Archived [2022-05-13] - Guidelines on Contractual Arrangements

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

1. About these Guidelines

1.1 These Guidelines on Contractual Arrangements provide advice and interpretation to support the current Treasury Board Contracting Policy and its provisions pertaining to contractual arrangements. Its purpose is to provide guidance to managers and functional specialists on the defining characteristics and policy principles that support the use of contractual arrangements for the acquisition of goods, services and construction services. The Treasury Board of Canada Secretariat (TBS) has developed this guidance in consultation with other departments and agencies.

2. Application

2.1 These guidelines apply only to contractual arrangements as defined in the Contracting Policy. “Contractual arrangement” is not a legal term but a policy term. This includes arrangements with various public sector organizations (including other levels of government and international partners) that involve the acquisition of goods, services or construction services. They do not apply to arrangements (such as service agreements) between federal departments, transfer payment programs, and treaties or arrangements that do not include a procurement of some kind. Further, as these are guidelines, they are not considered mandatory, but rather impart advice and TBS interpretations in order to support departments’ implementation of the Treasury Board Contracting Policy.

3. Introduction

3.1 Ministers may use a variety of instruments to carry out the business of government with an equally diverse range of stakeholders. This includes the private sector, non-profit organizations, other levels of government, and international (state and non-state) actors. In many instances, a minister’s use of a particular instrument will fall within well-delineated legal and policy parameters, such as a contract or transfer payment, which have clearly outlined requirements for Cabinet, Treasury Board or other approval.

However, in instances where working with other public sector organizations will provide best value, a contract may be inappropriate. Some type of administratively binding although not legally enforceable agreement, such as a contractual arrangement, may be the only alternative. These guidelines should help departments ask the right questions when setting up contractual arrangements.

4. Key Characteristics

Key criteria to determine the right instrument:

- What are you paying for?

- Who directly benefits and who will use it?

- Who are you paying?

- Who is making the payment?

- What is the source of funds?

- Do you have the requisite authority to engage in the activity?

4.1 The following guidance offers some considerations when establishing contractual arrangements.

4.1.1 Where possible, and especially when using private sector resources, the best option is to protect the Crown by using a contract, which must follow the requirements of the Government Contracts Regulations (GCRs) and the Contracting Policy.

However, there is a spectrum of other instruments available. Determining the appropriate type of instrument to use requires an understanding of the legal characteristics of each party, the applicable laws, relevant policies, and the substance and nature of the transaction. All are covered by the Financial Administration Act (FAA), and all have different obligations in legislation and policy. It is important to find the most effective tool to derive the best value for the Crown and to set out clear expectations and payment provisions for both sides.

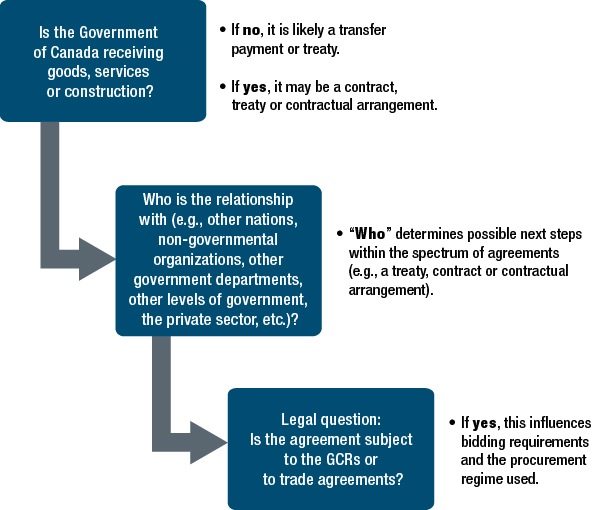

Figure 1: Key considerations for contractual arrangements

Text version: Key considerations for contractual arrangements

4.1.2 Generally speaking, the GCRs do not apply to contractual arrangements, and therefore there are no requirements to solicit bids. In addition, trade agreements generally do not apply to contractual arrangements. For example, the Agreement on Internal Trade does not apply to agreements between governments or “public bodies,” so those agreements have been specifically carved out. International trade agreements do not apply to contractual arrangements that have no legal recourse mechanism, as they are not considered contracts.

There can be exceptions, however. When in doubt, departments should consult their legal services unit to determine whether the GCRs or trade agreements apply to a particular arrangement.

4.1.3 Contractual arrangements are subject to the entry limits outlined in Part I of Appendix C, “Treasury Board Contracts Directive” of the Contracting Policy. It is not only contracts that are subject to such limits; contractual arrangements are as well, as stated in the preamble to the Contracts Directive:

Part I: Basic Contracting Limits

“1. A contracting authority, as defined in the Government Contracts Regulations and as specified in Column I in Schedules 1, 2, or 3, as well as in the text of Schedule 5, may enter into a contract or contractual arrangement without the approval of the Treasury Board, if the amount payable, which includes all applicable taxes (including GST or HST), does not exceed the limit set out in Columns II, IV and VI Schedules 1, 2, or 3 and in the text of Schedule 5.”

Typically, bids are not sought when creating contractual arrangements; therefore, the arrangements are subject to the non-competitive limits listed in the Contracts Directive (Appendix C of the Contracting Policy). Any contractual arrangements that exceed the limits in the Contracts Directive require Treasury Board approval.

4.1.4 Contractual arrangements may be legally binding or not, depending on the substance of the arrangement between the participating entities. Whatever the intention, arrangements can be interpreted by a court as being legally binding if they include some of the elements characteristically found in a legally binding contract, beyond provisions to share costs, risks and benefits, such as:

- Jurisdictions for dispute resolutions;

- Ownership of intellectual property and work products;

- Limitation of liability provisions;

- Offer and acceptance;

- Intention and capacity to create legal relations; and

- Consent of both parties.

Consultations with legal services can help clarify questions about whether the arrangement may be legally binding or not.

4.1.5 Contractual arrangements can have various names. “Contractual arrangement” is a generic term, often referred to by other names, including, but not limited to:

- Memorandum of Understanding;

- Memorandum of Agreement;

- Comprehensive Research and Development Agreement;

- Exchange of Service Agreement;

- Letter of Agreement; and

- Collaborative Arrangement.

Regardless of the name of an arrangement, the elements contained therein will dictate the effects or consequences that the arrangement has on the parties, for example, that a good, service or construction service is being provided to the department. The key questions are whether the department will acquire goods or services through this instrument, and who the participants are.

4.1.6 When the type of the payment is determined, it is a best practice for departments to use existing internal processes and controls governing the payment instrument (e.g., contract or contractual arrangement, contribution agreement), rather than creating separate processes, to ensure that due diligence is completed.

4.1.7 Prudence, probity and best value are important considerations for contractual arrangements. A key principle of the Contracting Policy is that government acquires goods, services and construction services in a manner that enhances access, competition and fairness, and results in best value or, if appropriate, an optimal balance of overall benefits to the Crown and to Canadians.

According to subsection 4.1.8 of the Contracting Policy:

“Public servants who have been delegated authority to negotiate and conclude contractual arrangements on behalf of the Crown must exercise this authority with prudence and probity so that the contracting authority (the minister) is acting and is seen to be acting within the letter and the spirit of the Government Contracts Regulations, the Treasury Board Contracts Directive and the government’s procurement policies, the North American Free Trade Agreement, the World Trade Organization Agreement on Government Procurement, and the Agreement on Internal Trade.”

In the case of contractual arrangements, they should respect core contracting policy principles by seeking value for money, being conducted transparently, and being able to withstand public scrutiny.

Examples of prudence and probity for contractual arrangements

- Maintaining clear documentation of procurement decision making, similar to what would be expected of a standard commercial contract.

- Providing justification for selecting the source and method of supply (e.g., why a contractual arrangement rather than a contract or transfer payment?), including a well-documented business analysis for any sourcing strategy.

- Maintaining evidence of value for money of the selected approach as compared with other sourcing strategies.

- Consulting legal, financial and procurement expertise within your department early and often.

- Ensuring that the appropriate contracting authority is signing the arrangement, and that other government departments have been consulted substantively and in a timely manner. Depending on the activity involved, departments may need to consult the Privy Council Office, Industry Canada, Aboriginal Affairs and Northern Development Canada, and Public Works and Government Services Canada, to name a few.

- Using existing procurement processes and controls to manage contractual arrangements.

5. Other Considerations When Using Contractual Arrangements

5.1 Treasury Board Approval

After consulting with internal departmental legal and procurement resources, departments should consult with TBS before entering into a contractual arrangement whose total value (including any sub-agreements) is valued above contract entry limits. As noted above, since bids are not normally solicited when a contractual arrangement is used, non-competitive entry limits apply.

Although policies related to limitation of liability or intellectual property do not generally apply to contractual arrangements, it is important to be mindful of their principles when signing a contractual arrangement, seek any exceptions that may be appropriate, and document the file accordingly.

Project and policy approvals may also be required prior to entering into a contractual arrangement. Early consultation with project management, legal, financial and procurement experts is a best practice.

5.2 Arrangements With International Partners

Although the definition of contractual arrangements is an agreement between contracting authorities and “entities of the Crown” (see the definition of “contractual arrangement” in Appendix A), this has been further interpreted to include agreements with other countries, public entities, non-governmental organizations, or supranational organizations (e.g., the United Nations), where appropriate. Careful analysis is needed to ensure that these arrangements are not treaties, transfer payments or contracts. Foreign Affairs, Trade and Development Canada and Public Works and Government Services should be consulted as required.

5.3 Transfers

As per Section 3, “Application,” of the Contracting Policy, transfers are not covered by these guidelines. Such transfers include:

- Transfers between federal departments (as defined in Section 2 of the FAA); and

- Transfers as defined by the Policy on Transfer Payments (grants, contributions or other transfer payments, such as transfers to support programs run by other levels of government).

There are times when the federal government cooperates with other governments to carry out a project. Often, these arrangements are embodied in federal-provincial agreements, normally governed by legislation or related to the overall mandate of the federal authority. When this formal government-to-government relationship is not applicable, a contractual relationship between the federal contracting authority and the other government entity may be appropriate. When buying goods, services or construction services from other levels of government (provincial, municipal, other states, or even supranational organizations), a contractual arrangement should be used.

When working with a public sector entity outside the federal family, it is a best practice to involve departmental advisors in the areas of financial management, procurement and legal services early in the process to determine the best course of action and whether contractual arrangements are required.

Should it be a contractual arrangement?

When working with other levels of government, the following indicators can help departments determine whether a contractual arrangement is required. Generally, the more indicators there are, the more likely it is that a contractual arrangement is required. Indicators may include, but are not limited to, the following:

- The Crown receives a good, service or construction at a value commensurate with overall costs and may include title, possession, control or use of intangibles.

- The transaction is covered by the GCRs (a transaction at no cost is not likely covered) and meets the definition of goods, services or a construction contract.

- The arrangement involves the private sector in the delivery of the good, service or construction.

- The good, service or construction can be delivered by the private sector.

- The arrangement is not covered by other legislation that restricts or carves out Treasury Board authority to issue administrative policy (e.g., federal-provincial agreements, the Public Service Employment Act, treaties).

- The arrangement uses capital or operations and maintenance funding and not contribution funds (some vote wording permits exceptions).

- The planned arrangement is treated as a procurement by a trade agreement.

- The good, service or construction received is in exchange for a monetary payment and is not a gift, volunteering, transfer, trade, barter, exchange, expropriation, confiscation, spoil of war or inventory adjustment.

- The cost of the arrangement is tracked in financial systems under an economic object that is aligned with procurement.

- The arrangement is entitled or contains words typical of a procurement, e.g., “contract,” “purchase order,” “call-up,” “the contractor shall deliver,” etc.

- The arrangement is signed by a contracting authority.

- The arrangement is within the mandate of the contracting authority.

5.4 Public Works and Government Services Canada’s and Other Government Departments' Roles and Responsibilities

Departments are reminded that under Section 9 of the Department of Public Works and Government Services Act, the Minister of Public Works and Government Services has the exclusive authority to acquire goods, with only a few exceptions. Similarly, under the Defence Production Act, the Minister of Public Works and Government Services had the exclusive authority to buy or otherwise acquire defence supplies and construct defence projects.

It is a best practice to consult with legal advisors to ensure that a department has the authority to enter into a contractual arrangement for any goods, services or construction services. It is also recommended that departments consult Public Works and Government Services Canada early in any process that may involve an acquisition over $25,000 and that may be within Public Works and Government Services Canada’s purview. Public Works and Government Services Canada will also require evidence that certification of expenditure initiation under Section 32 of the FAA (e.g., a “funded” requisition, or the 9200 form) to proceed with these arrangements.

Departments should consult with colleagues in other departments early in the process of developing contractual arrangements, particularly those that may involve possible future acquisitions or other commitments. This is also important so that sufficient time can be allocated in any critical path that requires Cabinet-level approvals or navigating Public Works and Government Services Canada’s processes, as required.

5.5 Contractual Arrangements That Have Multiple Activities

Some relationships may involve other aspects beyond any procurement of goods, services or construction services. This might include personnel exchanges, research and development partnerships, sharing of data, or other technical information or various other types of collaboration. Arrangements to collaborate that have no procurement aspects in the short term may also lead to procurement relationships in the medium or long term.

A best practice in these instances is to look at how large a component the procurement aspect is (or may potentially become) as compared with the overall scope of activities. If procurement is a significant proportion of the related activity, or if it is risky or otherwise sensitive, departments should consider processing the arrangement through their usual procurement channels to ensure sufficient due diligence. These instances must be treated on a case-by-case basis. Early engagement with departments’ legal, procurement and financial expertise and with TBS can help determine the required course of action.

5.6 Financial Management and Payment Implications

Departments are encouraged to structure arrangements so that they certify that the goods or services procured have been received in accordance with Section 34 of the FAA. This includes defining expected outcomes and schedules of payment, and a description of the responsibilities of the parties. This is important, as departments cannot legally make payments on non-binding agreements unless they meet these standard obligations under Section 34.

Where neither contracting nor transfer payment models fit the planned approach, departments are encouraged to seek legal advice early on in the development of the arrangement to ensure that they have the legal authority in place to make payments. In some cases, an order-in-council may be required.

Financial management questions

It may also be useful to determine the financial management policy implications, and when it may be appropriate to use a contractual arrangement, by asking the following questions:

- Is the transaction authorized under the legal mandate of the department?

- Against which appropriation will the expenditures be charged (transfer payment or operational expenditures)?

- Can the department make recoverable expenditures under its legislative authorities?

- Is it a transfer payment or is the government receiving a good or service?

- Is there a third party, and what is the nature of the relationship and the rule that applies (contractor or recipients of a transfer payment)?

- How will requirements of Section 34 of the FAA be met?

6. References

6.1 Relevant Legislation

6.2 Treasury Board Policies

6.3 Other Policies/Guidance

7. Conclusion

7.1 Next Review Date

This document will be reviewed and updated within 12 months of its publication date. Subsequently, it will be updated every three years, or as part of any review of the Contracting Policy.

8. Enquiries and Comments

8.1 For questions on this policy instrument, please contact TBS Public Enquiries.

Appendix A: Definitions

- Contract (marché)

- An agreement between a contracting authority and a person or firm to provide a good, perform a service, construct a work or lease real property for appropriate consideration.

- Contractual arrangement (accord contractuel)

- An agreement between a contracting authority and an entity of the Crown (e.g., Crown corporations, provincial governments or municipalities) to provide a good, perform a service, construct a work or lease real property for appropriate consideration. These types of agreements are not contracts in the true sense but are still subject to certain limits or constraints imposed by the Treasury Board.

- Transfer payment (paiement de transfert)

- A monetary payment, or a transfer of goods, services or assets made, on the basis of an appropriation, to a third party, including a Crown corporation, that does not result in the acquisition by the Government of Canada of any goods, services or assets. Transfer payments are categorized as grants, contributions and other transfer payments. Transfer payments do not include investments, loans or loan guarantees.

© His Majesty the King in right of Canada, represented by the President of the Treasury Board, 2017,

ISBN: 978-0-660-09818-0