Guideline on Common Financial Management Business Process 1.1 – Manage Planning And Budgeting

Executive Summary

This guideline is part of a set of guidelines designed to assist departments See footnote [1] in implementing common financial management business processes.

This guideline presents the “should be” model for Manage Planning and Budgeting, which involves internal departmental planning and budgeting against voted authorities (for example, operating expenditure vote, capital expenditure vote, and grants and contributions vote) for the fiscal year. This guideline describes roles, responsibilities and recommended procedures in the context of the Financial Administration Act, other legislation, and Government of Canada policy instruments.

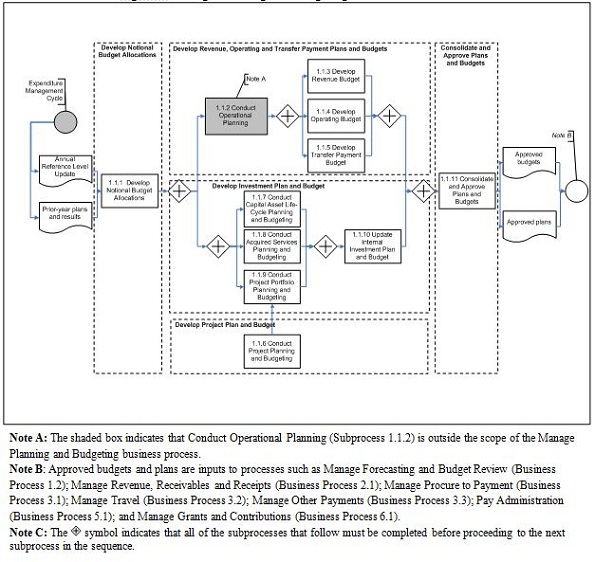

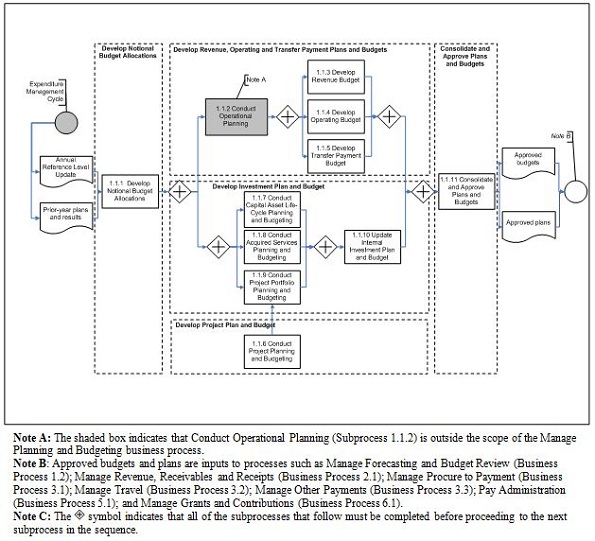

Figure 1. Manage Planning and Budgeting – Level 2 Process Flow

Text version: Figure 1. Manage Planning and Budgeting – Level 2 Process Flow

As illustrated in Figure 1, Manage Planning and Budgeting comprises 11 subprocesses (1.1.1 to 1.1.11). These are arranged in five subprocess groups, as follows.

Develop Notional Budget Allocations is the start of the Manage Planning and Budgeting business process and involves the development of notional budget allocations to responsibility centres and other planning dimensions, including authorities, objects of expenditure, program activities and projects.

Develop Revenue, Operating and Transfer Payment Plans and Budgets involves the development of operational plans and related budgets that are aligned with departmental objectives, priorities, assumptions and constraints. Depending on the structure of the department's budget, not all subprocesses or activities will apply. For example, Develop Transfer Payment Budget (Subprocess 1.1.5) applies only to departments that administer transfer payments.

Develop Project Plan and Budget involves the identification, assessment, planning and approval of projects throughout the fiscal year. These activities support the deputy head in meeting his or her responsibility for ensuring that a department-wide project management governance and oversight mechanism is in place to manage the initiation, planning, execution, control and closing of projects. See footnote [2] Although the other activities within the Manage Planning and Budgeting business process occur before the start of the fiscal year, the activities within the Develop Project Plan and Budget subprocess group may occur at any point in the year, as new projects are identified.

Develop Investment Plan and Budget involves activities to ensure that capital asset life-cycle requirements, project portfolio plans, and planned investments in acquired services are considered in the development of the departmental investment plan and budget. These activities support the requirement that effective investment planning should ensure a diligent and rational manner of resource allocation for both existing and new assets, and for acquired services. See footnote [3]

Consolidate and Approve Plans and Budgets involves the consolidation, review, challenging and approval of plans and budgets. Options to address budget pressures or to use surplus funds effectively are also reviewed and approved. Approved budgets are then communicated to responsibility centre managers.

Throughout the Manage Planning and Budgeting business process, plans and budgets are developed and rolled up at various levels within the department. For example, activities within the Develop Revenue, Operating and Transfer Payment Plans and Budgets subprocess group are typically conducted by various responsibility centre managers and rolled up by business unit, whereas activities within the Develop Investment Plan and Budget subprocess group are conducted using a more centralized approach, within an organization-wide investment management framework. Activities are often completed concurrently because the resulting budgets (revenue, operating, transfer payments, capital assets and project portfolio), pressures, surpluses and risks are interdependent across activities.

1. Date of Issue

This guideline was issued on May 15, 2013.

2. Context

This guideline is part of a set of guidelines designed to assist departments See footnote [4] in implementing common financial management business processes. This guideline supports the Policy on the Stewardship of Financial Management Systems and the Directive on the Stewardship of Financial Management Systems.

This guideline presents the “should be” model for Manage Planning and Budgeting, describing roles, responsibilities and recommended activities from a financial management perspective. Most activities are financial in nature, but some non-financial activities are included in order to provide a comprehensive process description; these activities are identified as outside the scope of Managing Planning and Budgeting. The recommended activities comply with the Financial Administration Act, other legislation, and Government of Canada policy instruments.

Recognizing that deputy heads are ultimately responsible for all aspects of financial management systems within their department, standardizing and streamlining financial management system configurations, business processes and data across government provides significant direct and indirect benefits relative to the quality of financial management in the Government of Canada. By establishing a common set of rules, standardization reduces the multitude of different systems, business processes and data that undermine the quality and cost of decision-making information. As government-wide standardization increases, efficiency, integrity and interoperability are improved. See footnote [5]

3. Introduction

3.1 Scope

This guideline defines Manage Planning and Budgeting, which begins with the Annual Reference Level Update as an input to identify the notional departmental budget and ends with the approval of annual budgets allocated to responsibility centres and other planning dimensions, including authorities, objects of expenditure, program activities and projects. This process is generally completed before the beginning of the fiscal year.

This guideline covers the following subprocess groups:

- Develop Notional Budget Allocations;

- Develop Revenue, Operating and Transfer Payment Plans and Budgets;

- Develop Project Plan and Budget;

- Develop Investment Plan and Budget; and

- Consolidate and Approve Plans and Budgets.

Some financial management activities described in this guideline are also related to internal controls. The intent is neither to provide a complete listing of controls, nor to produce a control framework; however, this model may provide useful content for the development of a department's control framework.

3.2 Structure of the Guideline

The remainder of this guideline is structured as follows. Section 4 provides an overview of the roles that carry out Manage Planning and Budgeting. Section 5 presents a detailed description of the Manage Planning and Budgeting business process, including subprocess groups, subprocesses, activities and responsible roles. Appendix A provides definitions of terminology used in the guideline, and relevant abbreviations are listed in Appendix B. Appendix C describes the methodology used in the guideline, and Appendix D elaborates on the roles and responsibilities outlined in Section 4. Finally, Appendix E provides examples of the components typically found in an operational plan.

3.3 References

The following references apply to this guideline.

3.3.1 Acts and Regulations

3.3.2 Policy Instruments

- Directive on Expenditure Initiation and Commitment Control

- Directive on the Management of Expenditures on Travel, Hospitality and Conferences

- Directive on the Stewardship of Financial Management Systems

- Guideline on Common Financial Business Process 5.1 – Pay Administration

- Policy Framework for the Management of Assets and Acquired Services

- Policy on Financial Management Governance

- Policy on Financial Resource Management, Information and Reporting

- Policy on Internal Control

- Policy on Investment Planning – Assets and Acquired Services

- Policy on Learning, Training, and Development

- Policy on Management of Information Technology

- Policy on Management of Materiel

- Policy on Management, Resources and Results Structures

- Policy on Special Revenue Spending Authorities

- Policy on the Management of Projects

- Policy on the Stewardship of Financial Management Systems

- Standard for Organizational Project Management Capacity

- Standard for Project Complexity and Risk

- Standards on Knowledge for Required Training

3.3.3 Other References

- A Guide to Preparing Treasury Board Submissions

- Financial Information Strategy Accounting Manual

- Guide on Financial Arrangements and Funding Options

- Guide to Costing

- Guide to Investment Planning – Assets and Acquired Services

- Management Accountability Framework

- Manager's Guide to Operating Budgets

- Project Complexity and Risk Assessment Tool

- The Financial Administration Act: Responding to Non-compliance – Meeting the Expectations of Canadians

4. Roles and Responsibilities

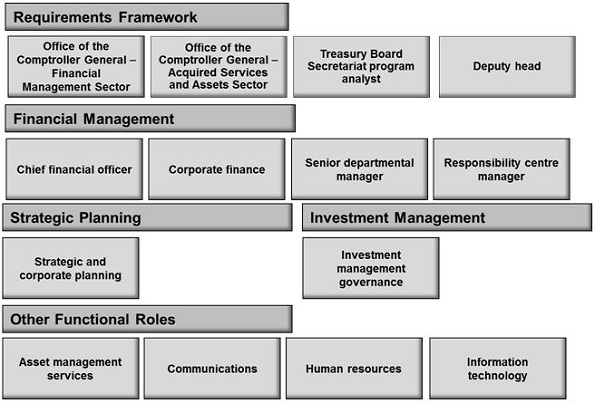

Figure 2 depicts the roles involved in the Manage Planning and Budgeting business process, grouped by stakeholder category.

Figure 2. Roles Involved in Manage Planning and Budgeting

Text version: Figure 2. Roles Involved in Manage Planning and Budgeting

In this guideline, a role is an individual or a group of individuals whose involvement in an activity is described using the Responsible, Accountable, Consulted and Informed (RACI) approach. Because of differences among departments, a role may not correspond to a specific position, title or organizational unit. The roles and responsibilities for Manage Planning and Budgeting are briefly described in Sections 4.1 to 4.5 and are explained in more detail in Appendix D.

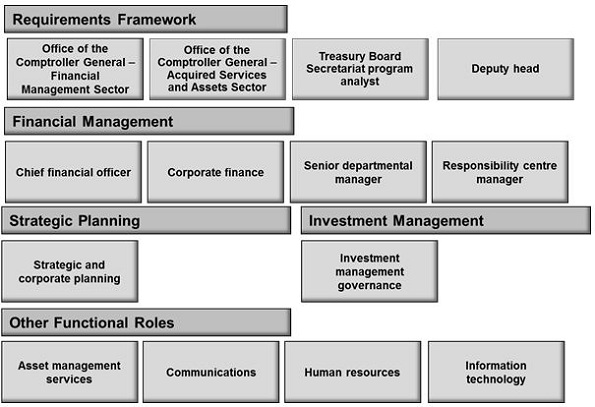

4.1 Requirements Framework

The following organizational roles act in support of legislation, such as the Financial Administration Act and the Federal Accountability Act, and define policy or processes that must be followed.

- The Office of the Comptroller General – Financial Management Sector is the policy authority for financial management.

- The Office of the Comptroller General – Acquired Services and Assets Sector is the policy authority responsible for developing, implementing, monitoring and renewing asset management, investment planning and project management-related policies, standards, tools and guides.

- The Treasury Board Secretariat program analyst is responsible for providing departments with analysis and advice on resource allocation for the effective use of resources; program design, viability and responsiveness; funding pressures and mitigation strategies; and broad government operational issues and management strategies. See footnote [6]

- The deputy head is responsible for:

- Providing departmental leadership by demonstrating financial responsibility, transparency, accountability and ethical conduct in financial and resource management, including compliance with legislation, regulations, Treasury Board policies and financial authorities; See footnote[7]

- Ensuring effective oversight of the department's financial plan, budget and related allocations of resources;

- Making decisions based on sound analysis of reliable information; and

- Ensuring the timely allocation of approved budgets, throughout the fiscal year, to all managers with financial authorities. See footnote [8]

4.2 Financial Management

The following organizational roles act in response to financial management policy and process requirements—for example, from the Office of the Comptroller General – Financial Management Sector and from the deputy head.

- The chief financial officer is responsible for:

- Supporting the deputy head in meeting his or her financial management accountabilities;

- Acting as the lead departmental executive for all aspects of financial management, program financing, financial reporting and disclosure, and for dealing with central agencies and other stakeholders;

- Leading the financial component of the departmental planning process on behalf of the deputy head, which includes assessing business risks and financial resource implications;

- Performing the challenge function on the use of public resources; and

- Providing advice to the deputy head, to mitigate financial risk to the organization. See footnote [9]

- The corporate finance role is responsible for:

- Supporting the deputy head and the chief financial officer in meeting their financial management accountabilities by developing, communicating and maintaining the departmental financial management framework;

- Providing leadership and oversight on the proper application and monitoring of financial management across the department; See footnote [10]

- Supporting departmental and business unit-level activities related to resource management, including managing resource allocation at the departmental level;

- Providing financial analysis and input to departmental planning and reporting documents, including the Report on Plans and Priorities, the Departmental Performance Report, the Annual Reference Level Update and Treasury Board submissions; and

- Providing financial management advice and guidance to responsibility centre managers.

- The senior departmental manager reports directly to the deputy head (for example, an assistant deputy minister) and is responsible for:

- Exercising his or her financial management authorities, responsibilities and accountabilities;

- Managing the organization's financial resources prudently; and

- Complying with legislation, regulations and Treasury Board policies, directives and standards. See footnote [11]

- The responsibility centre manager holds budget management responsibilities, which include:

- Exercising financial management authorities, responsibilities and accountabilities;

- Managing financial resources entrusted to him or her prudently; and

- Complying with legislation, regulations and Treasury Board policies, directives and standards.

4.3 Strategic Planning

The following organizational role acts in response to strategic and operational planning requirements.

- The strategic and corporate planning role is responsible for:

- Coordinating input to the organization's strategic, integrated and operational planning processes; and

- Supporting central agency requirements, such as those under the Policy on Management, Resources and Results Structures and the Management Accountability Framework, and Parliamentary reporting requirements, such as the Report on Plans and Priorities and the Departmental Performance Report.

4.4 Investment Management

The following organizational role provides direction and oversight related to investment, asset and project management.

- Investment management governance is responsible for governing departmental investment decisions and for supporting the deputy head in ensuring that departmental investment planning:

- Is influenced by and supports departmental strategic planning;

- Incorporates a departmental, portfolio, horizontal and government-wide perspective and takes into account strategic government-wide initiatives;

- Is aligned with the outcomes set out in the department's Management, Resources and Results Structure, and considers areas of greatest risk in achieving departmental objectives;

- Is influenced by an assessment of investment performance;

- Considers alternative and innovative options for meeting assets and service requirements, including internal and external delivery models and a range of instruments;

- Is within reference levels; and

- Takes into account the whole-of-life cost of stewardship, based on the life cycle of assets and acquired services. See footnote [12]

4.5 Other Functional Roles

The following organizational roles act in response to policy and process requirements related to the management of other functional areas.

- The asset management services role is responsible for supporting the deputy head in:

- Establishing an asset management framework that reflects an integrated approach to risk management;

- Providing relevant performance information;

- Establishing clear accountability and decision-making regimes that are consistent with organizational resources and capacity; and

- Supporting timely and informed asset management planning and budgeting decisions and the strategic outcomes of departmental programs. See footnote [13]

- The communications role is responsible for:

- Managing corporate identity, advertising, publishing, marketing, environment analysis, public opinion research, media relations, event participation and other communication activities;

- Ensuring that communications planning is integrated into the departmental business planning exercise; and

- Providing communications advice and support to responsibility centre managers.

- The human resources role is responsible for such functions as classification, staffing and labour relations, which involve:

- Executing human resources-related transactions, including classification decisions, identification of successful candidates in a staffing action, and decisions on disciplinary actions; See footnote [14] and

- Providing human resources guidance and advice to responsibility centre managers in support of planning, budgeting and day-to-day activities.

- The information technology role is responsible for supporting the deputy head in:

- Ensuring effective management of information technology within the department, including the implementation of information technology planning and spending decisions;

- Ensuring appropriate and ongoing measurement of information technology performance; and

- Integrating departmental information technology investment plans into the overall business plans of the department. See footnote [15]

5. Process Flows and Descriptions

Appendix C describes the methodology used in this Section.

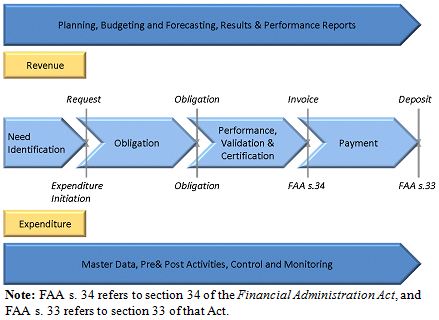

5.1 Overview of Planning and Budgeting

Planning and budgeting are key components of effective financial resource management. Effective financial resource management supports effective and efficient use and stewardship of public resources and involves planning, budgeting, monitoring and reporting. See footnote [16]

The Manage Planning and Budgeting business process focuses on internal departmental planning and budgeting, and uses inputs resulting from central agency planning and budgeting subprocesses that form part of the Expenditure Management System of the Government of Canada.

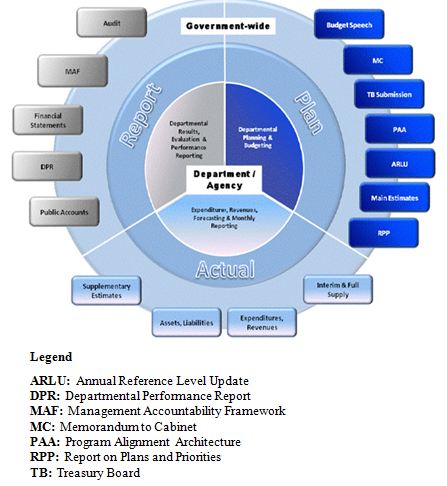

5.1.1 The Expenditure Management System

The Expenditure Management System of the Government of Canada is the framework for developing and implementing the government's spending plans and encompasses a number of elements and activities, including planning and evaluation, that guide decisions on the allocation of resources. See footnote [17] Through its various components, the Expenditure Management System promotes an ongoing review of programs and spending, with a focus on performance. Figure 3 provides a summary of the expenditure management cycle.

In Figure 3, the boxes to the right of the “Plan” component represent the mechanisms through which initial funding is approved and appropriated to departments. The outputs of the elements of planning, including Treasury Board submissions and Annual Reference Level Updates, are used as inputs for internal departmental planning and budgeting.

5.1.2 Manage Planning and Budgeting – Common Financial Management Business Process 1.1

Departments are appropriated their annual funding through voted authorities and receive details on their statutory authorities according to the outputs of the planning component of the expenditure management cycle. The Manage Planning and Budgeting business process is the set of integrated activities that the organization completes each fiscal year in order to develop detailed internal departmental plans and budgets against voted authorities (for example, operating expenditure vote, capital expenditure vote, and grants and contributions vote). These activities have both financial and non-financial components.

The Manage Planning and Budgeting business process supports the deputy head's responsibility for ensuring effective oversight of the department's financial plan, budget and related allocations of its resources and for making decisions based on sound analysis of reliable information. This oversight ensures that:

- Financial resources are aligned with the mandate and priorities of the department and the government;

- Key assumptions, including workload and cost estimates, are reliable;

- Significant financial risks to effective planning and budgeting are identified and risk mitigation strategies are reasonable; and

- Monitoring and reporting on the use and performance of financial resources are effective. See footnote [18]

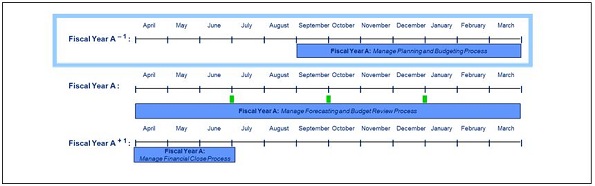

The Manage Planning and Budgeting business process is generally completed in the year preceding the fiscal year being planned, as represented by “Fiscal Year A–1,” as shown in Figure 4.

Figure 4. Sample Timeline for the Manage Planning and Budgeting Business Process

Text version: Figure 4. Sample Timeline for the Manage Planning and Budgeting Business Process

As illustrated in Figure 5, the Manage Planning and Budgeting Level 2 business process comprises 11 subprocesses (1.1.1 to 1.1.11). These are arranged in five subprocess groups: Develop Notional Budget Allocations; Develop Revenue, Operating and Transfer Payment Plans and Budgets; Develop Project Plan and Budget; Develop Investment Plan and Budget; and Consolidate and Approve Plans and Budgets.

Figure 5. Manage Planning and Budgeting – Level 2 Process Flow

Text version: Figure 5. Manage Planning and Budgeting – Level 2 Process Flow

The subprocesses within each subprocess group and the roles and responsibilities relevant to each subprocess are summarized below.

Develop Notional Budget Allocations

- Develop Notional Budget Allocations (Subprocess 1.1.1): The planning and budgeting process begins with the Annual Reference Level Update as an input to the development of notional budget allocations to responsibility centres and other planning dimensions, including authorities, objects of expenditure, program activities and projects. Notional budget allocations are envelopes within which responsibility centre managers develop their detailed annual budgets. In addition, an integrated planning package, which provides planning instructions and timelines and which may provide high-level planning priorities assumptions and constraints, is prepared for managers with planning and budgeting responsibilities.

Develop Revenue, Operating and Transfer Payment Plans and Budgets

- Conduct Operational Planning (Subprocess 1.1.2): Based on the notional budget allocations and the integrated planning package, operational plans are developed at the business-unit level. These plans outline the activities that business units will undertake to help the department achieve its strategic objectives. Operational plans include key performance indicators and may include requirements for human resources, information management and information technology, office accommodations and communications. Note that operational planning is largely a non-financial function and therefore is outside the scope of the Manage Planning and Budgeting business process.

- Develop Revenue Budget (Subprocess 1.1.3): The revenue budget is developed to validate the amount of expected revenue forecast in the Annual Reference Level Update. The budget outlines the expected revenue by program or source and by responsibility centre for the fiscal year, taking into account assumptions, constraints, historical trends and current information. When revenue is respendable, the budget will be an input to Develop Operating Budget (Subprocess 1.1.4).

- Develop Operating Budget (Subprocess 1.1.4): Based on operational plans and resource requirements, the operating budget is developed. The operating budget is divided into salary and non-salary components.

- Develop Transfer Payment Budget (Subprocess 1.1.5): Based on transfer payment plans, the transfer payment budget for each program is allocated, taking into account any related assumptions and constraints.

Develop Project Plan and Budget

- Conduct Project Planning and Budgeting (Subprocess 1.1.6): Projects are identified, assessed, planned and approved throughout the fiscal year. The resulting approved projects are an input to the Develop Investment Plan and Budget subprocess group.

Develop Investment Plan and Budget

- Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7): Based on the current approved investment plan and budget, the notional budget allocations, the integrated planning package and any asset assessment results, the capital asset life-cycle requirements are identified, prioritized, budgeted and validated. Requirements may be either capital in nature (relating to new assets or betterments) or non-capital in nature (relating to asset repairs and maintenance or minor capital).

- Conduct Acquired Services Planning and Budgeting (Subprocess 1.1.8): Acquired services requirements and budgets from the capital asset life-cycle and project portfolio plans are summarized. Other operational acquired services requirements are also estimated.

- Conduct Project Portfolio Planning and Budgeting (Subprocess 1.1.9): Budget allocations for in-progress, newly approved, and additional potential projects are validated. The project portfolio plan and budget may also include an allocation of funds to a reserve, to allow flexibility in allocating funds to additional projects during the fiscal year.

- Update Internal Investment Plan and Budget (Subprocess 1.1.10): Based on the capital asset life-cycle, acquired services, and project portfolio plans and budgets, the internal investment plan and budget are updated.

Consolidate and Approve Plans and Budgets

- Consolidate and Approve Plans and Budgets (Subprocess 1.1.11): Plans and budgets are consolidated, reviewed, challenged and approved at the departmental level. Options to address budget pressures or to effectively use surplus funds are also reviewed and approved. Approved budgets are then communicated to responsibility centre managers.

Throughout the Manage Planning and Budgeting business process, plans and budgets are developed and rolled up at various levels within the department. For example, activities within the Develop Revenue, Operating and Transfer Payment Plans and Budgets subprocess group are typically conducted by various responsibility centre managers and are rolled up by business unit, whereas activities within the Develop Investment Plan and Budget subprocess group are conducted using a more centralized approach, within an organization-wide investment management framework. Activities are often completed concurrently because the resulting budgets and plans (revenue, operating, transfer payments, capital assets and project portfolio), pressures, surpluses and risks are interdependent across subprocesses. Once completed, all plans and budgets are consolidated, reviewed, challenged and approved at the departmental level.

5.2 Develop Notional Budget Allocations

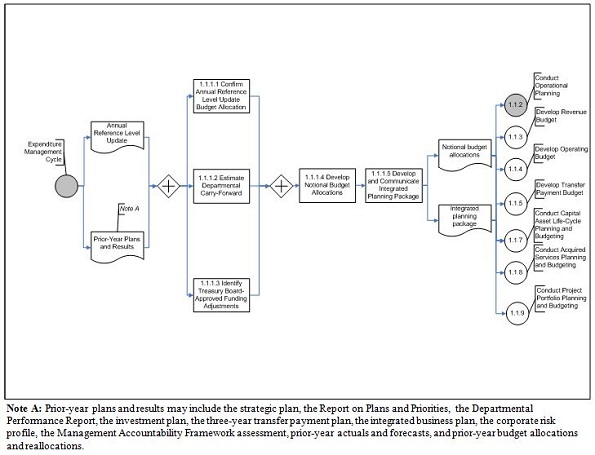

5.2.1 Develop Notional Budget Allocations (Subprocess 1.1.1)

The planning and budgeting process begins with the Annual Reference Level Update as an input to the development of notional budget allocations to responsibilities centres and other planning dimensions, including authorities, objects of expenditure, program activities and projects. Corporate finance is responsible for developing the notional budget allocations, which are envelopes within which responsibility centre managers develop their detailed annual budgets.

Figure 6 depicts the Level 3 process flow for Develop Notional Budget Allocations.

Figure 6. Develop Notional Budget Allocations (Subprocess 1.1.1) – Level 3 Process Flow

5.2.1.1 Activities

The initial departmental budget for the fiscal year is confirmed by comparing the Annual Reference Level Update approved by the Treasury Board with the amounts submitted by the department through the Annual Reference Level Update process (Activity 1.1.1.1 – Confirm Annual Reference Level Update Budget Allocation).

The current-year funds that the department can potentially carry forward to the next fiscal year are estimated using the current-year total annual forecast (Activity 1.1.1.2 – Estimate Departmental Carry-Forward). The maximum amount of carry-forward depends on the stipulation related to lapsing appropriations specified in the department's enabling legislation—the Financial Administration Act or a department-specific act—and the type of vote. For example, Treasury Board permits some departments to carry forward a percentage of the organization's Main Estimates operating budget to the next fiscal year, based on lapses reported in the Public Accounts of Canada. In addition, some departments with separate capital votes in the Main Estimates may also carry forward a percentage of their capital vote to the next fiscal year.

New funding adjustments (for example, Treasury Board submissions, collective agreement adjustments, frozen allotments and budget reductions) that have been approved by the Treasury Board but that have not yet been included in the Estimates are identified (Activity 1.1.1.3 – Identify Treasury Board-Approved Funding Adjustments). Typically, departments receive confirmation of these adjustments through Treasury Board Information Notices or through consultation with their Treasury Board Secretariat program analyst.

Based on the confirmed initial departmental budget outlined in the Annual Reference Level Update, the carry-forward estimate and the funding adjustments approved by the Treasury Board, notional budgets are developed and allocated to responsibility centres and other planning dimensions, including authorities, objects of expenditure, program activities and projects (Activity 1.1.1.4 – Develop Notional Budget Allocations). Whether funds are ongoing (A-base) or sun-setting (B-base) should also be considered when allocating funds to responsibility centres and providing instructions for planning against these funds.

When applicable to the department's financial risk management strategy, the allocation of notional budgets may also include a departmental budget contingency or reserve. If used, contingencies and reserves should be established within a framework that clearly defines how the funds are managed, used and monitored. Departments should consider the risks of allocating budgets in excess of parliamentary-approved funding (for example, carry-forward and funding adjustments approved by the Treasury Board) and should develop appropriate risk mitigation measures.

An integrated planning package is prepared for managers with planning and budgeting responsibilities (Activity 1.1.1.5 – Develop and Communicate Integrated Planning Package). The planning package provides instructions and timelines for completing the planning and budgeting process. The instructions provide managers with guidance on conducting operational and investment planning and budgeting, and integrate both financial and non-financial components. To help align planning and budgeting with the department's overall strategic objectives and operational requirements, the planning package may also provide a summary of high-level planning priorities, assumptions and constraints—for example, budgeting requirements outlined in the Directive on the Management of Expenditures on Travel, Hospitality and Conferences and departmental staffing objectives in support of targeted programs. Key inputs to the planning package may include prior-year plans and results—for example, the strategic plan, the Report on Plans and Priorities, the Departmental Performance Report, the investment plan, the three-year transfer payment plan, the integrated business plan, the corporate risk profile, the Management Accountability Framework assessment, prior-year actuals and forecasts, and prior-year budget allocations and reallocations.

Assumptions and constraints included in the planning package may need to be re-validated throughout the planning process to ensure that any new information is considered in the development of plans and budgets. The notional budget allocations against which managers should plan may also need to be revised with the changes in funding approved during the Manage Planning and Budgeting business process.

5.2.1.2 Roles and Responsibilities

Table 1 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

For Activity 1.1.1.5 – Develop and Communicate Integrated Planning Package, there are two scenarios. In scenario one (S1), the chief financial officer is accountable; in scenario two (S2), strategic and corporate planning is accountable.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.1.1 Confirm Annual Reference Level Update Budget Allocation |

|

CF | CF | TBS-PA | N/A | EMIS |

| 1.1.1.2 Estimate Departmental Carry-Forward |

|

CF | CF | CFO, RCM, SDM | N/A | DFMS |

| 1.1.1.3 Identify Treasury Board-Approved Funding Adjustments |

|

CF | CF | CFO, RCM, SDM, TBS-PA | N/A | DFMS |

| 1.1.1.4 Develop Notional Budget Allocations |

|

CF | CFO | DH, SDM | N/A | DFMS |

| 1.1.1.5 Develop and Communicate Integrated Planning Package |

|

S1: CF, SCP S2: CF, SCP |

S1: CFO S2: SCP |

S1: DH S2: DH |

S1: RCM, SDM S2: RCM, SDM |

DFMS |

5.3 Develop Revenue, Operating and Transfer Payment Plans and Budgets

Operational plans and related budgets are developed and aligned with departmental objectives, priorities, assumptions and constraints. Depending on the structure of the department's budget, not all subprocesses will apply. For example, Develop Transfer Payment Budget (Subprocess 1.1.5) applies only to departments that administer transfer payments.

5.3.1 Conduct Operational Planning (Subprocess 1.1.2)

Based on the notional budget allocations and the integrated planning package, operational plans are developed at the business-unit level by responsibility centre managers. These plans outline the activities that business units will undertake to help the department achieve its strategic objectives. Operational plans include key performance indicators and may include requirements for human resources, information management and information technology, office accommodations and communications. Appendix E provides a list of possible components of an operational plan.

Although the resulting operational plan provides context for the development of budgets and may include a high-level allocation of funds allocated by operational priority, operational planning is largely a non-financial function and is therefore outside the scope of the Manage Planning and Budgeting business process. Consequently, there is no Level 3 process flow or Responsible, Accountable, Consulted and Informed (RACI) table for this subprocess.

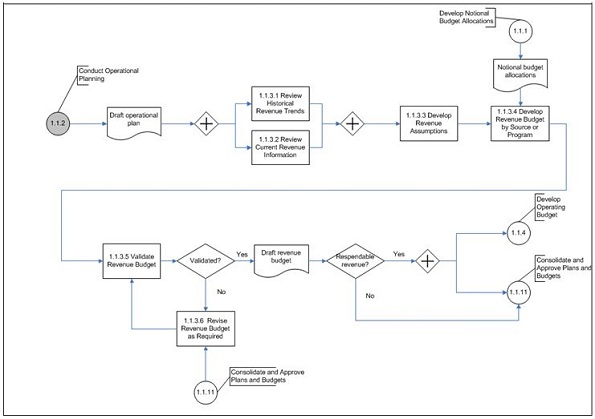

5.3.2 Develop Revenue Budget (Subprocess 1.1.3)

The revenue budget is developed to validate the amount of expected revenue forecast in the Annual Reference Level Update. The budget outlines the expected revenue by program or source and by responsibility centre for the fiscal year, taking into account assumptions, constraints, historical trends and current information. Depending on the department's revenue profile, revenue budgeting may be completed by the responsibility centre manager or may be centralized.

Figure 7 depicts the Level 3 process flow for Develop Revenue Budget.

Figure 7. Develop Revenue Budget (Subprocess 1.1.3) – Level 3 Process Flow

Text version: Figure 7. Develop Revenue Budget (Subprocess 1.1.3) – Level 3 Process Flow

5.3.2.1 Activities

Historical revenue results are reviewed to identify historical trends (Activity 1.1.3.1 – Review Historical Revenue Trends), and current revenue information is reviewed to identify key drivers, including volumes (Activity 1.1.3.2 – Review Current Revenue Information).

Based on historical trends, current revenue information and planned activities outlined in the draft operational plan, the assumptions, constraints and risks that should be considered when developing the revenue budget are identified (Activity 1.1.3.3 – Develop Revenue Assumptions).

The annual revenue budget outlining the forecast revenue to be collected by program or source and by responsibility centre for the fiscal year is developed, taking into account the appropriate assumptions, constraints and risks (Activity 1.1.3.4 – Develop Revenue Budget by Source or Program). The revenue budget covers both respendable (revolving funds and vote netted revenue) and non-respendable revenue. When revenue is respendable, the revenue budget will be an input to Develop Operating Budget (Subprocess 1.1.4).

The revenue budget is validated by key stakeholders (Activity 1.1.3.5 – Validate Revenue Budget); revised as required, with the feedback received (Activity 1.1.3.6 – Revise Revenue Budget as Required); and then re-validated.

5.3.2.2 Roles and Responsibilities

Table 2 provide an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.3.1 Review Historical Revenue Trends |

|

CF, RCM | RCM | N/A | N/A | DFMS |

| 1.1.3.2 Review Current Revenue Information |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.3.3 Develop Revenue Assumptions |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.3.4 Develop Revenue Budget by Source or Program |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.3.5 Validate Revenue Budget |

|

CF, RCM | SDM | CFO | N/A | DFMS |

| 1.1.3.6 Revise Revenue Budget as Required |

|

CF, RCM | RCM | N/A | SDM | DFMS |

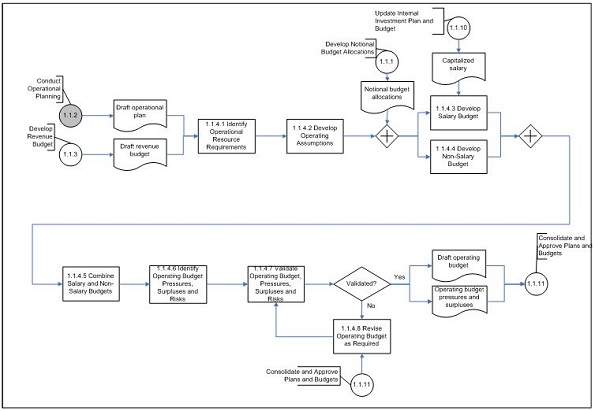

5.3.3 Develop Operating Budget (Subprocess 1.1.4)

Based on operational plans and resource requirements, the operating budget is developed. The operating budget is divided into salary and non-salary components.

Figure 8 depicts the Level 3 process flow for Develop Operating Budget.

Figure 8. Develop Operating Budget (Subprocess 1.1.4) – Level 3 Process Flow

Text version: Figure 8. Develop Operating Budget (Subprocess 1.1.4) – Level 3 Process Flow

5.3.3.1 Activities

Based on the draft operational plan, operational resources required to support planned activities, results and timelines for the fiscal year are identified (Activity 1.1.4.1 – Identify Operational Resource Requirements). Operational resource requirements generally support ongoing activities and exclude resources related to projects and investments.

Based on the operational resource requirements, the assumptions and constraints that should be considered when developing the operating budget are identified (Activity 1.1.4.2 – Develop Operating Assumptions).

The operating budget is developed, taking into account the notional budget allocations, resource requirements, assumptions and constraints. When revenue is respendable, the draft revenue budget is also an input to the development of the operating budget.

The operating budget is divided into salary and non-salary components.

The salary budget is developed by the responsibility manager in consultation with human resources (Activity 1.1.4.3 – Develop Salary Budget). The salary budget is based on validated staffing plans and, when applicable, is reduced by the amount expected to be charged to the capital vote under the investment plan—for example, salary costs for the construction of new capital assets.

The budget for non-salary operating requirements is developed (Activity 1.1.4.4 – Develop Non-Salary Budget). Requirements may include, for example, professional services, travel and hospitality. When developing the non-salary operating budget, the responsibility centre manager may consult with functional experts, such as asset management services or information technology. Note that capital asset repairs and maintenance expenses are planned for during Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7).

The salary and non-salary budgets are consolidated (Activity 1.1.4.5 – Combine Salary and Non-Salary Budgets). Funds may be reallocated to resolve any shortfalls between the two components. The related Employee Benefits Plan costs should be considered when reallocating funds between salary and non-salary budget components. Any budget pressures and surpluses that remain after the operating budget has been consolidated are identified, as are any risks to planned spending (Activity 1.1.4.6 – Identify Operating Budget Pressures, Surpluses and Risks). The operating budget and the related pressures, surpluses and risks are validated by key responsibility centre managers at various levels up to the senior departmental manager (Activity 1.1.4. 7 – Validate Operating Budget Pressures, Surpluses and Risks). The operating budget is revised as required, with the feedback received (Activity 1.1.4.8 – Revise Operating Budget as Required) and then re-validated.

5.3.3.2 Roles and Responsibilities

Table 3 provide an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.4.1 Identify Operational Resource Requirements |

|

CF, RCM | RCM | N/A | N/A | DFMS |

| 1.1.4.2 Develop Operating Assumptions |

|

CF, RCM | RCM | N/A | N/A | DFMS |

| 1.1.4.3 Develop Salary Budget |

|

CF, RCM | RCM | HR | N/A | DFMS |

| 1.1.4.4 Develop Non-Salary Budget |

|

CF, RCM | RCM | AMS, IT | N/A | DFMS |

| 1.1.4.5 Combine Salary and Non-Salary Budgets |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.4.6 Identify Operating Budget Pressures, Surpluses and Risks |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.4.7 Validate Operating Budget, Pressures, Surpluses and Risks |

|

CF, RCM | SDM | CFO | N/A | DFMS |

| 1.1.4.8 Revise Operating Budget as Required |

|

CF, RCM | RCM | N/A | SDM | DFMS |

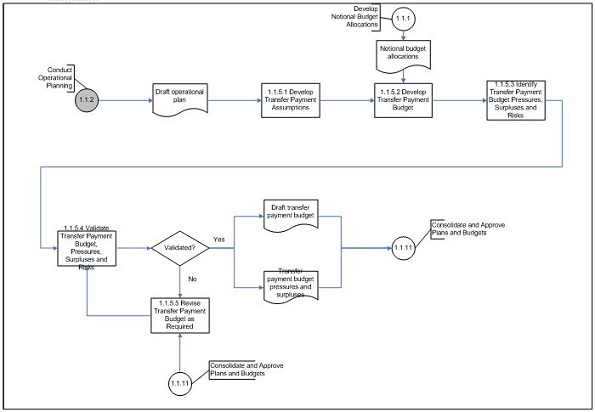

5.3.4 Develop Transfer Payment Budget (Subprocess 1.1.5)

This subprocess applies only to departments that administer transfer payments.

Based on transfer payment plans, the transfer payment budget for each program is allocated, taking into account any related assumptions and constraints. Depending on the department's transfer payment profile, transfer payment budgeting may be completed by the responsibility centre manager or may be centralized by program.

Figure 9 depicts the Level 3 process flow for Develop Transfer Payment Budget.

Figure 9 Develop Transfer Payment Budget (Subprocess 1.1.5) – Level 3 Process Flow.

Text version: Figure 9. Develop Transfer Payment Budget (Subprocess 1.1.5) – Level 3 Process Flow

5.3.4.1 Activities

Based on the draft operational plan, the assumptions and constraints that should be considered when developing the transfer payment budget are identified (Activity 1.1.5.1 – Develop Transfer Payment Assumptions).

The transfer payment budget is developed for each transfer payment program, taking into account the notional budget allocations and the related assumptions and constraints (Activity 1.1.5.2 – Develop Transfer Payment Budget).

Any budget pressures and surpluses are identified, as are any risks to planned spending (Activity 1.1.5.3 – Identify Transfer Payment Budget Pressures, Surpluses and Risks). The transfer payment budget and the related pressures, surpluses and risks are validated by key responsibility centre managers at various levels up to the senior departmental manager (Activity 1.1.5.4 – Validate Transfer Payment Budget, Pressures, Surpluses and Risks). The transfer payment budget is revised as required, with the feedback received (Activity 1.1.5.5 – Revise Transfer Payment Budget as Required) and then re-validated.

5.3.4.2 Roles and Responsibilities

Table 4 provide an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.5.1 Develop Transfer Payment Assumptions |

|

CF, RCM | RCM | N/A | N/A | DFMS or TPS |

| 1.1.5.2 Develop Transfer Payment Budget |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.5.3 Identify Transfer Payment Budget Pressures, Surpluses and Risks |

|

CF, RCM | RCM | SDM | N/A | DFMS |

| 1.1.5.4 Validate Transfer Payment Budget, Pressures, Surpluses and Risks |

|

CF, RCM | SDM | CFO, DH | N/A | DFMS |

| 1.1.5.5 Revise Transfer Payment Budget as Required |

|

CF, RCM | RCM | N/A | SDM | DFMS |

5.4 Develop Project Plan and Budget

Projects are identified, assessed, planned and approved throughout the fiscal year.

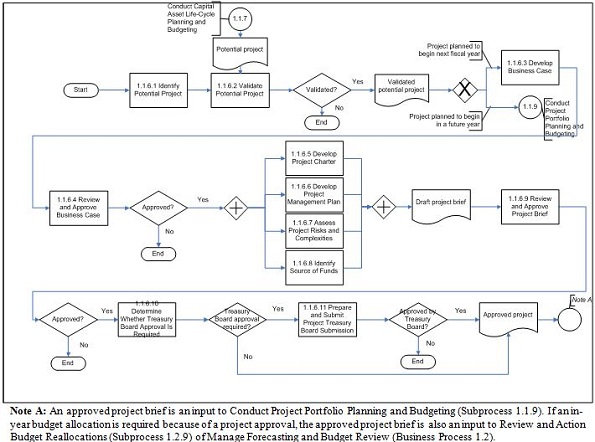

5.4.1 Conduct Project Planning and Budgeting (Subprocess 1.1.6)

The activities within this subprocess support the deputy head in meeting his or her responsibility for ensuring that a department-wide project management governance and oversight mechanism is in place to manage the initiation, planning, execution, control and closing of projects. See footnote [19] Although the other activities within the Manage Planning and Budgeting business process occur before the start of the fiscal year, the activities within Conduct Project Planning and Budgeting may occur at any point in the fiscal year, as new projects are identified, assessed, planned and approved.

Figure 10 depicts the Level 3 process flow for Conduct Project Planning and Budgeting.

Figure 10. Conduct Project Planning and Budgeting (Subprocess 1.1.6) – Level 3 Process Flow

5.4.1.1 Activities

The responsibility centre manager identifies a potential project, typically an investment in acquired services or assets (Activity 1.1.6.1 – Identify Potential Project). An investment is “the use of resources with the expectation of a future return, such as an increase in output, income or assets, or the acquisition of knowledge or capacity.” See footnote [20]

The senior departmental manager sponsoring the project validates the potential project to ensure alignment with departmental objectives (Activity 1.1.6.2 – Validate Potential Project). Potential projects may be identified on an ad hoc basis throughout the fiscal year or as part of Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7). Validation criteria should be established to determine which projects should continue to the business case development phase, as the development of business cases can often consume significant departmental resources.

When the validated potential project is planned to start in the current or the next fiscal year, the responsibility centre manager develops a business case for presentation to the investment management governance (Activity 1.1.6.3 – Develop Business Case). When a validated potential project is planned to start in a future year (beyond the next fiscal year), it should be considered during

Conduct Project Portfolio Planning and Budgeting (Subprocess 1.1.9). Alternatively, the development of the business case may be deferred until a future year.

A business case typically describes the alignment of the project to departmental strategic objectives and the program outcomes expected to be achieved, and provides a cost-benefit analysis and an analysis of the options considered. The business case should also include the resource requirements by fiscal year for the duration of the project, as well as a description of the significance of the project to the department's overall investment plan. The Treasury Board Secretariat's Guide to Costing provides guidance on developing a business case.

Based on departmental business case approval criteria and taking into account all other potential projects validated as part of the Conduct Project Planning and Budgeting subprocess, the business case is reviewed for approval by the investment management governance (Activity 1.1.6.4 – Review and Approve Business Case).

When approval is not granted, the process ends. When approval is granted, the responsibility centre manager prepares a project brief to provide the project approval authority with a more detailed understanding of the project. The project brief summarizes the expected business outcomes, the significance of the project in achieving program and government objectives, potential project options, the performance indicators to be measured, and an evaluation strategy identifying critical milestones, to ensure that objectives are met.

The project brief is also supported by the following key project initiation components:

- Project charter: A description of the project's purpose, objectives, guiding principles, scope, schedule and budget (Activity 1.1.6.5 – Develop Project Charter).

- Project management plan: A description of the performance and outcome measures; evaluation strategy; accountability for outcomes; governance and project team structure, roles and responsibilities; and communication plan (Activity 1.1.6.6 – Develop Project Management Plan).

- Assessment of project risks and complexities: An assessment of the level of risk and complexity for the purposes of project approval authority, conducted in accordance with the Policy on the Management of Projects See footnote [21] and the

Standard for Project Complexity and Risk See footnote [22] (Activity 1.1.6.7 – Assess Project Risks and Complexities). Assessments should be completed using the Project

Complexity and Risk Assessment Tool, which evaluates the level of risk and complexity of individual projects using criteria in the following project knowledge areas:

- Project characteristics;

- Strategic management;

- Contract or procurement characteristics;

- Human resources;

- Business;

- Project management integration; and

- Engineering or technical.

- Source of funds: A description of the planned internal or external source of funds for the project (Activity 1.1.6.8 – Identify Source of Funds).

Depending on the type of project and the departmental project approval framework, additional project documentation, such as an environmental assessment or a privacy impact assessment, may be required.

The investment management governance reviews and approves the project brief and the supporting components to allow the project to proceed and funds to be allocated to the project (Activity 1.1.6.9 – Review and Approve Project Brief).

Although a project may receive internal departmental approval, Treasury Board approval must be sought when the assessed risk and complexity of the project exceeds the assessed class of capacity that the sponsoring minister can approve. See footnote [23] Corporate finance, supported by the senior departmental manager sponsoring the project and by strategic and corporate planning, should determine whether Treasury Board approval is required according to the project approval threshold See footnote [24] above which ministers must seek approval (expenditure authority) from the Treasury Board (Activity 1.1.6.10 – Determine Whether Treasury Board Approval Is Required). The requirements for determining a department's capacity to manage projects are provided in the Standard for Organizational Project Management Capacity. Departments may wish to consult their Treasury Board Secretariat program analyst for assistance.

When Treasury Board approval is required, the Treasury Board submission and the project brief, signed by the minister, the deputy minister and the chief financial officer, are submitted to the Treasury Board (Activity 1.1.6.11 – Prepare and Submit Project Treasury Board Submission). Consultation with the department's Treasury Board Secretariat program analyst may be required to ensure that the submission meets the appropriate requirements. Depending on the type of project, other authorities may be required, such as contracting approval or approval of a real property transaction.

When conducting project planning, the responsibility centre manager may consult with key stakeholders in asset management services, corporate finance, communications, information technology, or strategic and corporate planning, depending on the type of project.

5.4.1.2 Roles and Responsibilities

Table 5 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.6.1 Identify Potential Project |

|

RCM | RCM | AMS, CF, IT, SCP | SDM | DFMS |

| 1.1.6.2 Validate Potential Project |

|

RCM | SDM | AMS, CF, IT, SCP | IMG | DFMS |

| 1.1.6.3 Develop Business Case |

|

RCM | RCM | AMS, CF, IT, SCP | SDM | DFMS |

| 1.1.6.4 Review and Approve Business Case |

|

RCM | IMG | AMS, CF, IT, SCP | N/A | DFMS |

| 1.1.6.5 Develop Project Charter |

|

RCM | RCM | AMS, CF, IT | N/A | DFMS |

| 1.1.6.6 Develop Project Management Plan |

|

RCM | RCM | AMS, CF, COMM, IT, SCP | N/A | DFMS |

| 1.1.6.7 Assess Project Risks and Complexities |

|

RCM | RCM | AMS, CF, COMM, IT, SCP | N/A | DFMS |

| 1.1.6.8 Identify Source of Funds |

|

RCM | RCM | CF | N/A | DFMS |

| 1.1.6.9 Review and Approve Project Brief |

|

RCM, SDM | IMG | N/A | N/A | DFMS |

| 1.1.6.10 Determine Whether Treasury Board Approval Is Required |

|

CF, SCP, SDM | CFO | RCM, TBS-PA | DH | DFMS |

| 1.1.6.11 Prepare and Submit Project Treasury Board Submission |

|

CFO | DH | TBS-PA | CF, RCM, SCP, SDM | DFMS |

5.5 Develop Investment Plan and Budget

In accordance with the Policy on Investment Planning – Assets and Acquired Services, effective investment planning and budgeting should ensure a diligent and rational manner of resource allocation for both existing and new assets and for acquired services. See footnote [25]

In this context, the subprocesses within this subprocess group ensure that the departmental investment plan and budget are developed with due consideration of capital asset life-cycle requirements, investments in acquired services, and project portfolio planning.

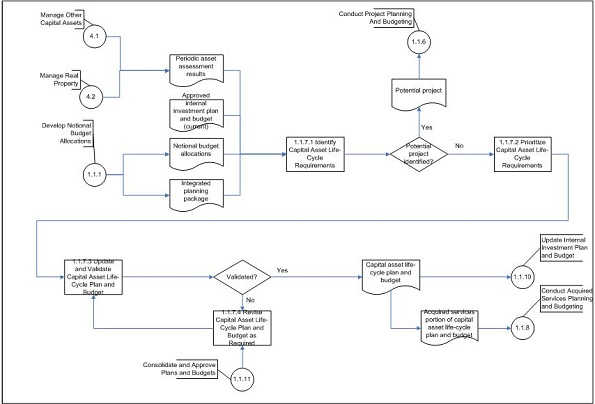

5.5.1 Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7)

Based on the current approved investment plan and budget, the notional budget allocations, the integrated planning package and any asset assessment results, the capital asset life-cycle requirements are identified, prioritized, budgeted and validated. Requirements may be either capital in nature (relating to new assets or betterments) or non-capital in nature (relating to asset repairs and maintenance or minor capital).

Figure 11 depicts the Level 3 process flow for Conduct Capital Asset Life-Cycle Planning and Budgeting.

Figure 11. Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7) – Level 3 Process Flow

5.5.1.1 Activities

Based on the results of periodic asset assessments performed during both Manage Other Capital Assets (Business Process 4.1) and Manage Real Property (Business Process 4.2), the responsibility centre manager identifies capital asset life-cycle requirements (Activity 1.1.7.1 – Identify Capital Asset Life-Cycle Requirements). The current approved internal investment plan and budget, the notional budget allocations and the integrated planning package are also considered when completing this activity. The identification of requirements includes outlining the capital asset replacement, purchase and retirement needs as well as the related budget. Requirements can be capital in nature (relating to new assets or betterments) or non-capital in nature (relating to asset repairs and maintenance or minor capital). Capital asset life-cycle requirements can also include planned asset disposals or retirements and the estimated proceeds from the sale of assets. Requirements that meet the organization's definition of a project should be planned for during Conduct Project Planning and Budgeting (Subprocess 1.1.6).

Based on departmental priorities and available resources, capital asset life-cycle requirements are prioritized over a multi-year time horizon by the investment management governance (Activity 1.1.7.2 – Prioritize Capital Asset Life-Cycle Requirements). With the prioritization, key responsibility centre managers at various levels up to the senior departmental manager update and validate the capital asset life-cycle plan and budget (Activity 1.1.7.3 – Update and Validate Capital Asset Life-Cycle Plan and Budget). The plan and budget are revised as required, with the feedback received (Activity 1.1.7.4 – Revise Capital Asset Life-Cycle Plan and Budget as Required) and then re-validated.

5.5.1.2 Roles and Responsibilities

Table 6 provide an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.7.1 Identify Capital Asset Life-Cycle Requirements |

|

AMS, RCM | RCM | CF | N/A | DFMS |

| 1.1.7.2 Prioritize Capital Asset Life-Cycle Requirements |

|

AMS, IT | IMG | CF, RCM, SCP | N/A | DFMS |

| 1.1.7.3 Update and Validate Capital Asset Life-Cycle Plan and Budget |

|

IMG | IMG | AMS, CF, CFO, IT, SCP | RCM | DFMS |

| 1.1.7.4 Revise Capital Asset Life-Cycle Plan and Budget as Required |

|

AMS, RCM | RCM | CF | N/A | DFMS |

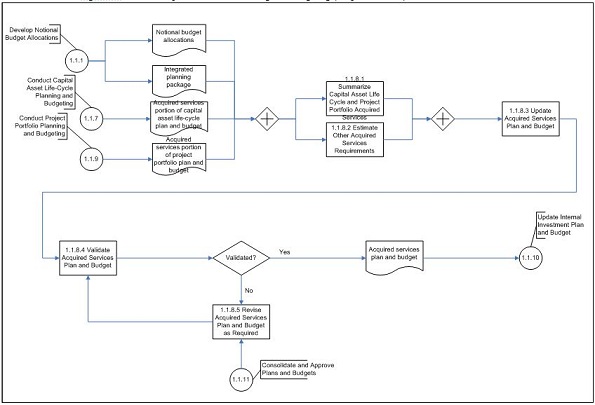

Conduct Acquired Services Planning and Budgeting (Subprocess 1.1.8)

Acquired services are “services obtained through formal arrangements, including contracts, memoranda of understanding, and letters of agreement, to support internal or external clients or stakeholders in achieving specific outcomes.” See footnote [26] Acquired services can be planned as part of capital asset life-cycle planning and budgeting, within the context of a project or to meet operational requirements.

Figure 12 depicts the Level 3 process flow for Conduct Acquired Services Planning and Budgeting.

Figure 12. Conduct Acquired Services Planning and Budgeting (Subprocess 1.1.8) – Level 3 Process Flow

5.5.2.1 Activities

Corporate finance aggregates the acquired services portions of the capital asset life-cycle and project portfolio plans and budgets (Activity 1.1.8.1 – Summarize Capital Asset Life Cycle and Project Portfolio Acquired Services). In addition, other planned acquired services requirements—for example, contracts with a third party to support operational requirements—are estimated (Activity 1.1.8.2 – Estimate Other Acquired Services Requirements).

The acquired services plan and budget are updated to reflect the asset life-cycle, project portfolio and other acquired services investments and related budget allocations (Activity 1.1.8.3 – Update Acquired Services Plan and Budget). The acquired services plan and budget are validated by the investment management governance (Activity 1.1.8.4 – Validate Acquired Services Plan and Budget); revised as required, with the feedback received (Activity 1.1.8.5 – Revise Acquired Services Plan and Budget as Required); and then re-validated.

5.5.2.2 Roles and Responsibilities

Table 7 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.8.1 Summarize Capital Asset Life Cycle and Project Portfolio Acquired Services |

|

CF | CF | AMS, IT, RCM, SDM | N/A | DFMS |

| 1.1.8.2 Estimate Other Acquired Services Requirements |

|

CF | CF | AMS, IT, RCM, SDM | N/A | DFMS |

| 1.1.8.3 Update Acquired Services Plan and Budget |

|

CF | IMG | AMS, IT, RCM, SDM | N/A | DFMS |

| 1.1.8.4 Validate Acquired Services Plan and Budget |

|

IMG | IMG | CF | N/A | DFMS |

| 1.1.8.5 Revise Acquired Services Plan and Budget as Required |

|

CF | CF | AMS, IT, RCM, SDM | N/A | DFMS |

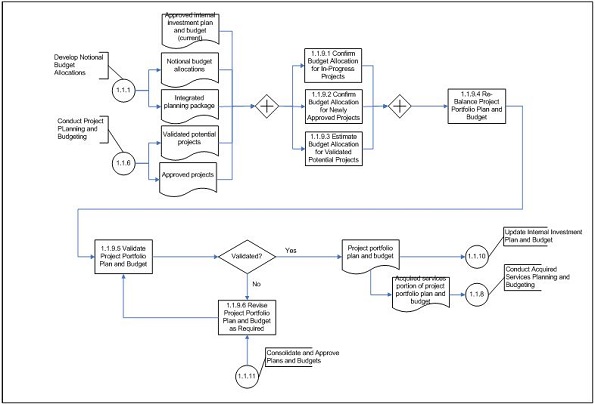

5.5.3 Conduct Project Portfolio Planning and Budgeting (Subprocess 1.1.9)

The Conduct Project Portfolio Planning and Budgeting subprocess determines and validates the allocation of funds to the department's project portfolio. The project portfolio consists of:

- Previously approved projects that are currently in progress;

- Newly approved projects that are projected to begin in the next fiscal year; and

- Additional potential projects that are projected to begin in a future fiscal year.

Figure 13 depicts the Level 3 process flow for Conduct Project Portfolio Planning and Budgeting.

Figure 13. Conduct Project Portfolio Planning and Budgeting (Subprocess 1.1.9) – Level 3 Process Flow

5.5.3.1 Activities

In the context of the current approved internal investment plan and budget, the notional budget allocations for projects, and the integrated planning package, corporate finance confirms the budget allocation for in-progress projects (Activity 1.1.9.1 – Confirm Budget Allocation for In-Progress Projects) and newly approved projects (Activity 1.1.9.2 – Confirm Budget Allocation for Newly Approved Projects) and estimates the budget allocation for validated potential projects (Activity 1.1.9.3 – Estimate Budget Allocation for Validated Potential Projects).

The project portfolio plan and budget are re-balanced within the notional budget allocations for all projects, according to confirmed or estimated amounts for each component (Activity 1.1.9.4 – Re-Balance Project Portfolio Plan and Budget). If permitted as part of the department's financial risk management strategy, the project portfolio plan and budget may also include a reserve of unallocated funds to allow for flexibility in allocating and reallocating project funds during the fiscal year.

The project portfolio plan and budget are validated by the investment management governance (Activity 1.1.9.5 – Validate Project Portfolio Plan and Budget);revised as required, with the feedback received (Activity 1.1.9.6 – Revise Project Portfolio Plan and Budget as Required); and then re-validated.

5.5.3.2 Roles and Responsibilities

Table 8 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.9.1 Confirm Budget Allocation for In-Progress Projects |

|

CF, RCM | CF | AMS, IT | N/A | DFMS |

| 1.1.9.2 Confirm Budget Allocation for Newly Approved Projects |

|

CF, RCM | CF | AMS, IT | N/A | DFMS |

| 1.1.9.3 Estimate Budget Allocation for Validated Potential Projects |

|

CF, RCM | CF | AMS, IT | N/A | DFMS |

| 1.1.9.4 Re-Balance Project Portfolio Plan and Budget |

|

CF | IMG | CFO, SDM | N/A | DFMS |

| 1.1.9.5 Validate Project Portfolio Plan and Budget |

|

IMG | IMG | AMS, CF, CFO, IT, SCP, SDM | RCM | DFMS |

| 1.1.9.6 Revise Project Portfolio Plan and Budget as Required |

|

CF, RCM | CF | AMS, IT | N/A | DFMS |

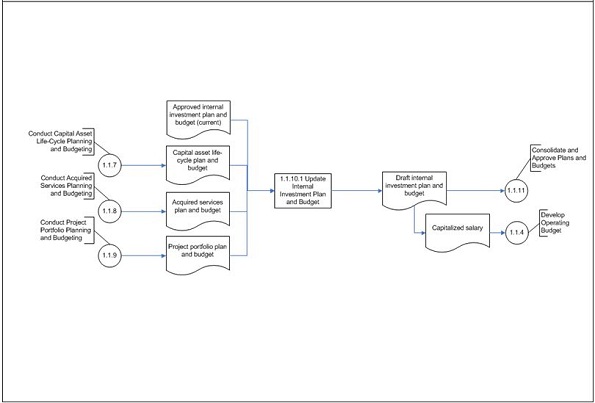

5.5.4 Update Internal Investment Plan and Budget (Subprocess 1.1.10)

The investment plan and budget, which are based on reference levels, provide a summary of future activities and long-term investments that will contribute to the achievement of the department's strategic objectives. See footnote [27] The department's investment plan and budget are submitted to the Treasury Board at least every three years. See footnote [28]

Figure 14 depicts the Level 3 process flow for Update Internal Investment Plan and Budget.

Figure 14. Update Internal Investment Plan and Budget (Subprocess 1.1.10) – Level 3 Process Flow

5.5.4.1 Activities

The internal investment plan and budget are updated with the capital asset life-cycle plan and budget, the acquired services plan and budget, and the project portfolio plan and budget (1.1.10.1 – Update Internal Investment Plan and Budget). If applicable, the amount of salary in the investment plan and budget that is expected to be charged to the capital vote should be deducted from the operating salary budget during Develop Operating Budget (Subprocess 1.1.4).

5.5.4.2 Roles and Responsibilities

Table 9 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.10.1 Update Internal Investment Plan and Budget |

|

AMS, CF, IT | IMG | N/A | DH, SDM | DFMS |

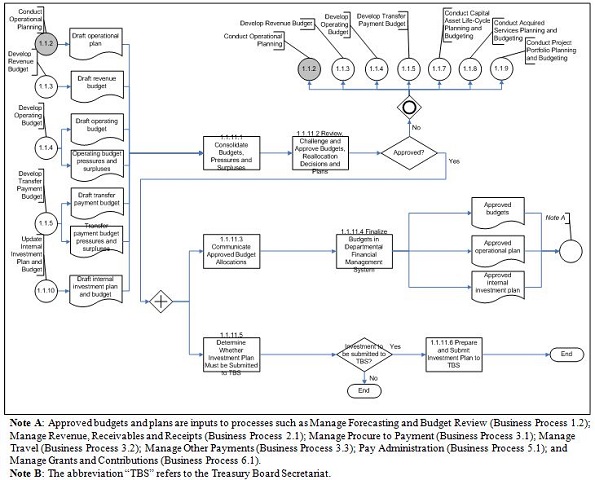

5.6 Consolidate and Approve Plans and Budgets

Plans and budgets are consolidated, reviewed, challenged and approved at the departmental level. Options to address budget pressures or to effectively use surplus funds are also reviewed and approved. Approved budgets are then communicated to responsibility centre managers.

5.6.1 Consolidate and Approve Plans and Budgets (Subprocess 1.1.11)

Figure 15 depicts the Level 3 process flow for Consolidate and Approve Plans and Budgets.

Figure 15. Consolidate and Approve Plans and Budgets (Subprocess 1.1.11) – Level 3 Process Flow

5.6.1.1 Activities

Budgets, pressures, surpluses and plans are consolidated at the departmental level by corporate finance (Activity 1.1.11.1 – Consolidate Budgets, Pressures and Surpluses). The activity also includes a comparison of the consolidated budgets with the department's authorities (for example, vote netted revenue, operating and maintenance vote, transfer payment vote, and capital vote) as well as with the notional budget allocations established during Develop Notional Budget Allocations (Subprocess 1.1.1).

The deputy head, chief financial officer and senior departmental managers review and challenge the consolidation and identify options to reallocate surpluses, to resolve budget pressures. The deputy head approves the budgets, reallocation decisions and plans (Activity 1.1.11.2 – Review, Challenge and Approve Budgets, Reallocation Decisions and Plans). If budgets and plans are not approved, one or more of the following subprocesses may be revisited as required, to address the feedback:

- Conduct Operational Planning (Subprocess 1.1.2);

- Develop Revenue Budget (Subprocess 1.1.3);

- Develop Operating Budget (Subprocess 1.1.4);

- Develop Transfer Payment Budget (Subprocess 1.1.5);

- Conduct Capital Asset Life-Cycle Planning and Budgeting (Subprocess 1.1.7);

- Conduct Acquired Services Planning and Budgeting (Subprocess 1.1.8); and

- Conduct Project Portfolio Planning and Budgeting (Subprocess 1.1.9).

The approved budget allocations are communicated by corporate finance to the appropriate responsibility centre managers and key stakeholders (Activity 1.1.11.3 – Communicate Approved Budget Allocations). Corporate finance also finalizes the approved budget allocations in the departmental financial and materiel management system according to the appropriate budget dimensions (Activity 1.1.11.4 – Finalize Budgets in Departmental Financial Management System). Budgeting dimensions may include authorities, objects of expenditure, program activities and projects.

Following approval of the internal investment plan and budget, the chief financial officer should determine whether the investment plan needs to be submitted to the Treasury Board Secretariat (TBS) (Activity 1.1.11.5 – Determine Whether Investment Plan Must Be Submitted to TBS). Under the Policy on Investment Planning – Assets and Acquired Services, the investment plan must be submitted to the Secretariat at least every three years or at the Secretariat's request. See footnote [29] Although the investment plan is not a vehicle of individual projects, contracts, real property transactions or any other activities cited or referred to in the plan, it is submitted to the Treasury Board Secretariat for review in support of the Secretariat's responsibility for assessing each department's performance in the management of its investment planning process. See footnote [30] Upon review, the Secretariat may also request that the investment plan and budget be submitted to the Treasury Board for approval. The decision to submit the investment plan to the Treasury Board is based on a number of factors, including:

- The significance and risk of planned investments;

- The organization's management performance, established through appropriate management accountability mechanisms and other monitoring activities; and

- The magnitude of changes in planned activities or capacity to deliver. See footnote [31]

When the investment plan needs to be submitted to the Treasury Board Secretariat according to the three-year cycle, or if it has been requested by the Secretariat, steps should be taken to prepare the plan in the appropriate format (Activity 1.1.11.6 – Prepare and Submit Investment Plan to TBS).

The Secretariat receives a high-level strategic document that:

- Defines the direction, capacity and commitments of the department relative to its investment in assets and acquired services;

- Sets out departmental priorities and strategies for the upcoming five-year period clearly;

- Outlines a three-year investment function that meets the needs of the department within available resources; See footnote [32]

- Provides a summary of regular low-risk, planned investments; and

- Highlights and provides more detail on significant investments deemed complex, high-risk, sensitive or extraordinary. See footnote [33]

Departments may wish to consult with their Treasury Board program analyst and review A Guide to Preparing Treasury Board Submissions, to ensure that the plan meets the Secretariat's requirements.

5.6.1.2 Roles and Responsibilities

Table 10 provides an overview of roles and responsibilities, using the Responsible, Accountable, Consulted and Informed (RACI) approach. These roles and responsibilities are further described in Appendix D.

| Activity | Related Data | Responsible | Accountable | Consulted | Informed | Authoritative Source |

|---|---|---|---|---|---|---|

|

Legend

|

||||||

| 1.1.11.1 Consolidate Budgets, Pressures and Surpluses |

|

CF | CF | N/A | CFO, DH, SDM | DFMS |

| 1.1.11.2 Review, Challenge and Approve Budgets, Reallocation Decisions and Plans |

|

CFO, DH, SDM | DH | CF, RCM, SCP | CF, RCM | DFMS |

| 1.1.11.3 Communicate Approved Budget Allocations |

|

CF | CFO | N/A | DH, RCM, SCP, SDM | DFMS |

| 1.1.11.4 Finalize Budgets in Departmental Financial Management System |

|

CF | CFO | N/A | RCM, SDM | DFMS |

| 1.1.11.5 Determine Whether Investment Plan Must Be Submitted to TBS |

|

AMS, CF, SCP | CFO | N/A | DH, IMG | DFMS |

| 1.1.11.6 Prepare and Submit Investment Plan to TBS |

|

CF, CFO | DH | AMS, IT, SCP, SDM | IMG | DFMS |

Appendix A: Definitions

The following definitions apply to this guideline and reflect common definitions used in Treasury Board policies, standards, directives, guides and tools.

- Accountable – RACI:

In the context of the RACI tables, the role that can attest to the truth of the information or a decision and that is accountable for the completion of the activity. There must be exactly one role accountable for each activity.

- Acquired Services:

Services obtained through formal arrangements, such as contracts, memoranda of understanding, and letters of agreement, to support internal or external clients or stakeholders in achieving specific outcomes. See footnote [34]

- Activity:

An elaboration on a subprocess appearing in a Level 3 business process flow. See also Process, Subprocess.

- Annual Reference Level Update (ARLU):

Used to set the expenditure baseline for the direct program spending component of the fiscal plan, reflected in the annual federal budget, and serves as the basis for the appropriations sought from Parliament in the Main Estimates. See footnote [35]

- Appropriation:

Any authority of Parliament to pay money out of the Consolidated Revenue Fund. See footnote [36]

- Appropriation authority:

The means by which Parliament controls the outflow of money from the Consolidated Revenue Fund. See footnote [37]

- Authoritative source – RACI:

In the context of the RACI tables, a system that holds the official version of the information generated by the activity or a decision resulting from the activity. The authoritative source can be automated or manual.

- Cluster group:

A collective of departments working together to promote and implement business-driven and standardized solutions for interoperable financial and materiel management in the Government of Canada. See footnote [38]

- Consolidated Revenue Fund (CRF):

The aggregate of all public moneys on deposit at the credit of the Receiver General. See footnote [39]

- Consulted – RACI:

In the context of the RACI tables, a role that is required to provide accurate information or a decision for an activity to be completed. There may or may not be a consulted role, and consultation may or may not be mandatory. When consultation does occur, there is typically a two-way communication between those consulted and the responsible party.

- Departmental budget:

The overall budget of the department, based on voted appropriations, to deliver the departmental mandate and priorities of the government. The departmental budget normally sets the baseline for the allocation and reallocation of resources within the department for a given fiscal year. See footnote [40]

- Departmental financial and materiel management system (DFMS):

Is a financial management system (FMS) whose primary objectives are to demonstrate compliance by the government with the financial authorities granted by Parliament, comply with the government's accounting policies, inform the public through departmental financial statements, provide financial and materiel information for management and control, provide information for economic analysis and policy formulation, meet central agency reporting requirements and provide a basis for audit. See footnote [41]

- Expenditure Management Information System (EMIS):

The Government of Canada system used to gather information from departments in order to bring together the various pieces of financial information that go into the Estimates and other reports to Parliament.

- Financial Management System (FMS):

-

Is any combination of business processes (end-to-end, automated and manual), procedures, controls, data and software applications, all of which are categorized as either a departmental financial and materiel management system (DFMS) or program system or central system that produces financial information and related non-financial information.

Financial management systems are used for any of the following:

- Collecting, processing, maintaining, transmitting and reporting data about financial events and to maintain accountability for the related assets, liabilities and equity;

- Supporting financial management, planning, budgeting and decision-making activities;

- Accumulating and reporting cost information; or

- Supporting the preparation of internal and external reports, such as departmental financial statements and input to the Public Accounts of Canada. See footnote [42]

- Informed – RACI:

In the context of the RACI tables, a role that is notified of the information or a decision after the decision is made or the activity is completed. There may or may not be an informed role, and informing the role may or may not be mandatory. There is typically a one-way communication from the responsible (or accountable) party to those informed.

- Investment:

The use of resources, with the expectation of a future return, such as an increase in output, income or assets, or the acquisition of knowledge or capacity. See footnote [43]