Archived - Guidelines on Costing

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Note to reader

The Guidelines on Costing supersede the Guide to Costing.

1. About the Guidelines

These guidelines are intended to inform discussions about costing and to facilitate collaboration by all parties involved throughout the costing process.

The Guidelines explain the fundamentals of costing, describe common applications of costing in government, and outline key principles and practices. They provide general guidance that includes a seven-step approach to costing that departments are encouraged to use. The Guidelines also provide links to specific guidance on costing-related matters, such as the attestation provided by chief financial officers (CFOs) for Cabinet submissions.

2. Fundamentals of Costing

2.1 What is cost and what is costing?

- Cost

- Is the value of the resources (human, physical or financial) consumed to achieve a certain end (e.g., to produce a product, to deliver a service, or develop and implement a new system).

- Costing

- Is a management function that involves compiling cost information to serve a specific purpose.

2.2 Why is costing important?

Costing is important because cost information helps managers at all levels understand the financial impact of the decisions they make and the initiatives they propose. They need to know how the costs will change when the nature or level of an activity changes.

Costing can provide answers to a wide range of questions, including the following:

- What will it cost to deliver the new program?

- What additional costs will be incurred if we provide a higher quality of service or alter the type of service?

- What is the cost of providing a service in my region compared with the cost of providing the same service in another region?

- What are the current costs of providing a service and do they align with the fee that was established several years ago?

- What is the total cost of a collaborative arrangement with another department and what is my department's share?

- What is the cost of re-engineering the existing system?

High-quality, timely cost information supports decision making and performance monitoring, and enhances transparency. It is essential for CFOs' attestation on the financial implications of memoranda to Cabinet and Treasury Board submissions. In certain situations it could be used to substantiate the CFO sign-off on financial statements and reports to Parliament.

2.3 Costing, pricing and funding

Although they are related, costing, pricing and funding are different concepts.

- Costing

- Is the compiling of cost information to serve a specific purpose, such as determining the cost of providing a service, aligning resources with results, measuring performance, evaluating efficiency or reallocating resources.

- Price

- Is the amount that is charged for a good or service. The price the government charges for a good or service is based on the cost of providing that good or service. The government cannot charge more than cost, but it can charge less than cost in order to, for example, ensure fairness, minimize economic impact on clients, and achieve policy objectives.

- Funding

- Is the allocation of money to a manager's budget or to a department's reference levels based on government priorities. If there is a gap between the cost of a program and the funding available, management must take action to align planned activities with the funding available. The amount of funding can also depend on revenues from fees in cases where an organization has the authority to spend revenues.

3. Common Applications

The following are the common applications of costing in government.

Level-of-service decisions

When deciding what level of service to provide, decision makers can use costing to help identify which costs will change if the level of service changes and which costs will not change. For example, a decision to provide a lower level of service may reduce salary and other operating costs.

Decisions about offering a new service or program

When deciding whether to offer a new service or program, decision makers can use costing to help identify new costs but also existing costs that could change. For example, offering a new service might increase costs for internal services such as communications or legal services; it might also affect the cost of services provided without charge by other government departments.

Cost-benefit decisions

When deciding between two courses of action (e.g., upgrade an existing computer or acquire a new one), costing can be used to support a cost-benefit analysis for each.

Capital investment decisions

When making decisions relating to the building, betterment or acquisition of capital assets, decision makers can use costing to help identify and estimate planning, acquisition, maintenance, operating, and disposal costs. For specific guidance on capital investment decisions, refer to the Guideline on Cost Estimation for Capital Asset Acquisitions .

Legislative or policy change

When considering a proposed change in legislation or policy, decision makers are provided with a costing analysis of the proposal to assist them in understanding the scope and financial impact of the change and to ensure adequate resources are available to implement and sustain the change.

Cost-recovery decisions

When deciding how much to charge for a product or service in order to cover all or part of the cost of delivering it, decision makers can use costing to help identify all of the relevant costs and then determine the full cost of delivery.

Decisions about reorganizations

When making decisions about interdepartmental reorganizations or about establishing a new organization, decision makers can use costing to help make sure that all parties involved understand all the cost implications and to ensure that the resulting reference levels will be appropriate.

"Make-or-buy" decisions

When a department is deciding whether to "make" a product or service or whether to "buy" it—in other words, to develop a product or deliver a service itself or to have another department or organization (e.g., a private company) do so—decision makers can use costing to determine both the one-time and the ongoing costs of each option.

4. Principles

Everyone who is involved in a costing exercise should have a basic understanding of the following principles.

Costing requires consultation and judgment.

Changes to a program usually affect more than one organizational unit in a department and can affect other departments, so costing cannot be done in isolation. It requires consultation–sometimes, extensive consultation.

Before starting a costing exercise, managers should consult their department's CFO organization. The CFO organization can provide advice on costing and help ensure a balance between the level of effort required to produce the cost information and the value of the information to the decision maker.

Costing must be done for a specific purpose.

Cost information must be compiled to serve a specific purpose. Before starting a costing exercise, the parties involved must agree on why the exercise is being conducted (i.e., the purpose it will serve and what decision the cost information will inform); different purposes require different information.

Costing should be done consistently for costing exercises that have the same purpose.

If the circumstances are similar and the cost information will serve the same purpose, costing should be done consistently so that the resulting information will be comparable.

Costs do not always vary in proportion to changes in the level of activity.

Costs can be affected by changes in the level of activity in three main ways:

- Costs can change in proportion to changes in the level of activity (variable costs).

- Costs can remain constant regardless of changes in the level of activity (fixed costs).

- Costs can remain constant within a particular range of activity but change when the level of activity passes a specific amount (step-variable costs).

Data used in a costing exercise must be of high quality.

The quality of the data used in a costing exercise directly affects the quality of the information that decision makers receive. Data must be reasonable, consistent, defensible, reconcilable and current. The CFO organization can recommend appropriate data sources based on the purpose of the costing exercise and on the available data.

The benefits of cost information must be balanced against the cost of producing it.

When developing a costing methodology, departments must strive to balance elements such as level of detail, timeliness, accuracy and complexity with the cost of producing the cost information. Departments' costing practices must meet their needs, but the practices must also be sustainable. The investment made to produce cost information should not exceed the benefits the information provides.

5. A seven-step approach to costing

This toolkit sets out a seven-step approach to costing, and provides templates and checklists to help you apply the approach.

The approach can be adapted to the diverse mandates and operating environments found in government. If you use it consistently, you will be able to provide high-quality cost information to managers.

In addition to using a consistent approach to costing, you are encouraged to use national or international standards where appropriate to improve the comparative value of cost information (e.g., standards related to work-breakdown and cost-breakdown structures).

Seven Steps to Costing

This toolkit breaks the costing process down into the following seven steps, which are explained in detail in the rest of Section 5:

- Determine the purpose of the costing exercise. (i.e., What decision will the cost information be used to support?)

- Define the cost objects. (e.g., Are you costing an activity, an output or a service?)

- Determine the cost base. (e.g., Will you use historical expenditure information for an existing service as the basis for estimating the cost of a new service that is similar, assuming the same costs are relevant?)

- Classify the costs by whether they are directly or indirectly related to the cost objects. (e.g., The salary of a service centre employee is directly related to the cost of delivering the service. The cost of heating and cooling the building in which the service centre is located is indirectly related to the cost of delivering the service.)

- Attribute costs to the cost objects. (e.g., attributing a cost that is indirectly related to the cost object requires an understanding of how the cost will change in relation to changes in the cost object. For example, the cost of heating and cooling a service centre might change if the number of staff is doubled, but it will not change if staff increases by one or two people.)

- Validate and confirm the results of the costing exercise.

- Get sign-off on the results of the costing exercise from the appropriate authorities.

Step 1 – Determine the purpose of the costing exercise

Key questions: Why is this costing exercise being conducted? What is the purpose of the information that is being gathered? How will the information be used?

Unless you know how the information will be used and why, you will not be able to determine the scope of the exercise and what costs are relevant. For example, are you trying to calculate the cost of procuring a particular asset; or are you trying to calculate the cost of owning the asset over its entire life-cycle?

The following are three common purposes for which cost information is produced:

- 1. To determine resource allocations

- Decision makers will use the information to set resource levels for a new program or initiative, to fund an increase in the level of service, to estimate savings that will result from discontinuing an activity, to fund a system change, or to determine what costs should be recovered through a fee.

- 2. To decide on a program delivery option

- Decision makers will use the information to help them decide between alternatives.

- 3. To measure and evaluate performance

- Decision makers will use the information to assess performance.

You need to understand the purpose of the costing exercise because how the information will be used and whether it is intended to meet ad hoc or ongoing requirements influences the rest of the steps in the costing process.

Responsibilities

Managers at all levels are responsible for assisting with the development of the cost information that is used to support decisions. Managers are also responsible for understanding how their decisions affect their departments' overall costs.

During this step, the CFO organization ensures that all stakeholders have a common understanding of the purpose that the cost information is intended to serve, and that the cost information produced will meet any applicable central agency requirement. The CFO organization also assesses the feasibility of producing the required cost information. This assessment includes reviewing data sources, and if no data exist, determining how to collect the necessary data.

Purpose Statement

Once you have determined the purpose of the costing exercise, draft a purpose statement that includes the following information:

- The decision the cost information will support;

- The overarching assumptions that have been made;

- The information that is required to support the decision and the source(s) of data that will be used;

- The time period that will be covered; and

- How often the information will be produced.

Once the purpose statement has been drafted, the end-user of the information should review and approve it.

If the purpose changes later in the costing process, all steps completed up to that point must be revisited.

Tips

Don't rush through defining the purpose. Time and effort spent up front will make it easier to complete the remaining steps in the process.

When costing horizontal initiatives, develop the purpose statement in consultation with all parties before proceeding.

Common Purposes

This is a list of the common purposes that cost information serves in government and may help you draft a purpose statement. The list is not comprehensive.

Resource allocation

- New program

- Start-up

- Ongoing operation

- Changes to existing program

- One-time costs

- Demand

- Service standards

- Capital investment

- Life-cycle costs

- One-time costs

- Cost reduction

- Reduced services

- Reduced overhead

- Discontinuance

- Other cost reduction

- Cost avoidance

- Reducing future costs

- Reallocations

- Current year

- Future years

Performance measurement

- Cost efficiency

- Cost per output

- Cost effectiveness

- Cost per outcome

- Benchmarking

- Cost of identical entity

- Cost of similar entity

Program delivery options

- In-house vs. outsourced

- Collaborative and shared services

- Discontinuance

- One-time costs

- Costs that remain

Cost recovery

- Full cost

- Incremental cost

Purpose Checklist

- What management decisions will the cost information support?

- What business issues triggered the need for the cost information?

- Did you consider any central agency, legislative or policy requirements that could affect the purpose of the costing exercise? If so, describe them. If not, why not?

- Who are the stakeholders in the costing exercise? Did you consult them in drafting the purpose statement? If not, why not?

- Will the initiative that is being costed affect any other departments? If so, have they been consulted?

- What time period will the costing exercise cover?

- What assumptions were made in defining the purpose of the costing exercise? Are they documented in the purpose statement, along with the supporting rationale?

- What type of cost information is required (e.g., incremental costs, full costs or both)?

- Is the cost information needed to meet a one-time or a recurring requirement? If it is needed to meet a recurring requirement, specify the frequency.

- Have the end-users of the information confirmed their agreement with the purpose?

- Have you documented the purpose statement?

Step 2 – Define the cost objects

Key question: What is being costed?

A cost object is anything that needs to be costed. For example, it can be an activity, a product, a service or program outcome.

A costing exercise can have more than one cost object. For example, if the purpose of a costing exercise is to compare the cost of the internal services consumed by each of a department's six program branches, there will be six cost objects.

The cost objects for a costing exercise must align with the purpose you identified in Step 1: they must serve the purpose.

Cost objects can include the following:

- Organization (e.g., a department and its units);

- Programs (e.g., business lines);

- Processes (e.g., activities);

- Horizontal initiatives;

- Internal services (e.g., finance and human resources);

- Locations (e.g., headquarters and other offices housing departmental operations);

- Infrastructure (e.g., buildings and systems); and

- Outputs (e.g., services).

Responsibility

Program managers have the most knowledge about their programs, so they need to work with the CFO organization to make sure that cost objects are defined appropriately.

Tip

During discussions about the cost objects, have a copy of the department's program alignment architecture and organizational chart on hand. They can be useful when defining the limits of a cost object such as an activity that involves more than one organizational unit.

Common Cost Objects

This is a list of the common cost objects. The list is not comprehensive, and terminology varies from department to department.

- Organization

- Department

- Branch

- Directorate

- Internal services

- Management and oversight services

- Communications services

- Legal services

- Human resources management services

- Financial management services

- Information management services

- Information technology services

- Real property services

- Materiel services

- Acquisition services

- Location

- Region

- Headquarters

- Program

- Business line

- Service

- Client

- Project

- Activity

- Performance measurement unit

- Output

- Immediate outcome

- Intermediate outcome

- Strategic (final) outcome

- Process

- Activity

- Task

- Departmental process

- Interdepartmental process

Checklist for Defining Cost Objects

- Did you consult the users of the cost information when you were defining the cost objects?

- Did you review the documents that were used when defining the purpose (e.g., program alignment architecture, Report on Plans and Priorities, user fee information, audit reports, public accounts)?

- Do the cost objects fully align with the defined purpose?

- Have internal and external stakeholders confirmed the cost objects?

- Have you documented the cost objects?

- When the cost object is an activity or service, are the proposed start and end dates for the activity or service reflected in the purpose statement?

Step 3 – Determine the cost base

Key question: Based on the purpose the cost information will serve and on the cost objects, which costs are relevant?

In this step, you identify all of the costs that are relevant to the purpose and the cost objects. Relevant costs could be in the program manager's budget (e.g., salaries and supplies) or in other managers' budgets (e.g., internal services such as finance, human resources and contracting).

The relevance of a cost depends on the purpose of the costing exercise. In other words, relevance depends on what the information will be used for. For example, the cost information will be used to determine how much costs will increase if the number of clients increases, but if the cost of services provided without charge by other government departments (OGDs) does not change, these costs would not be relevant. If, however, the information will be used to determine the government's annual cost of providing a program to the public, the cost of services provided without charge by OGDs could be relevant.

Consultation is essential to make sure that you have identified all the relevant costs and that you have used the most appropriate sources of data as the cost base. The types of data that could be used as a cost base include current-year expenditures, historical expenditures, budgets, multi-year average expenditures, estimates, forecasts, or standard costs. Ideally, the purpose statement will already specify the sources. Each source must be chosen objectively, and the rationale for the choice must be documented if it is not already explained in the purpose statement.

Responsibilities

CFO organization, program, and internal services staff share responsibility for determining the cost base. You may also need to consult other stakeholders, particularly in the case of joint and horizontal initiatives.

Program managers, play an important role in any costing exercise because their knowledge of the program is essential.

Tip

To ensure efficient consultations during a costing exercise, consider establishing a standing working group that includes representatives from all internal services areas, on the understanding that the group will be convened at the request of the chief financial officer.

| $ | Data Source table 1 note 1 | Assumptions | |

|---|---|---|---|

Table 1 Notes

| |||

| Program costs | |||

Salary | |||

Non-salary | |||

Capital table 1 note 2 | |||

| Internal services costs | |||

Management and oversight | |||

Communications | |||

Legal | |||

Human resources management | |||

Financial management | |||

Information management | |||

Information technology | |||

Real property | |||

Materiel | |||

Acquisition | |||

| Centrally managed costs table 1 note 3 | |||

| Services provided without charge by other departments | |||

| Other relevant costs table 1 note 4 | |||

| Total | |||

For any given cost purpose, you should develop supporting spreadsheets to capture and calculate the relevant cost information.

Cost Base Checklist

- What data is being used and why?

- Expenditure data: Does your department's existing financial coding allow you to extract the expenditure data that is relevant? If so, did you use a single field or a combination of fields in the coding block to extract the data? If not, how will you obtain the necessary information?

- Standard costs: How were they developed and have they been updated within the last two years? If not, why not? Does management approve standard costs?

- Estimated and forecasted costs: Have you documented the estimating or forecasting technique and your assumptions? Did senior management and other relevant stakeholders validate your assumptions?

- Did you consult with the program managers and the internal services managers? Have you considered all departmental operating costs, including the relevant internal services costs?

- Have you considered all costs that are charged to statutory votes or centrally managed funds such as employee benefits?

- Have you considered amortization costs?

- If you are costing a joint or horizontal initiative, did you consult with partner departments? Did you take their costs into consideration? If not, why not?

- If you are costing a service that is provided under a revolving fund, did you include interest on the drawdown as a cost?

- Did the end-user of the cost information review and endorse the cost base?

- Have you documented all aspects of the cost base?

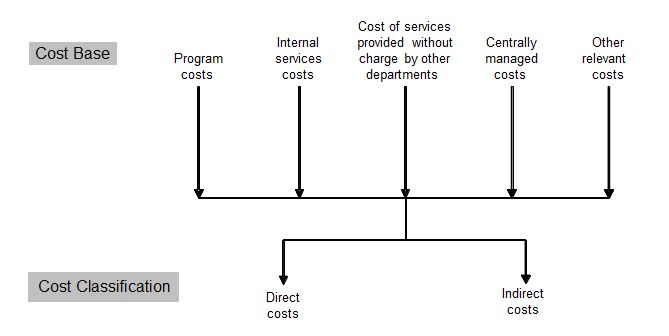

Step 4 – Classify the costs

Key questions: What types of costs are in the cost base?

Once you have determined the relevant costs, you have to classify them as either direct costs or indirect costs, based on how they relate to a cost object.

Costs are considered direct when they are incurred solely to support the cost object. For example, if the cost object is an activity, the salaries of employees who work full time on carrying out that activity are classified as direct costs.

Costs are considered indirect when they are incurred to support more than one cost object, not solely the object that is being costed. For example, the deputy head has a role in managing all activities of the department; the cost of the deputy head's office is therefore an indirect cost.

The figure below illustrates the concept of cost classification.

Responsibilities

The responsibility for classifying costs rests primarily with the department's CFO organization, with assistance from program and internal services managers.

Tip

A good way to obtain information to support cost classification is through the working group suggested in the Step 3 tip.

Cost Classification Template

- Purpose:

- Object:

- Assumptions:

| Direct Cost | Indirect Cost | Total Cost | |

|---|---|---|---|

| Program costs | |||

Salary | |||

Non-salary | |||

Capital | |||

| Internal services costs | |||

Management and oversight | |||

Communications | |||

Legal | |||

Human resources management | |||

Financial management | |||

Information management | |||

Information technology | |||

Real property | |||

Materiel | |||

Acquisition | |||

| Centrally managed costs | |||

| Services provided without charge by other departments | |||

| Other relevant costs | |||

| Total |

Cost Classification Checklist

- Have you classified all relevant costs as either direct or indirect?

- When classifying costs, did you consult the managers who are responsible for them? If not, why not?

- Did you use financial systems data to help you classify costs or confirm classifications? If not, why not?

- Have stakeholders confirmed your classification of the costs? If not, why not?

- Have you documented your cost classification process, including any assumptions you made?

Step 5 – Attribute costs to the cost objects

Key questions: What are the best ways to attribute costs to the cost objects?

Attributing costs is the process of identifying the appropriate amount of each relevant cost to include when determining the cost of an object such as a service.

The way you attribute costs varies based on the purpose. For example, if the purpose is to calculate the full cost of a government program outcome, you need to attribute a portion of internal services program costs to the outcome, in addition to the direct costs of the program that produces the outcome.

The way you attribute costs also varies based on how you classified the costs in Step 4—as direct costs or indirect costs.

Direct costs

In the case of a direct cost, attribute the full amount of it to the cost object. For example, if the cost object is a particular service delivered to Canadians, the salaries of employees who deliver that service are a direct cost of the service, so you would attribute the full amount of those salaries to the cost object.

Indirect costs

In the case of an indirect cost, attribute a portion of it to the cost object using a general basis of attribution. For example, you could use the percentage of the total departmental budget that is allocated to a unit as a basis for attributing indirect costs to the services provided by that unit.

The costs of internal services (e.g., legal services) are normally indirect costs. However, consult with the internal service managers to determine whether any of their services are provided solely to support the cost object and could therefore be attributed directly. For example, if the cost object is a particular service delivered to Canadians and a situation arises in the delivery of the service that ultimately results in a court case, you would attribute the costs of the legal services associated with the case directly to that service. Whenever possible, identify costs that are incurred solely to support the cost object and attribute them directly because it will make the resulting information more precise.

Cost pools

When you are doing attributions, one efficient approach is to use cost pools—groupings of homogeneous or like costs. Costs are considered like each other when they vary for similar reasons and at similar rates relative to the cost object. If you determine that certain costs are homogeneous, you could group them together as a cost pool and attribute them in the same way. For example, if you determine that human resources, security, and facilities management costs are like costs, you could attribute them as a pool. Cost pools are particularly useful when attributing significant numbers of low-dollar amounts.

Result

At the end of Step 5, you will have created a document that describes the way you attributed each cost (i.e., using direct or general attributions). It also describes any cost pools you have created and the way you attributed each one.

Responsibility

The CFO organization is responsible for determining the most appropriate approach to attribute costs in consultation with program, and internal services managers.

Program and internal service managers have the most knowledge of programs and what drives costs, so they are in the best position to know whether an attribution is reasonable.

Tips

Consult the internal services and program areas because their knowledge of the business can help you determine the most appropriate ways to attribute costs.

| Direct Costs | Indirect Costs | |||

|---|---|---|---|---|

| Attributed directly $ | Attributed based on a causal relationship $ | Attributed through a cost pool table 3 note 1 $ | Total amount attributed $ | |

Table 3 Notes

| ||||

| Program costs | ||||

Salary | ||||

Non-salary | ||||

Capital | ||||

| Internal services costs | ||||

Management and oversight | ||||

Communications | ||||

Legal | ||||

Human resources management | ||||

Financial management | ||||

Information management | ||||

Information technology | ||||

Real property | ||||

Materiel | ||||

Acquisition | ||||

| Centrally managed costs | ||||

| Services provided without charge by other departments | ||||

| Other relevant costs | ||||

Cost Attribution Checklist

- Have you attributed all of the direct and indirect program costs to each cost object?

- Did you identify costs that can be attributed directly to the cost objects in consultation with the program and internal services managers? If so, did you attribute them to the cost objects and exclude them from the costs to be attributed using another basis of attribution?

- For the remaining costs, did you consult the program and internal services managers to determine the extent to which there is a causal relationship between the costs and the cost object?

- For indirect costs that have no causal relationship with the cost object, did you attribute them using a reasonable basis, such as the number of FTEs, salary budget, or operating budget?

- Did you check whether some or all of the costs were homogeneous and could be pooled before you attributed them to the cost objects?

- In deciding on an attribution methodology, did you take into account the time, resources and level of precision required against the benefits to be derived from the information to ensure that there was a balance?

- Have you documented your cost attribution process, assumptions and data sources?

Step 6 – Validate and confirm the results

Key question: Is the information you have compiled complete?

This is when you review the calculations with the appropriate managers.

Verify the calculations; make sure that the assumptions, methodologies, reconciliations and documentation are complete, accurate and reasonable; and confirm that the results meet the purpose defined in Step 1.

Once the results are deemed mathematically sound, the department should confirm with the end-user that the results meet the needs, as defined in Step 1.

Responsibilities

Responsibility for validating the data sources, assumptions, methodology and calculations rests with the CFO organization.

Responsibility for confirming that the costing information satisfies the purpose identified in Step 1 rests with both the CFO organization and program management. In the case of horizontal or joint initiatives, other stakeholders may also have some responsibility for confirming that the results meet the purpose.

In complex or highly sensitive costing exercises, the CFO organization or senior management may choose to contract a qualified, neutral third party to validate the results of the exercise.

Tips

To help make the validation and confirmation process run smoothly, carry out the recommended consultations in the preceding steps.

To enhance the credibility of a costing exercise, document all assumptions, data sources and methodologies clearly. Sound documentation helps the CFO organization answer questions from decision makers and provides a valuable point of reference for future costing exercises.

Validation and Confirmation Checklist

- Review the calculations.

- Review the customized spreadsheets and the costing software and other methods you used.

- Make sure that all the headings and data (cost objects, cost base, cost pools, and related volumes) were accurately entered into the spreadsheet or software program.

- Have you included footnotes where needed?

- Are the formulas correct?

- Have you performed all the relevant calculations?

- Did you review the first five steps to ensure that they were done properly?

- Did you ensure that the results are reasonable by comparing them with the financial reports for the time period covered by the costing exercise?

- Have you collected all the necessary financial information from the appropriate sources?

- Have you checked the mathematical accuracy of your calculations?

- Have you collected the appropriate non-financial information from the appropriate sources? Have you described those data and their sources?

- Have you documented all consultations with stakeholders (internal and external) and senior management and the confirmation that the results of the costing exercise respond to the purpose statement?

Step 7– Get sign-off from the appropriate authorities

Departments are expected to have an internal sign-off process for all costing exercises to ensure adequate consultation, quality assurance, internal control, and accountability. The sign-off process should involve the CFO organization, the end-user of the cost information, and all other significant stakeholders.

When internal sign-off on a costing exercise is needed for a memorandum to Cabinet or for a Treasury Board submission, the CFO must complete the attestation letter described in the Guideline on Chief Financial Officer Attestation for Cabinet Submissions . Section 4.1 of that guideline describes the six assertions that CFOs must consider before attesting to a submission. Two of the assertions are relevant to cost estimates. For Assertion 1, the CFO must assess the reasonableness of assumptions that were used in developing the cost estimate. For Assertion 2, the CFO must ensure that risks have been assessed and that the cost estimate was adjusted appropriately. The subjects of risk, sensitivity analysis and contingency are covered in the Guideline on Cost Estimation for Capital Asset Acquisitions .

Responsibility

The CFO is responsible for confirming the quality, completeness and reasonableness of the cost information that was prepared.

Tip

Use the templates and checklists in this toolkit to help make costing exercises transparent, to support accountability, and to help make sure that the resulting cost information is of a high quality and is accurate.

CFO Sign-off Template

This template indicates the minimum requirement for an internal CFO sign-off.

| Yes/No (If no, please explain.) | |

|---|---|

| 1. Adequate consultations took place to clearly define the purpose of the cost information. | |

| 2. Adequate consultations took place to ensure that all relevant costs were captured. | |

| 3. Internal sign-offs have been completed by all required stakeholders. | |

| 4. The methodologies and data sources used, and the assumptions made are documented. |

Summary of the seven steps

| Step | Organization Responsible | Results |

|---|---|---|

| 1. Determine the purpose of the costing exercise | Management, in consultation with the department's CFO organization | A clearly defined purpose for which the information is needed; for instance, the information may be intended to support a specific management decision Timeframe and level of detail needed to support the defined purpose |

| 2. Define the cost objects | Program management and the department's CFO organization | Definition of the cost objects needed to support the purpose and the level of detail required Underlying assumptions—document these as they emerge |

| 3. Determine the cost base | The department's CFO organization, in consultation with program and internal services management and other stakeholders, as required | Determine whether the cost base will use budgets, actuals, forecasts, or a combination, as appropriate; document the sources Program costs and internal services costs Capital costs (e.g., amortization) Cost of inventories used, if material Consolidated Revenue Fund lending rate (for revolving funds) Costs of services provided by other government departments |

| 4. Classify the costs | The CFO organization, in consultation with program and internal services management and other stakeholders, as required | Segregate relevant costs in the cost base into either direct or indirect costs |

| 5. Attribute costs to the cost objects | The CFO organization, in consultation with internal services and program management and other stakeholders, as required | To the extent possible and affordable, select a basis for attribution that is causal (i.e., there is a cause-and-effect) Cost pools—pool like costs into cost pools |

| 6. Validate and confirm the results of the costing exercise | The CFO organization validates and confirms the results, in consultation with program and internal services management and other stakeholders, as required. | Validated calculations and assumptions Confirmation that costing information satisfies the cost purpose defined in Step 1 |

| 7. Get sign-off on the results | CFO and other internal stakeholders | Internal sign-off of all other costing exercises CFO attestation of cost information in Treasury Board submissions and memoranda to Cabinet |

Application of the seven steps to costing

The following is an example of how to apply the seven-step approach.

Background: A department that has service centres across the country has established that demand in a particular region is sufficient to warrant setting up a new service centre. The deputy minister (DM) has asked how much it will cost.

Step 1 – Determine the purpose of the costing exercise

- The purpose of the exercise is to determine the cost of opening a new regional service centre.

Step 2 – Define the cost objects

- The cost object is the new service centre.

Step 3 – Determine the cost base

- Financial officers from the CFO organization consult with the program manager and with managers from the internal services branch about the start-up and ongoing needs of the new service centre.

- They determine that the following costs are relevant to the cost object:

- Salaries and salary-related costs, including annual training for on-site staff;

- Equipment and supplies used by on-site staff (e.g., computers and office supplies);

- Accommodation costs (e.g., rental fees for space);

- The incremental costs to headquarters and to regional program management of providing direction and guidance to staff at the new centre and of monitoring their performance; and

- The incremental internal services costs of supporting the new service centre.

Step 4 – Classify the costs

- Direct costs: The costs directly related to setting up the new service centre (e.g., the salaries of the people that will staff the centre)

- Indirect costs: All costs not directly related to setting up the service centre (e.g., relevant program management and internal service costs that will be incurred at headquarters)

Step 5 – Attribute the costs to the cost objects

- The department already has a number of service centres, and they already have a methodology for attributing costs to a service centre. In order to be consistent and to have comparable information, the program manager and the CFO organization agreed to use the same attribution methodology for the new service centre.

Step 6 – Validate and confirm the results

The CFO organization, in consultation with internal services, program management and other stakeholders, does the following:

- Summarizes all information at the level of detail required and performs reconciliations with source data;

- Completes the necessary calculations and reviews them for accuracy;

- Reviews the results, assumptions, and methodologies to ensure they are reasonable; and

- Confirms with the DM's office that the cost information meets the DM's needs.

Step 7 – Get sign-off from the appropriate authorities

Get sign-off at the appropriate levels to indicate that the department's internal procedures, checklists and templates were used.

Appendix A - Glossary

This glossary defines terms that are commonly used when producing and/or using cost information in the federal government.

- Activity (activité)

- An operation or work process that uses inputs to produces outputs (e.g., activities such as training, research, construction, negotiation or investigation).

- Amortization (amortissement)

- The attribution of the cost of a capital asset (e.g., building, motor vehicle, major equipment) over the course of its useful life in order to reflect the economic benefit received from the asset each month or each year. For details on amortization, see Treasury Board Accounting Standard 3.1 - Capital Assets .

- Capital asset (immobilisation)

-

A tangible asset that is purchased, constructed, developed or otherwise acquired and that:

- Is held for use in the production or supply of goods, in the delivery of services or to produce program outputs;

- Has a useful life extending beyond one fiscal year and is intended to be used on a continuing basis; and

- Is not intended for resale in the ordinary course of operations.

- Cost (coût)

- The value of the resources (human, physical or financial) consumed by a program, activity or service. Cost can include both the direct resources consumed by the object and an attribution of support services that are consumed by the cost object.

- Cost base (base de coûts)

- All costs that are relevant to the purpose that will be served by the cost information and to the object that is being costed.

- Cost behaviour (variation des coûts)

- The way that costs change in response to different variables. For example, mailing costs will change with the number of mailings, but the cost of mailroom staff might stay the same even if there is a significant change in the volume of mailings.

- Costing (établissement des coûts)

- The process of determining the cost of a something such as producing a product, or delivering a service.

- Cost object (objet de coût)

- Something to which costs are attributed. Common examples are an activity, a program, a product, a service, a client, an organization or an outcome.

- Cost of financing (coût du financement)

- The cost of the interest that is charged to revolving funds on the amount of drawdown that has been used.

- Cost pool (regroupement des coûts)

- A grouping of like costs. Costs are considered like when they vary for similar reasons and at similar rates in relation to the cost object.

- Direct costs (coûts directs)

- Costs that are incurred as a direct result of the production of a good or the provision of a service. Direct costs are incurred to support a single cost object. Direct costs normally include the salaries of the people who deliver the program; operating costs such as office supplies, travel, and professional services; and capital acquisitions, to the extent that they directly contribute to the production of a good or the provision of a service.

- Employee benefits (avantages sociaux)

- Benefits that are covered by employment agreements and for which the employer pays some of the cost, for example, superannuation, Canada Pension Plan, Quebec Pension Plan, and unemployment insurance.

- Incremental cost (coûts différentiel)

- The increase or decrease in costs that results from a change in the cost object such as a change in the cost of a service when the level of service is increased. (Compare with "marginal cost.")

- Indirect costs (coûts indirects)

- Costs that are incurred in connection with producing a number of goods or providing a number of services. Indirect costs are incurred to support more than one cost object. For example, internal services costs are incurred to support all programs in a department, not just one; therefore, they are indirect costs when determining the cost of a program.

- Internal services (Services internes)

- Groups of related activities and resources that are administered to support the needs of programs and other corporate obligations of an organization. Internal services include only those activities and resources that apply across an organization, and not those provided to a specific program. The groups of activities are: Management and Oversight Services; Communications Services; Legal Services; Human Resources Management Services; Financial Management Services; Information Management Services; Information Technology Services; Real Property Services; Materiel Services; and Acquisition Services.

- Marginal cost (coût marginal)

- The additional cost of producing one more item of a product. Although "marginal cost" is sometimes used interchangeably with "incremental cost," "incremental cost" generally has a broader meaning because, as well as including changes in costs resulting from changes in volume, it includes changes in costs that result from other factors, such as a new task or service, and a change to any portion of an operation.This Guide uses "incremental costs."

- Materiality (importance relative)

- The significance of financial information to decision makers. An item of information, or an aggregate of items, is material if it is probable that its omission or misstatement would influence or change a decision. (For details on materiality, see Treasury Board Accounting Standard 2.2 - Materiality .)

- Program support costs (coûts de soutien au programme)

- The costs of a program incurred in the performance of work that is not directly involved in service delivery but that support service delivery activities. Program support costs include the cost of supervisory, administrative, management and policy functions in a program branch, at headquarters or in the regions. Program support costs are separate and distinct from internal services costs.

- Standard cost (coût standard)

- The projected cost of an activity, operation, process or unit of product assuming normal operations. Standard costs are generally calculated on a per-unit basis. Standard costs should be reviewed against actual costs at least every two years to ensure that they are still reasonable.

- Unit cost (coût unitaire)

- The cost of a unit of a product or service, calculated by dividing the total costs of a given period or of a given operation by the number of units produced in that period or operation.

Appendix B - References

Legislation

Policy instruments

- Policy on Interdepartmental Charging and Transfers Between Appropriations

- Policy on Special Revenue Spending Authorities

- Policy on Management, Resources and Results Structure

- Policy on Service Standards for External Fees

- Policy on Transfer Payments

- Treasury Board Accounting Standard 3.1–Capital Assets

- Treasury Board Accounting Standard 3.1.1–Software

- Financial Information Strategy Accounting Manual

- Consolidated Revenue Fund Monthly Lending Rates for Periods of One Year and Over

- Canadian Cost-Benefit Analysis Guide

- Guide to Establishing the Level of a Cost-Based User Fee or Regulatory Charge

Appendix C - Useful sources of information on costing

The purpose of this appendix is to provide access to sources of information within the Government of Canada that could be useful in planning, producing and assessing cost information.

1. General guidance on costing

Lessons Learned on Costing Practices

2. Specific guidance related to costing

Guideline on Chief Financial Officer Attestation for Cabinet Submissions

Cost estimates in Cabinet submissions are subject to Chief Financial Officer (CFO) attestation. Section 4.1 of the Guideline on Chief Financial Officer Attestation for Cabinet Submissions describes the six assertions that CFOs must consider before attesting to a submission. Two of the assertions are relevant to cost estimates. For Assertion 1, the CFO must assess the reasonableness of assumptions that were used in developing the cost estimate. For Assertion 2, the CFO must ensure that risks have been assessed and that the cost estimate was adjusted appropriately.

Guide on Internal Services Expenditures: Recording, Reporting and AttributingPubliservice Only

The purpose of the Guide on Internal Services Expenditures: Recording, Reporting and Attributing is to establish a basis for greater consistency in recording and reporting internal services expenditures across government. Internal service expenditures are recorded separately from other program expenditures.

Guideline on Cost Estimation for Capital Asset Acquisitions

The purpose of the Guideline on Cost Estimation for Capital Asset Acquisitions is to provide guidance on how to prepare, present and use cost estimates for decision making. It also provides guidance on what cost information is required when making a decision on different options (e.g., purchase, lease or public private partnership).

2014 Guidance for the Preparation of TB Submissions

The 2014 Guidance for the Preparation of TB Submissions covers all aspects of preparing a Treasury Board submission. Most submissions contain cost information, which would be included in the following sections of the submission:

- Cost, Funding Requirements and Source of Funds;

- Costing, Due Diligence and Validation; and

- Financial Appendices.

These are described in the section Detailed Guidance for Writers.

© His Majesty the King in right of Canada, represented by the President of the Treasury Board, 2017,

ISBN: 978-0-660-09821-0