogeneous or like costs. Costs are like each other when they vary for similar reasons and at similar rates.

- Department (ministère)

- All departments as defined in section 2 of the Financial Administration Act.

- Fixed Cost (coût fixe)

- A cost that remains constant regardless of changes in the volume of an activity. A good example is the cost of heating. Generally, the cost of heating an existing office space will not change with a change in the number of staff.

- Internal Services (services internes)

- Groups of related activities and resources that are administered to support the needs of programs and other corporate obligations of an organization. Internal services include only those activities and resources that apply across an organization, and not those provided to a specific program. The groups of activities are: Management and Oversight Services; Communications Services; Legal Services; Human Resources Management Services; Financial Management Services; Information Management Services; Information Technology Services; Real Property Services; Materiel Services; and Acquisition Services.

- Internal Support Services (services de soutien internes)

- Are administrative services provided by one department to another under the authority of section 29.2 of the Financial Administration Act. They include administrative activities that support human resources management services, financial management services, information management services, information technology services, communications services, real property services, materiel services, acquisition services or any other administrative service that is designated as such by order of the Governor in Council.

- Program (programme)

- A group of related resource inputs and activities that are managed to meet specific needs and to achieve intended results, and that are treated as a budgetary unit.

- Program Alignment Architecture (PAA) (architecture d'alignement des programmes)

- An inventory of all the programs undertaken by a department. The programs are depicted in their logical relationship to each other and to the strategic outcomes to which they contribute. The PAA is the initial document for establishing a Management, Resources, and Results Structure.

- Program Support Costs (coûts de soutien au programme)

- Are the costs of a program incurred in the performance of work that is not directly involved with service delivery, but that supports service delivery activities. Program support includes supervisory, administrative, management, and policy functions within a program branch. These costs may be incurred within the program branches at headquarters or in the regions. Program support costs are separate and distinct from internal service costs.

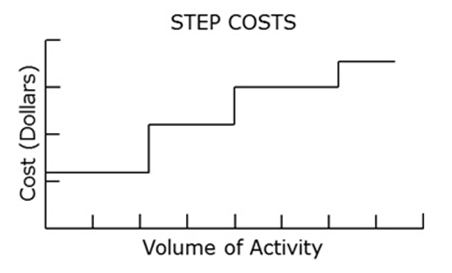

- Step Costs (coûts par paliers)

Costs that do not change steadily with changes in activity volume. Instead these costs are fixed over a range of activity and change when activity levels pass a specific activity volume. For example, supervision costs are fixed for a given range of supervised employees, but once the maximum ratio of staff to supervisor is exceeded, an additional supervisor would need to be hired. This leads to added supervisory costs in a lump-sum fashion, illustrated in the diagram below.

Organizations need to be aware of step costs when planning for an increase in activity that could cause an incremental step cost. Conversely, they should also be aware of step costs when activity levels decline, so that costs can be reduced where possible.

- Strategic Outcome (résultat stratégique)

- A long-term and enduring benefit to Canadians that stems from a department's mandate and vision. It represents the difference that a department intends to make for Canadians. Strategic outcomes should be measurable and reflect the department's sphere of influence.

- Variable Cost (coût variable)

- A cost that changes in proportion to changes in the volume of activity. A good example is the cost of stamps, which varies in relation to the volume of mailings.

Annexe B : Example for Producing Historical Program Cost Information

The purpose here is to provide a scenario that illustrates how to produce historical program cost information through the application of the methodology described in this appendix. The scenario illustrates the production of historical program cost information at the lowest level of the PAA.

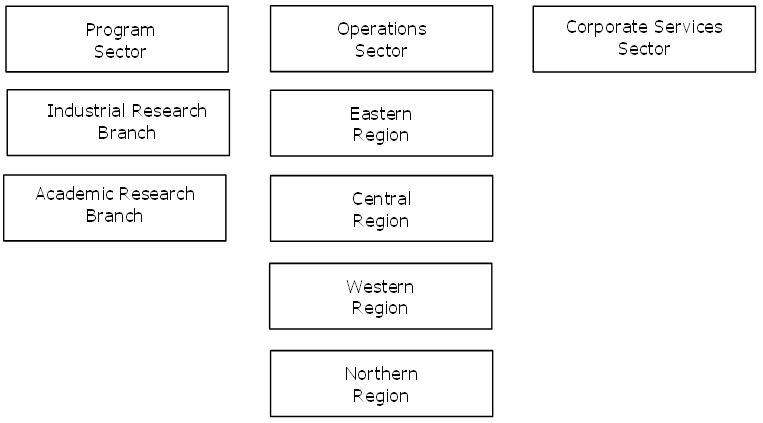

Scenario Department

This scenario is based on a department that has the following organization chart, personnel and Program Alignment Architecture (PAA). The organization chart shows that the scenario department has three sectors managed by assistant deputy ministers, and two branches and four regions managed by directors general.

Table 1 provides the complement of full-time equivalents (FTEs) and the budget for each organizational unit.

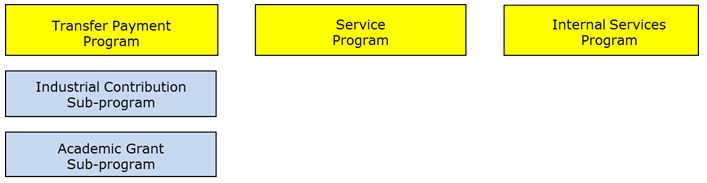

As illustrated in Figure 4, this organization's PAA has three programs and two sub-programs.

| Organization | FTEs | Budget |

|---|---|---|

| Program Sector | 3 | $4 |

| Industrial Research | 5 | $100 |

| Academic Research | 5 | $75 |

| Operations Sector | 5 | $7 |

| Eastern Region | 12 | $140 |

| Central Region | 12 | $140 |

| Western Region | 12 | $140 |

| Northern Region | 6 | $80 |

| Corporate Services Sector | 12 | $56 |

| Grand Total | 72 | $742 |

The Methodology for Producing Historical Program Cost Information

In this scenario, the objective is to determine the department's full cost to deliver its programs (i.e., all programs except the Internal Services Program) at the lowest level of the PAA. These programs are the Transfer Payment Program and the Service Program. As discussed in the previous section Producing Historical Program Cost Information, the department's full cost to deliver a program includes the expenditures of the program plus an attribution of internal service costs.

Table 2 presents the scenario department's expenditures summarized by program as defined in its PAA.

| Industrial Contribution Sub-Program | Academic Grant Sub-Program | Service Program | Internal Services Program | |

|---|---|---|---|---|

Table 2 Notes

| ||||

| Expenditures Summarized by Program | $100 | $75 | $500 | $67table 2 note * |

The attribution of internal service costs is a two-step process. Completing the first step involves reviewing all internal service costs, identifying any material internal service costs that were incurred to support a specific program, and attributing these costs to the that program.

Table 3 presents a summary of the review results and the direct attributions that were identified.

| Dedicated communications FTEs attributed to the Industrial Contribution Sub-Program | $5 |

|---|---|

| Legal consultation cost attributed to the Academic Grant Sub-Program | $2 |

| Recipient audits attributed to the Service Program | $17 |

| Total | $24 |

The historical program cost table is then updated to include these direct attributions, as illustrated in Table 4.

| Industrial Contribution Sub-Program | Academic Grant Sub-Program | Service Program | Internal Services Program | |

|---|---|---|---|---|

| Expenditures Summarized by Program | $100 | $75 | $500 | $67 |

| Step 1: Direct Attributions | $5 | $2 | $17 | -$24 |

| Residual Internal Service Costs | $43 |

Completing the second step of the process involves accumulating the residual internal service costs into pools to facilitate the attribution process and to accommodate different methods of attribution. There would normally be more than one cost pool, but this scenario will use only one in order to focus on the approach.

The total residual value of internal service expenditures from the first step (i.e., $43) is grouped into a cost pool. The total value of the cost pool is then attributed based on the number of FTEs.

Table 5 illustrates the attribution process.

| Industrial Contribution Sub-Program | Academic Grant Sub-Program | Service Program | |

|---|---|---|---|

Table 5 Notes

| |||

| Program FTEstable 5 note * | 5 | 5 | 42 |

| Attribution based on the proportion of program FTEs | 5/52 of $43 | 5/52 of $43 | 42/52 of $43 |

| Cost-pool attribution | $4 | $4 | $35 |

The historical program cost table is then updated to include these cost-pool attributions as illustrated in Table 6.

| Industrial Contribution Sub-Program | Academic Grant Sub-Program | Service Program | Internal Services Program | |

|---|---|---|---|---|

| Expenditures Summarized by Program | $100 | $75 | $500 | $67 |

| Step 1: Direct Attribution | 5 | 2 | 17 | -24 |

| Step 2: Cost-Pool Attribution | 4 | 4 | 35 | -43 |

| Attributed Internal Service Costs | 9 | 6 | 52 | -67 |

| Historical Program Costs | $109 | $81 | $552 | 0 |

Summary of Scenario Results

The historical program costs for the scenario department at the lowest level of the PAA are as follows:

- Industrial Contribution Sub-Program—$109

- Academic Grant Sub-Program—$81

- Service Program—$552

© His Majesty the King in right of Canada, represented by the President of the Treasury Board, 2017,

ISBN: 978-0-660-09532-5