Rescinded [2016-02-02] - Guide to Costing

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Financial Management and Analysis Sector - Foreword

This Guide to Costing is one of several tools that the Office of the Comptroller General (OCG) has developed to advance stewardship, accountability, and value for money across the Government of Canada. The use of well-prepared, timely cost information contributes to accountability and transparency as well as good decision making and intelligent risk taking.

This Guide replaces the Treasury Board of Canada Secretariat Guide to the Costing of Outputs in the Government of Canada , which has been the main source of costing guidance since it was issued in 1989.[1] The principles that were contained in that Guide have been retained in this Guide as they remain useful and relevant. This new Guide was developed to focus more broadly on costing in recognition of the fact that it has become a common managerial requirement as opposed to one that was relevant to just a few departments and agencies, primarily those with cost-recoverable operations. The management accounting principles and guidelines issued by the Certified Management Accountants of Canada (CMA Canada) were an important source of reference in the development of, and are supported by, this Guide.

This Guide should be used by financial officers and managers at all levels as the official Treasury Board of Canada Secretariat (the Secretariat) reference on costing. It should be used by financial officers when called upon to perform costing, give costing advice, or attest to the accuracy and relevance of cost information; for example, in Treasury Board and Cabinet submissions.

The roles and responsibilities of the parties involved in costing are described in each of the recommended seven steps.

A costing tool kit has been developed as a supplement to this Guide (see Annex B). It was designed to explain fundamental concepts to those who do not have expertise in costing and to show managers and practitioners at all levels how to take a logical, consistent approach when developing and challenging cost information. The tool kit provides a consistent approach to the calculation of cost information that is necessary for planning, resource acquisition and allocation, decision making, performance measurement, reporting, and accountability.

The concepts of "costing," "pricing," and "funding" are easily confused. Costing, pricing, and funding, however, are separate and distinct functions. Costs should be known regardless of whether a charge is being considered and irrespective of the level of funding. The purpose of pricing is to determine what a charge should be or whether it is appropriate to make a charge. Pricing considers many factors besides costs. A comparison of the costs and the funding will reveal if there is a gap that should be addressed in some way. The focus of this Guide is on costing.

All departments and agencies were consulted during the revision of this Guide, and we thank the many who provided comments.

This Guide will be updated periodically as required. Suggestions are welcome.

Inquiries concerning this guide should be directed to the following:

Financial Management and Analysis SectorOffice of the Comptroller General

Treasury Board of Canada Secretariat

L'Esplanade Laurier

300 Laurier Avenue West

Ottawa ON K1A 0R5

Email: fin-www@tbs-sct-gc.ca

Telephone: 613-957-7233

Fax: 613-952-9613

Executive summary

Costing is a business management function that is key to the sign-off of the financial implications of Memoranda to Cabinet (MC) and Treasury Board submissions as well as the sign-off leading to the release of financial statements and reports to Parliament by the chief financial officer (CFO) or the Chief Financial Officer (CFO). Quality, timely costing information supports decision making and performance monitoring. It also enhances transparency when dealing with internal and external auditors along with other third parties. All financial proposals and decisions are strengthened when there is a clear understanding of their complete resource implications.

This Guide, which is based on generally accepted management accounting principles, presents a logical seven-step approach to be used for all costing exercises.

To produce meaningful costing information that will be used by all levels of management, the Guide puts an emphasis on the consultation that must take place between the Deputy Chief Financial Officer (DCFO) organization, program managers, and all other stakeholders to establish a clear understanding of the information needs to which the costing exercise will respond. This consultation will bring together the costing expertise of the DCFO organization and the detailed knowledge of the business functions held by the program managers and the providers of internal services (IS), also referred to as corporate and administrative services (CAS). Under the direction of the DCFO organization, and with the cooperation of these parties, consultation produces complete, relevant, and well-justified costing information.

Another important benefit of following the logical, seven-step approach to costing is that it requires documentation of the underlying assumptions and methodologies used to produce the information, thereby supporting departments' internal sign-off processes. This will enhance the credibility of the information as well as accountability. Departments are encouraged to add to the checklists and internal sign-off processes described throughout this Guide, making them as detailed as required to meet their internal control and accountability needs.

The Guide's logical, seven-step approach to costing includes the following:

- a tool kit to reinforce the logical, seven-step approach;

- a description of the roles and responsibilities arising at each of the seven steps;

- expanded guidance and examples relating to costing methodologies;

- checklists for each of the seven steps, including the internal sign-off;

- a case study; and

- an improved glossary of terms and list of related references.

The seven steps of the Guide to Costing produce information that supports the actions of managers and decision makers, assists the Secretariat in assessing business cases, and enhances reporting and public disclosure of information. Managers may also use the cost information to develop, for example, cost-benefit analyses, risk assessments, or cost-recovery strategies.

Whether departments use sophisticated costing software or more basic cost-finding methods is not important. The choice of method depends on what is feasible and cost-effective in light of their operations. What is important is an understanding of fundamental costing principles and concepts and how to apply them consistently in decision making, performance comparison, and planning, managing, and reporting results and resources.

Introduction

Costing is a business management function that needs to be understood and used effectively by financial officers and managers at all levels. Consultation between the program managers and the department's DCFO organization is essential to the production of quality costing information. DCFOs and their financial officers provide functional direction, guidance, and support to managers on the most appropriate costing methods and practices to meet their needs. Given their expertise, a department's financial officers, under the ultimate direction of the DCFO, should normally take the lead in most costing exercises. Judgment is a critical element in this business management function because costing is not an exact science.

Costing is needed because questions about costs arise virtually every day, such as the following:

- What is the appropriate budget for Program X?

- What does it cost to deliver this service?

- What did it cost to improve the timeliness of this service?

- What will the department's costs be in a joint undertaking?

- What will the additional cost be if client demand increases by 10 per cent?

- What is the difference in cost between providing this function in-house and outsourcing it?

- What are the relevant costs associated with a proposed cost-recoverable arrangement?

- What are the environmental costs associated with this project?[2]

Cost is the value of the resources consumed for something such as an activity, output, or outcome. A question on costs is answered through effective costing, which involves the production of cost information specifically for the purposes intended.

Costing depends on circumstance, the selection of the relevant variables, and the underlying assumptions, which significantly influence the final figures. A costing exercise requires consultation with all stakeholders who may be affected or potentially affected.

Although costing is not an exact science, a logical costing approach should be followed, regardless of the type of cost information required. The Guide to Costing includes the following seven steps:

- Cost purpose: What is the purpose for which the cost information will be used?

- Cost object: What is being targeted for costing (e.g. an activity, output, service, or immediate outcome)?

- Cost base: Which costs are relevant to the cost purpose and object(s)?

- Cost classification: Which costs can be identified directly with the cost object(s) and purpose, and which costs are less direct (such as the cost of supporting activities)?

- Cost assignment: What are the appropriate methodologies for assigning the costs to the cost object(s)? The methods chosen should be reasonable and cost-effective in light of the purpose of the cost information.

- Calculate, validate, and confirm: Apply the costing methodologies, validate the calculations and assumptions, and confirm that the results respond to the cost purpose defined in Step 1.

- Sign-off: Sign-off by CFO for Treasury Board submissions and MCs or underlying internal sign-off as designed by departments to meet their own needs.

Before starting any costing exercise, it is critical for all parties to have a clear and precise understanding of the purpose for which the information is needed. Understanding exactly what decision the information will support is the essential first step. More details on this and the other steps in costing can be found in the costing tool kit found in Annex B.

Objective of this Guide

A premise of this Guide is that all managers need to understand what causes the consumption of resources; i.e. costs and what it costs to produce their services or products. Whether departments use sophisticated costing software or more basic cost-finding methods is not important; the choice will depend on what is feasible and cost-effective. What is important is an understanding of fundamental costing principles and concepts and how to apply them consistently in decision making, performance comparison, and planning, managing, and reporting results and resources. As such, this Guide elaborates on the fundamental costing principles that remain unchanged from the previous version of the Guide. These principles mirror those used in the private sector.

Simply put, the purpose of this Guide is to help departments perform their costing function. This assistance, in turn, will result in more accurate and better-justified costing information that will benefit decision makers in departments and in the Secretariat. It will also make improved information available to parliamentarians and other stakeholders.

Guiding principles

The following seven principles are the foundation for the guidance provided in this document.

1. Costing requires consultation and judgment

Sound costing cannot be performed in isolation. Effective consultation and sound judgment are always required. Consultation among the stakeholders, which may sometimes be extensive, is a fundamental costing principle since all relevant costs often reside throughout the organization. The relevant costs often include IS, program support services, and the costs of common and central services, such as accommodation and employee benefits. For horizontal initiatives, the costs of services in the same department or other departments may be relevant.

As well as stakeholders whose costs may be relevant, there are other parties who may be affected by the purpose and use of the cost information; for example, the Secretariat analyst who has to understand the cost implications of a new initiative included in a submission.

DCFOs and their financial officers are key stakeholders as it is their responsibility to provide sound judgment, advice, and guidance on costing. They will ensure that relevant and reliable cost information and reasonable assumptions are used for financial planning, resource allocation, performance reporting, and, more generally, decision making that will affect resources. It is also their role to recommend a costing approach that balances the level of investment (e.g. in time and resources) needed to generate the information against the benefits of that investment. An excessively detailed approach may be more costly and time-consuming to maintain than is warranted.

2. Costing is done for the purpose intended

Costing must be tailored to the purpose for which the cost information will be used. Before costs can be determined it is critical that all parties agree and understand exactly what decision the information supports. Once that is understood, the task of identifying what information is needed may commence. Examples of two different purposes could be the following: (a) to determine the cost to establish and deliver a new program; and (b) to determine the cost of expanding an existing service to meet additional demands. Each purpose and its different information needs are described in more detail below.

For the scenario in case (a), the purpose is to determine the costs to all stakeholders of establishing and delivering this new program. It is essential to identify and assign all the resources that will be required to support the program. These resources include not only the one-time and ongoing resources that are needed by the organization directly responsible for the program but also any additional resources needed by other organizations that will provide support to the program.

For the scenario in case (b), the purpose is to develop cost information for the preparation of a business case to secure incremental funding to expand this service. It is necessary to identify and assign the additional resources that are required — in other words, the resources that are incremental to the resources already provided for the existing level of service. It is essential to take into account the ability of the organization (or organizations) to absorb any additional workload required to directly deliver or indirectly support the expanded service.

3. Costs do not always vary in proportion to changes in volume

Costs do not always vary proportionately with demand. Numerous variables will influence how costs vary or not, in relation to a change in a situation. The existing capacity to absorb an increase or decrease in volume before any incremental costs are incurred or before any savings are realized should be one of the first considerations of costing. Understanding the fixed and variable costs and the causal relationships that affect cost behaviour is essential. Equally important is determining the costs associated with the initial start-up, steady state, and windup — including disposition and remediation, as well as other one-time costs — and then costing each of the foregoing for the appropriate time period. This principle is explained further under "Cost behaviour" in the Glossary.

4. Costing is done consistently for the same purposes

Where the same circumstances and purposes exist in an organization or department, costing must be done consistently. Otherwise, comparative information used for performance or other purposes will not be valid. Different circumstances could exist within a department where there is, for instance, more than one kind of funding, such as a revolving fund for one program and regular annual appropriations for the other programs. Normally, revolving fund costs will include non-cash items, such as amortization of major equipment, that are not accounted for in cash-based appropriations.If, however, comparisons are made between these two groups of activities, such as the efficiency of performance, identical costing must be done for both.

5. Costing, pricing, and funding are not the same things

Costing, pricing, and funding are three distinct functions.

Costing is an important business management function that is undertaken for various reasons such as measuring performance, aligning resources to results, evaluating efficiency, and reallocating resources. In some instances, costing is also done to calculate the cost (i.e. the value of the resources consumed) of providing products or services. This information should always be established regardless of whether there will be charges for delivering the products or services.

Pricing is undertaken for broader policy purposes. It takes into account a number of factors such as fairness and equity, economic impact on clients, and competition with private sector suppliers. Specific considerations include but are not limited to the following:

- whether the advantage to the government outweighs the start-up and ongoing costs of administering the charges;

- the degree to which price will affect achievement of broader policy objectives; and

- whether the activity in question is a legitimate function of government that cannot be adequately provided by other sectors.

Funding depends on government priorities, affordability, and, in some cases, fee revenue. Any gap between the cost and the funding sources will require management action. At a minimum, this should include a thorough analysis of the costs. If fees are part of the equation, they too should be thoroughly analyzed in the context of program priorities and the associated costs. The information obtained from a rigorous costing analysis will help management make a well-justified case for its recommended course of action.

6. Data and documentation must be reasonable, consistent, defensible, reconcilable, and current

In most cases, it is up to the department to select, justify, and document the most appropriate data source for a particular costing exercise. For the purpose of this Guide, the data source for "costs" may be actual costs, historical costs, budgets, averages, multi-year averages of costs or budgets (adjusted for annual anomalies), estimates, forecasts, or standard costs (see definition in Annex A). Depending on the purpose of the cost information and the availability of data, the financial officer recommends the most appropriate data source. In all cases the choice must be reasonable, consistent, documented, and defensible. Departments should be able to reconcile their ultimate costing results with their main financial management systems.

Departments should document all assumptions, processes, and calculations used to produce the cost information. These, along with the data sources, should be reviewed at least every two years to ensure continuing validity.

7. There must be a balance between the desired elements and the affordability of the costing function

In designing a costing function, departments must strive to balance the following competing elements: level of precision, timeliness, accuracy, complexity, and affordability. Such a balance ensures that departments develop a sustainable costing capability that both meets their needs and is affordable. Situations should be avoided where the investment made to derive costing information exceeds the benefits of that information.

The Guide and different costing purposes

The purpose of this section is to describe some of the more common costing applications in government.

The logical seven-step approach to costing described in the Introduction and throughout this Guide applies to all costing initiatives.

The cost base and cost assignment methodologies that are used depend on the purpose for which the information is required. All parties involved in costing, including program managers, the DCFO organization, and IS (or CAS) must fully understand the purpose of the costing information required before the appropriate costing method is determined. To be consistent with the Management, Resources, and Results Structure Policy (MRRS) and Program Activity Architecture (PAA) instructions, this Guide uses the term "internal services" (IS) in place of "corporate and administrative services" (CAS).

In all cases, the relevance of non-cash costs such as amortization depends primarily on whether the purpose of the analysis being performed is to determine funding implications or to portray the economic impact of alternatives. Non-cash costs are considered only in the latter case.

Understanding the cost implications of a particular decision or initiative helps departments to internally reallocate resources not only from lower to higher priorities but also from one functional area to another. For instance, after performing the costing in support of an MC, a department may determine that resources need to be shifted from a lower priority to a higher one within the department and, further, that resources have to be reallocated to IS to support the delivery of the new MC initiative.

Below are some of the more common costing applications in government and the relevant costs to be considered in each case.

Cost recovery

Knowing the full costs of a product or service (also referred to as an output) is one of the first steps in supporting cost recovery decisions. Cost recovery refers to setting charges to cover some or all of the costs incurred in providing a product or service, rather than funding the product or service solely out of general tax revenues.

The full costing of outputs to support cost recovery rate-setting decisions does not necessarily mean that all costs will be recovered. The recovery of less than full cost may be justified on the basis of policy, program, or administrative grounds. Nevertheless, it is important to be aware of the gap between the costs of delivering a service and the revenues that will be generated. For guidance in setting fees, refer to the User Fees Act , your department's DCFO organization (costing or financial management group), or your Secretariat program analyst. Depending on the question, your program analyst may consult the Financial Management Strategies, Costing and Charging Division in the OCG. Other sources of guidance are listed in Annex D.

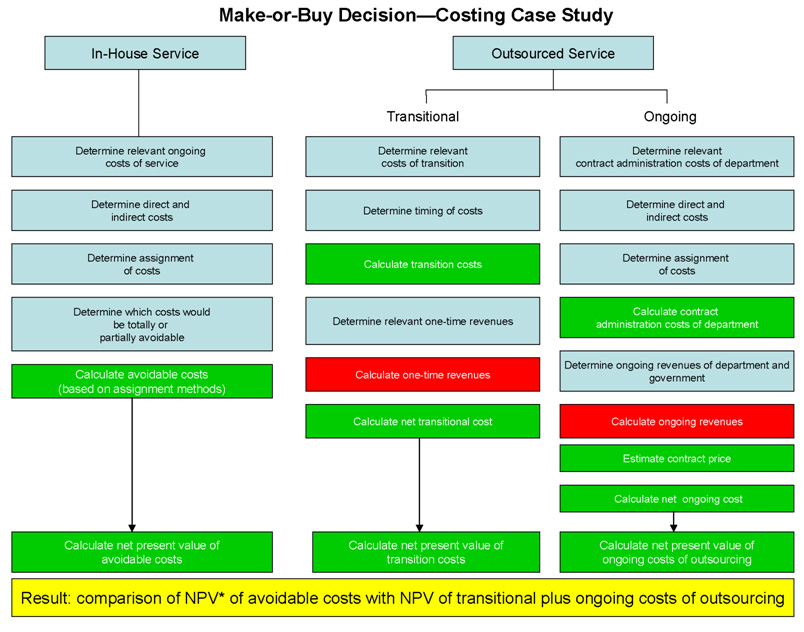

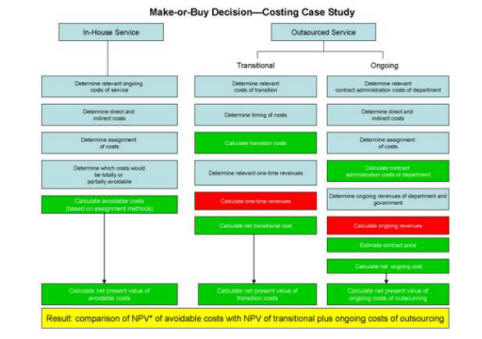

Make-or-buy decisions

A make-or-buy decision determines whether the delivery of a service or a product to users is more efficiently performed by the government or by a third party. For these decisions, relevant costs are limited to those that would change depending on which option is selected. See Annex C for an example.

Level-of-service decisions

These are decisions made by managers regarding the appropriate level of service to provide to users. Relevant costs are those that will change as the level of service is adjusted. For example, a lower level of front-line program delivery may reduce the direct salary and operation and maintenance (O&M) requirements. This may, in turn, have implications on the level and cost of the support functions.

Cost-benefit decisions

Cost-benefit decisions involve assessing alternative courses of action such as whether to acquire an asset or which type of asset to acquire. Relevant costs for these decisions are those that vary depending on the option. Usually non-cash costs such as amortization are not relevant to these decisions.

If the cost of acquiring or disposing of capital assets is relevant to a given cost-benefit decision, a net present value (NPV) methodology should be applied to cash flows to compare alternatives. If the support infrastructure already exists and does not change depending on the alternative, then the associated costs are not relevant. Relevant costs and methodologies are described in depth in the Canadian Cost-Benefit Analysis Guide.

Capital investment decisions

These are decisions concerning the building, creation, betterment, or acquisition of assets; they are a type of cost-benefit decision. They are usually supported by life-cycle costing that captures or predicts all the capital and operating costs of an asset over the four phases of its lifetime: planning, acquisition, operation and maintenance, and disposal. This life-cycle approach is also pertinent to the government's Policy on Green Procurement.

Costing of a new initiative — incremental funding

All the costs of a new initiative for a department must be known, including costs of employee benefits and accommodation. For a new initiative that is incremental to existing programs, it is necessary to know the incremental financial impact; that is, the costs that change as a result of the decision. These normally include the direct and indirect costs that originate in program support and IS. The incremental financial impact may also include the effect on partner departments and on services provided without charge from other government departments (OGD). This same incremental costing approach applies in determining the savings from discontinued initiatives.

Guidance on costing for Treasury Board submissions is provided in the Guide to Preparing Treasury Board Submissions.

Guidance on preparing an MC is available from the Privy Council Office (PCO) and on their website.

Program Activity Architecture (PAA)

The Secretariat's MRRS policy requires that resources be linked to each activity at all levels in the PAA and that each activity be linked to results. This achieves the alignment of resources, activities, and results and the integration of financial and non-financial performance information for decision making as specified in the MRRS. The costing approaches recommended in this Guide should be applied in determining the costs of each level of activity and relevant outputs and outcomes that are specified in a department's PAA.

Reorganizations

Credible, documented cost information is critical to both intra- and interdepartmental reorganizations as well as to the establishment of new governance structures. This information is necessary to ensure that the cost implication of a re-organization is completely understood by all parties. It may also be used by management to negotiate an acceptable amount of resources to transfer within a department or to a new or existing department.

The magnitude of the re-organization is an important factor in determining the relevant costs to analyze. A transfer of two full-time employees (FTE) and their related activities from one unit to another within the same department likely involves only the direct costs (salary and non-salary), with no impact on program support and IS. A government restructuring that sees an entire or significant portion of a function move from one department to another requires a more extensive costing effort. Such a restructuring may involve not only hundreds of FTEs and their direct costs, but it may also require the costing of the associated program support and IS costs that the original host department incurred to support that function.

On the other side of the equation, the receiving department, in addition to the foregoing costs, needs to factor additional elements into its calculation in order to understand the full impact of the transfer on its organization. For instance, the receiving department needs to consider the capacity of its program support and IS areas to absorb the increased demands of supporting the new function, plus any other incremental costs such as relocation, informatics infrastructure capacity, re-training, security, accommodation, and capital requirements. The receiving department may need to identify a source of funds for the incremental costs that will not be provided by the original host department. It also needs to report an increase in services provided without charge from other government departments.

Significant re-organizations, such as the example above, require that communication take place between the parties to ensure that a consistent, apples-to-apples approach is followed in the detailed calculations and that there is mutual agreement as to definitions and what to include and exclude. All parties should use the seven-step approach presented in this Guide.

Cost efficiency decisions

Costing provides information for measuring the cost-efficiency of operations. For example, are the unit costs of outputs going up or down? An input-to-output ratio expressed in dollar terms helps in analyzing efficiency.

Cost information only provides a measure of cost performance; it is not a measure of overall performance. While cost information definitely enhances the assessment of performance when, for example, comparing actual to budget costs, it has to be balanced against non-financial performance information, such as quality (e.g. the accuracy of claims processed) and timeliness (e.g. the speed with which client demands are met).

The seven-step approach to costing

Given the diversity in the nature, size, and complexity of federal government departments, each assesses its own needs and the needs of its stakeholders for cost information. This assessment, in turn, informs the appropriate depth and scope of costing required to respond to those needs.

This Guide is designed to help departmental managers and financial officers reinforce the costing practices that best suit their own information needs. It can be applied globally, at a government-wide or departmental level, or at the sub-subactivity level of a departmental program. No matter what the level or the relative importance of the cost information, the principles of the costing approach are the same and the series of steps it lays out should always be followed.

The steps must be taken in sequence; the extent of effort taken at each level to achieve the required result, however, depends on the purpose of the cost information and how it will be used.

Although costing is not an exact science, the seven steps must be followed regardless of the nature of the costing exercise. The first step is to clearly define the purpose for which the information is needed. Clear definitions are also required for each of the succeeding steps.

A brief description of each of the seven steps is provided below. Each is explained more fully in Annex B — Costing tool kit, along with the responsibilities for performing each step and supporting checklists.

- Determine the cost purpose: What is the purpose for which the cost information will be used?

- Determine the cost object: What is being targeted for costing, e.g. an activity, output, service, or immediate outcome?

- Determine the cost base: Which costs are relevant to the cost purpose and object(s)?

- Determine the cost classification: Which costs can be identified directly with the cost object(s) and purpose, and which costs are less direct, such as the cost of supporting activities?

- Determine the cost assignment methodologies: What are the appropriate methodologies for assigning the costs to the cost object(s)? An overriding principle is that the methods chosen should be reasonable and cost-effective in light of the purpose of the cost information.

- Calculate, validate, and confirm: Apply the costing methodologies, validate the calculations and assumptions, and confirm that the results respond to the cost purpose defined in Step 1.

- Get sign-off: Sign-off by CFO for Treasury Board submissions and MCs, or underlying internal sign-off as designed by departments to meet their own needs.

Annex A — Glossary of key terms and concepts

Introduction

Costing definitions used in the private and public sector were reviewed as part of the research for this Guide. Although it was found that there is no absolute consistency, the general meaning of common terms and concepts is very similar. At the same time, definitions for a few costing terms may vary under certain circumstances.

The definitions in this Annex are intended to be generally applicable to most costing applications in federal government departments.

- Accrual versus expenditure accounting

- There are a number of differences between accrual and modified cash accounting, but the main ones from a costing perspective relate to timing and treatment of assets and liabilities. For more information, please refer to the Financial Information Strategy Accounting Manual.

- Activity

- An activity is the work that is done to achieve an output, such as a product or service. It is a component of a program and may include several levels of activities (i.e. activity, subactivity, and sub-subactivity) at the level of detail needed to manage a program and its services successfully. A departmental activity structure used for costing purposes should be consistent with the department's PAA.

- Allocating costs

- Allocating is the action taken to apportion a cost when it benefits two or more objects. The term "allocating costs" is often used interchangeably with "cost assignment." When a cost cannot be directly identified with a single cost object, it must be allocated to the two or more objects it benefits on a basis that is as fair and accurate as possible based on the relative share that each cost object has consumed. If an engineer is engaged in three different activities, his or her salary cost would need to be "allocated" to each of these activities on some reasonable basis, such as the estimated time spent engaged in each activity. Wherever feasible, costs should be allocated on a causal basis (e.g. time spent). In cases where this is not feasible or practical, another reasonable basis for allocation should be used, such as the number of FTEs or percentage of budget. In choosing a cost allocation method, a balance should be maintained between the level of effort invested in the method and the usefulness of the information produced. In other words, a more precise allocation method may not be worthwhile for a cost that is not material. See also "Cost assignment."

- Amortization

- This is the allocation of the historical cost of an asset (e.g. buildings, motor vehicles, and major equipment) over the course of its useful life.

- Attributing costs

- See "Cost assignment."

- Avoidable costs

- These are costs that can be avoided by not performing an actual or planned activity or service. Not all relevant costs are avoidable; e.g. some program management and some IS costs may not be avoided by discontinuing an activity. See also Annex C — Case study of a make-or-buy decision.

- Business-sustaining costs

- These costs refer to some activities in an organization that do not directly contribute to the end cost objects yet which cannot be eliminated or reduced without harming the organization. Preparing regulatory reports or closing the books at year-end are examples of business-sustaining costs that benefit the organization as a whole but often cannot be logically traced to clients or services. Depending on the defined purpose of the costing exercise, along with any other imposed constraints (e.g. determining full cost under the Common Services Policy ) it may or may not be appropriate or even required to allocate these costs to cost objects. Recovering these costs via cost recovery may eventually be required. "Business-sustaining costs" and IS costs offer views of selected parts of the organization through different lenses. They are informed by the defined purpose and are not necessarily identical. Business-sustaining costs are sometimes referred to as organization-sustaining costs.

- Capital asset

- A capital asset is the cost of an asset with a life of more than one year. These are assets owned by a department, including land, buildings, equipment, furniture and fixtures, and motor vehicles. Capital assets include both real property and movable assets but exclude inventories that are consumed in the delivery of services or the manufacture of products. Guidance on the definition of fixed assets can be found in the Treasury Board Accounting Standards. Direction on valuation and amortization of assets can also be found in the Treasury Board Accounting Standards as well as in the Financial Information Strategy Accounting Manual.

- Corporate and administrative services (CAS)

- See "Internal services."

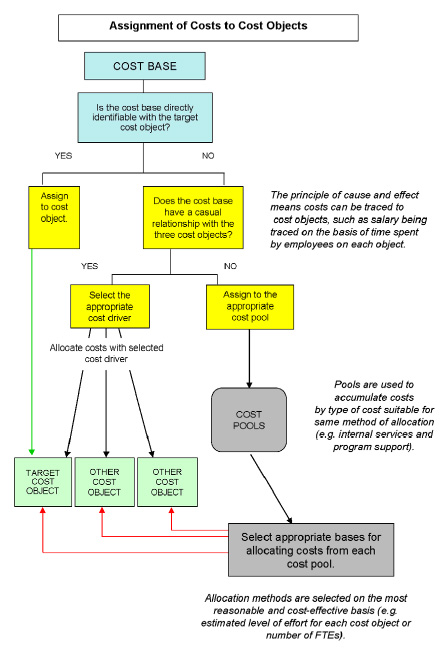

- Cost assignment

Cost assignment is the process that identifies costs with cost objects, such as activities, products, or services. Cost assignment should be performed by the following methods, listed in the recommended order:

- Direct assignment: Costs should be assigned by direct assignment where they can be directly identified with a single cost object, which is the case for the salary cost of an employee who is fully employed in a cost object.

- Assignment of costs on a cause-and-effect basis: Costs should be assigned on a cause-and-effect basis where costs are identified with two or more cost objects, which is the case for the salary cost of a manager who supervises a number of activities. Here the costs are assigned on a causal basis, such as time spent on each activity. Depending on the volume and circumstances, cost pools may be advisable.

- Allocation of costs on a reasonable and consistent basis: Costs should be allocated on an otherwise reasonable and consistent basis in cases where a causal relationship cannot be identified, or where it is not feasible to assign costs based on an identifiable causal relationship. For example, corporate human resource costs may be allocated to activities on the basis of the number of FTEs assigned to each activity. Depending on the volume and circumstances of the costs, cost pools may be advisable.

In all cases, the assumptions, methodologies, and source data used must be credible and documented.

See also "Allocating costs."

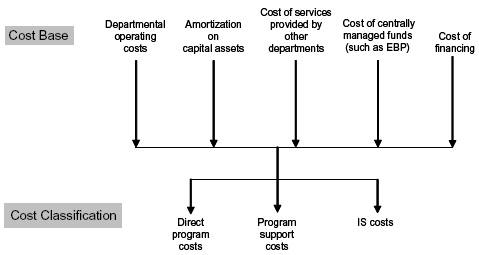

- Cost base

Cost base is the accumulation of all the costs that are considered relevant to the costing of a cost object, taking into account the purpose of the costing. Depending on the purpose of the cost information, it may not be appropriate to include all of the types of costs listed. The types of costs that should be considered for inclusion in the cost base are as follows:

- direct program costs;

- program support costs;

- IS costs;

- the costs due to the employee benefit plan (EBP) conversion factor in the case of transfers between salary and non-salary;

- accommodation costs where the department is the custodian;

- amortization charge for the capital assets used directly and indirectly by the cost object;

- financing costs on the drawdown (this applies to revolving funds only); and

- costs of services provided at no charge by other departments such as contributions covering the employer's share of employees' insurance premiums paid by the Secretariat; workers' compensation coverage paid by Human Resources and Social Development Canada (HRSDC); accommodation paid by Public Works and Government Services Canada (PWGSC); and legal services paid by the Department of Justice Canada (JUS).

It is always important to consult with the DCFO organization and other affected stakeholders to ensure that all relevant costs are included in a cost base. The source of relevant costs may be the actual or average expenditures, budgets, or standard costs or even multi-year averages of expenditures or budgets. Adjustments may be warranted to remove anomalies, such as the costs associated with one-time events that would otherwise distort the costing results. Depending on the purpose of the costing information and the availability of data, the DCFO organization will recommend the most appropriate approach and data source. For instance, estimated budget data is recommended if costing a new product or service, whereas a multi-year average of actual expenses, adjusted where appropriate to remove one-time costs, lends more credibility to the costing of a significant transfer resulting from an internal reorganization; judgment is necessary in cases like this because an historical average might still need to be adjusted to account for known future costs in order to arrive at a reasonable amount to transfer.

- Cost behaviour

Cost behaviour is the way that costs change in response to different variables. Cost behaviour is the key to determining causal relationships. It is based on the premise that costs do not all necessarily change correspondingly to variables. For example, the cost of stamps will vary with the number of mailings, but the cost of the mailroom's staff and their accommodation may be unaffected by this variable.

It is important to examine cost behaviour using historical cost information. Historical cost information helps improve the integrity of cost information that is used for performance measurement and for resource planning purposes. It is equally important, however, to address cost behaviour through consultation with the providers of the services that support the initiative in question, as historical data alone may not be sufficient. For example, through discussions with representatives from communications or legal services, it may become apparent that even though the initiative in question is relatively modest it is very sensitive in nature, and the communications and legal costs may be disproportionately high when compared to another, seemingly similar initiative.

Cost behaviour analysis is also important in the determination of incremental costs.

- Cost driver

- Cost drivers determine how a cost will vary and the rate at which that cost will vary. Cost drivers are the factors that cause changes in the level of resources consumed. Appropriate cost drivers are identified through an analysis of what causes resource requirements. There are many kinds of cost drivers, including clear numerical drivers, such as the number of units produced or the number of transactions which may drive data processing operation costs. More qualitative drivers include the complexity of procedures to the amount of seating in a client waiting room; departmental FTEs may also drive the costs incurred by the human resources (HR) function.

- Cost object

- Cost object is the term used to describe what is being costed. It can be almost anything, such as an activity, program, product, service, client, organization, or outcome.

- Cost of capital

- See "Cost of financing."

- Cost of financing

- The cost of financing is the cost of the interest charged to revolving funds on the amount of the drawdown used. The financing rate to apply for financing costs should be the current Consolidated Revenue Fund lending rate that is published by the Department of Finance Canada.

- Cost pools

For the sake of efficiency, costs may be accumulated into cost pools to facilitate different methods of allocation. Generally, the number of pools should be kept to a minimum and each pool should consist of homogeneous or " like" costs. For example, the HR and legal services costs may be accumulated into separate cost pools because each has a different relationship with the cost objects. Another cost pool may be used for all the other costs, which may be allocated on the basis of, for example, the percentage of total expenditures. Cost pools are also an efficient way of allocating numerous, relatively small value amounts to cost objects.

While the costs assembled in pools may come from different sources (e.g. different organizations or activities) and be made up of different types of resources (e.g. office supplies and postage), they are the same with respect to basis of allocation. For example, it may be decided that the IS costs from a number of different branches, such as finance, HR, and information technology (IT), which comprise many different types of costs (e.g. salary and non-salary), should be assembled in a single pool for allocation to direct programs on the basis of the number of FTEs.

Cost pools may also be necessary for subsequent allocations. For example, after costs have been allocated to an activity, it may be appropriate to accumulate the costs in this activity in cost pools for allocation to a number of cost objects (such as different product lines). An example is a building maintenance activity: the costs are accumulated in two cost pools, one for cleaning costs and the other for security services costs. This is useful if it has been decided that an appropriate causal basis for allocating cleaning costs is square metres of office space occupied and an appropriate causal basis for allocating security services costs is the number of employees in each service line. For a fuller discussion of cost pools, please refer to the section on cost pools in Step 5 of this Guide.

- Cost

- Cost is the value of resources (human, physical, or financial) consumed by a cost object. Cost can include both the direct resources consumed and an allocation of support services consumed by the cost object. Judgment is required to determine which costs to include and to what extent to include them.

- Costing versus pricing

- "Costing" and "pricing" are two distinct concepts. The cost of a cost object, such as a product or service, should always be determined regardless of whether there is a charge for the product or service. Pricing a product or service is a policy decision that may take into account a number of other factors besides cost, such as fairness and equity, economic impact on clients, and competition with private sector suppliers.

- Costing

- Costing is the action taken to determine the cost information required for a defined purpose. The information derived from costing will support many types of business management decisions.

- Direct costs

Direct costs are incurred as a result of the production of a good or the provision of a service, and they can be attributed directly to the good or service. Direct costs are relatively straightforward to identify and measure. Normally direct costs include direct labour; direct operating (such as matériel , travel, and professional services); and capital acquisitions (to the extent that these capital acquisitions will contribute to an output).

Care needs to be taken in how the terms "direct cost" and "indirect cost" are understood. The term "direct costs" is often used to describe program costs, and "indirect costs" to describe IS costs. This can be misleading in some instances, because although program support costs are "indirect" in relation to subactivities, they are "direct" at the program level. The same relative distinction applies to IS costs: if the cost object is an operational program, IS costs are considered "indirect," whereas IS costs are considered "direct" if the cost object is the department as a whole.

- Employee benefits

- These include employer contributions to employee benefit plans (EBP) such as superannuation, Canada Pension Plan, Québec Pension Plan, severance pay, and unemployment insurance contributions paid by departments. Employee benefits also include costs assumed by the Secretariat, such as the Disability Insurance (DI) Plan and the dental plan as well as costs for workers' compensation. On an annual basis, the Secretariat publishes the percentage to be applied to salary costs for these employee benefits. Consult the detailed instructions for the preparation of the Annual Reference Level Update(ARLU), being careful to select the appropriate year. Just like other costs that are not incurred directly by a department, employee benefit costs are only included when they are relevant.

- Fixed assets

- See "Capital assets."

- Full cost

The purpose that is served by the cost information influences what to include in the full cost. In addition, the context in which the full cost is being calculated may also influence the full cost. For instance, different funding mechanisms have an influence, as does the Common Services Policy , which defines full costs for its application. Because "full cost" is a subjective term, judgment is required in all instances to determine the scope of the indirect costs to allocate to the cost object. The indirect costs to be considered for inclusion include program costs at the regional and national headquarters (HQ) levels, program support costs at the regional and HQ levels, IS costs at the regional and HQ levels, EBP, amortization, cost of financing, and services provided without charge by OGDs.

When the full cost is calculated, care must be taken not to obscure the reporting of costs for which managers are held accountable. Any allocations of costs that are made from activities over which the managers have no control should be identified separately. The same holds true for any allocation of services provided without charge by OGDs.

It is essential that the person or persons responsible for conducting a costing exercise document which costs are included and excluded, along with supporting justification

The following are examples of how the definition of full cost can vary in different circumstances.

The type of funding arrangement influences the calculation of full costs. The full cost of a service funded by a revolving fund normally includes financing costs, whereas these costs are not included when costing a service funded by an appropriation.

Full costs can also vary to meet internal as opposed to external reporting requirements. In an external report it may be appropriate (depending on the purpose and the audience) to include in the cost of a program all of the departmental costs it consumed, in addition to the cost of services provided without charge by OGDs. On the other hand, an internal report that is being used for monthly budget variance tracking excludes any costs that are not controlled by the program manager, such as IS costs. The cost of any services that are provided without charge by OGDs are likewise excluded.

- Incremental costs

Incremental costs are the increases or decreases in the costs of cost objects that result from new circumstances. Examples of new circumstances include the following:

- a decision to increase or decrease levels of service;

- a decision to add a new service component; and

- any change in operations.

Incremental costing recognizes that some of the costs of an object do not change, or do not change proportionally, when conditions change. For example, existing building and major equipment costs may be unaffected by program changes, and other costs such as IS may be only marginally affected. Where a service unit has excess capacity, even direct service delivery costs may not be affected by a decision to increase service levels. Similarly, a decision to decrease service levels may only produce minor savings because it may not be feasible to reduce many of the costs, such as those related to FTEs.

- Indirect costs

- Indirect costs are costs that have to be allocated because they apply to more than one cost object. Indirect costs most often originate in program support and IS functions.

- Internal services (IS) —

Sometimes referred to as corporate and administrative services (CAS), these functions incur costs in support of departmental programs and activities. IS costs are normally incurred outside of program branches for the benefit of the department as a whole. For cost allocation purposes , IS costs are distinct from program support costs, which originate within a program.

Please refer to the profile of internal services for the most current list of IS.

IS costs are sometimes incurred in both headquarters and regional program branches in a decentralized environment, but they should still be accounted for as IS costs forallocation purposes.Also for cost allocation purposes , IS costs are distinct from program support costs, which originate within a program.

Depending on how a department or agency is organized and where it sources the IS that it consumes, the functions that IS would typically include are as follows:

- management and oversight services;

- communications;

- legal;

- human resource management;

- financial management;

- information management;

- information technology;

- travel and other administrative services;

- real property;

- materiel; and

- procurement.

- Marginal cost

- A marginal cost is a change in total costs as a result of a change in volume. The term "marginal cost" is sometimes used in place of "incremental cost." However, most costing and economics glossaries define "marginal cost" as the change in total costs of production when output is varied by a single unit. "Incremental cost" generally has a broader definition because as well as including changes in costs resulting from volume changes it also applies to changes in costs that come from other factors, such as a new task or service, and a change to any portion of an operation.This Guide uses the concept and term "incremental costs."

- Materiality

- Determining whether an item is material depends on the degree to which omitting information about the item makes it probable that the decision of a reasonable person relying on the information would be changed or influenced by the omission.

- Organization-sustaining costs

- See "Business-sustaining costs."

- Output

- Output refers to a product or service provided on behalf of a client, regardless of whether the client is within or external to the department.

- Product

- A product is a tangible output generated by a departmental program. An example is a publication produced by Statistics Canada.

- Program support costs

- These are costs of a program incurred in the performance of functions that are not directly involved with service delivery but that support service delivery activities. Program support includes supervisory, administrative, management, and policy functions within a program branch. These costs may be incurred within the program branches at HQ or in the regions. Program support costs are separate and distinct from IS costs, which are support costs incurred outside the program branches for the benefit of the department as a whole.

- Purpose

- Costing is tailored to the purpose for which the cost information will be used. Before costs can be determined, it is critical that all parties agree and understand the purpose; i.e. exactly what decision the information will be used for. Once the purpose is understood, the task of identifying exactly what information is needed may commence.

- Relevant costs

The relevanceof a cost is determined by the purpose that is served by the cost information. For example, relevant costs differ in the following scenarios: (a) the purpose is to determine the increase in costs that result from an increased number of clients; and (b) the purpose is to report the total annual cost of providing a program to the public. In the first scenario the cost of services provided without charge by OGDs are probably not relevant (provided they are fixed over the short term and do not vary as a result of the increase in the number of clients), while in the second scenario the OGDs' costs are relevant because the purpose is to disclose the full cost to the government of delivering the program.

In another example, if the purpose is to compare, among regions, the costs that are "controllable" by the regional managers, departmentally controlled costs such as the costs of program design and transformation are not relevant, even if they could be included in the full costs of regional services.

In all cases, it is important to document the costs that are deemed relevant, the justifications for these decisions, and the sources of the information that supports these decisions.

- Services provided without charge

- These are services provided, free of charge, by a department that significantly benefits one or more other departments. The estimated costs of services provided without charge are reported in the receiving departments' reports on plans and priorities (RPPs) and departmental performance reports (DPRs). The information is obtained directly from the departments providing the services. Examples of these services include the following:

- PWGSC — accommodation services;

- HRSDC — workers' compensation claims;

- JUS — legal services; and

- the Secretariat — employer's share of employees' health care premiums.

- Service

- Service is an intangible output generated within a department on behalf of either internal or external clients. It includes IS performed by other internal branches, such as staffing and program services.

- Standard cost

- Standard cost is the predetermined cost of a cost object that is used for costing purposes. Standard costs are generally calculated on a per-unit basis, such as cost per output or cost per person-year (for a specific job classification and level). The seven-step approach presented in this Guide should be used to establish standard costs. Standard costing is useful in circumstances where there is reasonable consistency in operations, e.g. where the type and volume of work is fairly uniform. In this kind of situation, standard costs can be used for budgeting, controlling, MCs and Treasury Board submissions. Standard costs are also useful for performance measurement purposes.It is important to regularly review standard costs against actual costs to ensure that they are still reasonable. This review should take place no less frequently than every two years.

- Unit cost

Unit cost is computed by dividing the total cost of a cost object, such as an activity, by its volume of outputs. Unit cost serves as a measure of cost efficiency when comparing unit costs over different periods.

Annex B — Costing tool kit

Introduction

This tool kit provides a handy summary that managers and financial officers at all levels can use to apply the seven-step approach to costing. It is designed to supplement the main body of this Guide by demonstrating how readers can use a logical, consistent approach in developing and challenging the cost information needed for planning, resource acquisition and allocation, decision making, performance measurement and reporting, and accountability.

If applied consistently, this costing approach for DCFOs and their financial officers to follow in consultation with program managers will result in quality costing information for deputy heads and departments, while at the same time recognizing the diversity and complexity of operations across government.

Accountability for the accuracy and quality of cost information rests with departments and managers at all levels in general and the CFO in particular. CFOs need to demonstrate that the cost information they provide and attest to, such as for Treasury Board submissions and MCs, was developed on the basis of the costing approach in this Guide.

Costing should not be performed by one individual in isolation. Consultation is essential between program managers, the DCFO organization, the providers of IS, and other departments affected by the initiative being costed should also be consulted. Depending on the circumstances and the complexity of the costing exercise, the DCFO organization may also need to consult the appropriate Secretariat program analyst; departmental legal services; departmental economists; Secretariat Regulatory Affairs; or the Financial Management Strategies, Costing and Charging Division of the OCG. These types of consultations will ensure that the resulting cost information and its implications are complete, reliable, and understood by all affected stakeholders.

The templates and sign-off checklists presented throughout this Annex should be considered a minimum standard. Departments are encouraged to add to these to meet their particular needs.

Costing

Costing is a business management function used to calculate the cost (dollar value of resources consumed) of something (cost object) relative to the purpose for which the cost information is used.

Costing is purpose-based. For example:

- If the purpose is to know the full cost, such as of an activity, it is necessary to calculate the cost of all the resources consumed (human, physical, and financial); and

- If the purpose is to know the incremental cost, such as of an increase in demand or improvement in the quality of a service, it is only necessary to calculate the cost of additional resources consumed.

Costing uses accepted methodologies for calculating the costs (resources consumed) that are relevant to the intended purpose.

Examples of why costing is needed

Budgeting and resource proposals

Costing is needed to answer questions related to the resource implications of proposals. For example:

- What will it cost to deliver this new program?

- What are the additional costs of this higher-quality service?

- What is an appropriate budget for this program, project, or activity?

- What are the life-cycle costs associated with this major capital expenditure?

- How does this initiative affect the costs of other programs?

- What are the environmental costs of a proposed project?[3]

Internal control and performance measurement

Costing information is needed to assist in controlling costs, manage risks, and answer questions related to performance. For example:

- What is the cost per unit this period compared to the last period for a type of product or service?

- How is the cost per client measured?

- How can one fairly compare the cost of providing a service in one region with other regions?

- Are products and services being delivered cost-efficiently?

- Are outcomes being achieved cost-effectively?

- Why are actual costs higher or lower than budgeted?

Internal and external charging

Costing is needed to answer questions related to new charging initiatives. For example:

- With respect to determining an appropriate fee, what are the full costs of the inspection services provided to a specific industry sector?

- What is the incremental cost of providing a one-time service to another department pursuant to the interdepartmental charging rules?

- How is the unit cost established for publications sold to the public?

Costing is also needed to answer questions related to the regular review of existing fees and charges. For example:

- What are the current costs of producing a product for which the fee was established several years ago?

- What amount of costs would not be recovered if the charge for this service were reduced?

Costing and pricing of products and services are separate functions.

Costing is performed to determine the value of the resources consumed in producing a product or delivering a service. It is performed in every case, regardless of whether there is a charge for the product or service.

Pricing establishes an appropriate charge. Pricing considers factors such as the following:

- the economic impact on stakeholders and the ability of clients to pay; and

- the degree to which a price may affect the achievement of public policy objectives.

Program delivery options

Costing is needed to answer questions related to program delivery options. For example:

- What is the difference in cost between a given outsourcing proposal and doing the work in-house?

- What are the estimated cost savings if this function is transformed into a shared departmental service?

- What is the total cost of a collaborative arrangement with a provincial government, and what is the cost to the federal government?

- What will the one-time and continuing cost savings be if a service is discontinued?

Step 1 — Cost purpose - How is the cost information to be used?

Determining the cost purpose is a prerequisite to costing. Unless one knows beforehand exactly how the resulting cost information will be used and why, it is impossible to determine the scope of the exercise and what costs are relevant to it.

As stated earlier, costing is tailored to the purpose for which the cost information will be used, whether for ad hoc or ongoing information needs. Before costs can be determined it is critical that all parties agree and understand exactly what decision the information will be used for. Once that is understood, the task of identifying exactly what information is needed may commence. A well-structured definition of the information needed will inform the scope of costs that are to be included in the costing and the degree of detail and rigour in cost assignment to be used.

Specifying a clear purpose is aided by determining which of the three general categories it falls into:

- Resources — focus is on resource levels corresponding to new, incremental, discontinuing, or cost-recovery activities;

- Performance measurement — focus is on measuring and evaluating performance;

- Program delivery options — focus is on alternatives and their relative cost impact.

Under each of these categories, there are numerous subcategories. It is therefore useful for departments to add to the purpose checklist, provided at the end of this step, to reflect particular departmental costing purposes.

Responsibility

The responsibility for complying with central agency costing information requirements rests with the DCFO. It is the joint responsibility of the DCFO and departmental management to determine the frequency and detail of departmental costing information requirements. The DCFO organization is responsible for ensuring that it understands the purposes for which the end-user requires cost information and provides advice, expertise, and appropriate support for the costing function. It is the responsibility of managers at all levels to be aware of decisions that affect costs and to assist in the development of methods of costing that provide better cost information to support such decisions.

Tasks

In defining the various costing purposes for a department, it is necessary to ensure a common understanding of the cost information needed to support decisions. The DCFO organization needs to work closely with the departmental stakeholders to develop a clear understanding of the purpose the information will serve.

Results

The result of the first phase of the costing process is a concise "user needs" statement that documents the purpose for which the costing information is needed. The user needs statement provides the following information:

- the specific decision that the costing is intended to support;

- the overarching assumptions used;

- in conceptual terms, the costing information required to support the decision, including the source or sources of the data to be used;

- the time period to be covered; and

- the frequency with which the information will be required.

This user needs statement is presented to the departmental end-user for review and approval prior to proceeding further. In the case of horizontal or other interdepartmental initiatives, the user needs statement should be developed in consultation and agreed to by all parties before proceeding.

Tips

Time and effort spent upfront in defining a clear purpose facilitates completion of the remaining steps.

Any subsequent change in the "purpose" statement requires revisiting each step.

Below is an example of a cost purpose template followed by a cost purpose checklist to which departments should add to meet their own needs.

Step 1 — Cost Purpose Template*

|

|

| |

|

This template helps to define a "purpose statement" that specifies exactly what cost information is needed, at what level of detail, and for what period of time. The resulting cost information should support the overarching decision, information need, or reporting requirement articulated in the purpose statement.

*This template is not meant to be all-inclusive — it covers only some of the more common costing purposes. Departments should add to this template, making it suitable for their particular circumstances.

Step 1 — Cost Purpose Checklist*

- What management decisions will be supported by the costing information? Please specify these decisions.

- What is the business issue or issues that triggered the need for cost information?

- Are there any central agency, legislative, or policy requirements that may affect the definition of the purpose or determination of the cost base? If yes, please describe these requirements. Did you take them into consideration? If not, please justify this decision.

- Who are the stakeholders in the costing project?

- What is the scope of the costing exercise? Please list the organizations involved (internal and external), the program activities, the program support services, and the specific IS activities involved.

- Are there any OGDs that will be affected by the initiative being costed, and have they been consulted?

- What is the time period to be covered by the costing exercise?

- What assumptions were made while defining the costing purpose? Have all assumptions been documented along with the supporting rationale?

- Does the defined purpose require information on incremental costs, full costs, or both?

- Is the cost information needed on a recurrent basis? If so, please specify the rate of recurrence.

- What are the deliverables? Please list and describe them along with the related timelines and recipients.

- Have all stakeholders been consulted in this step to define the purpose? If not, please explain why not.

- Has the defined purpose been confirmed by the ultimate end-user of the information?

- Have you documented the defined purpose?

Signature:

*Departments are encouraged to add to this checklist to satisfy their own needs.

Step 2 — Cost object

What is to be costed?

Cost objects are anything that needs to be costed, such as organizations, programs, outputs, or outcomes. Products and services are significant outputs because they are often the focus of performance measurement and other management decisions such as the setting of charges.

Cost purpose and cost objects are integral to each other. A cost purpose may include multiple cost objects; for example, the purpose of a costing exercise may be to compare the cost of IS consumed by each of the program branches (the cost objects) of a department. If there are six branches, there are six cost objects that have to be costed.

A checklist of appropriate cost objects is a useful road map for departments. It ensures the collection of all pertinent information at the level of detail required. Some typical categories of cost objects that may be included in checklists are the following:

- organization — such as a department and its units;

- programs — such as business lines, services, client groups, activities, and subactivities;

- processes — such as activities in the PAA;

- horizontal initiatives;

- IS — such as finance and HR;

- locations — such as HQ and other locations where there are departmental operations and services;

- infrastructure — such as buildings and departmental systems; and

- performance measurement units — such as outputs and outcomes.

Responsibility

It is the joint responsibility of program management and the DCFO organization to identify the appropriate cost objects for costing purposes. Program managers have the most knowledge about the nature of their programs and what needs to be costed. The DCFO organization provides advice and expertise to project managers on the most appropriate costing approaches and data sources. The relative involvement of representatives from each of these two groups will differ from department to department, depending on the division of responsibility and other influencing factors.

Tasks

The department's DCFO organization and program managers should clearly and completely define the cost objects to be costed.

In defining the purpose, the DCFO organization also reviews documents that provide key financial information (e.g. chart of accounts and monthly financial reports) and performance information.

Results

The result of this step is a clearly defined cost object consistent with the costing purpose.

There can be one or multiple cost objects for a single costing purpose.

Tips

Having a copy of the departmental PAA, organizational chart, and list of cost objects facilitates the discussions needed to complete Step 2.

Reference to these documents provides an opportunity for staff to gain insights into the structure of the department and components of the financial coding.

Following is an example of a cost object template followed by a cost object checklist that departments should supplement to meet their own needs.

Step 2 — Cost Object Template*

|

|

*This template is not meant to be all-inclusive and recognizes that terminology varies from department to department. Departments are encouraged to add to this template to meet their own needs.

Step 2 — Checklist for Defining the Cost Objects*

- Given the defined purpose, what are the cost objects (such as products, services, regional offices, processes, and program activities) to be costed? Please specify.

- Did you use the cost object template provided in Annex B?

- Did you consult with the various users of the cost information in order to define your cost objects?

- Have you reviewed the appropriate documents related to the defined purpose (such as PAA, RPP, user fee information, audit reports, and public accounts)?

- Does your choice of cost objects fully satisfy the defined purpose?

- Have the relevant stakeholders (internal and external) confirmed the defined cost objects?

- Have you documented your selection of cost objects?

Signature:

*Departments are encouraged to add to this checklist to satisfy their own needs.

Step 3 — Cost base

Which costs are relevant?

This step entails identifying all the costs that are relevant to the cost object or objects and the costing purpose. Determining which costs are relevant to the costing purpose and cost object or objects is necessary for accurate and reliable costing. It is often useful to consider all cost categories before deciding which ones are relevant, unless it is quite clear from the costing purpose that certain categories should be excluded.

Relevant costs are costs such as salaries and supplies that may originate in one's own budget and in the budgets of others, such as IS and OGDs.

Relevant costs commonly include the following:

- direct costs of the cost object;

- a share of the support costs of the program within which the cost object belongs; and

- a share of the IS costs that originate outside of the program.

Management Accounting Standard 2400-4 states that when various cost centres provide a significant level of services to themselves and to each other, the design of the costing system should reflect those interactions. Consequently, each category of IS costs that is allocated to a cost object should include its own direct costs as well as the indirect costs it has consumed. For example, the cost of the finance function would include the portion of HR and IT support costs it consumed.

Other costs that may be relevant, depending on the defined costing purpose and provided they are reasonably material, include the following:

- the costs of OGDs if the initiative is joint or horizontal;

- the costs of services provided at no charge by OGDs — estimates of costs provided by other departments at no charge can be obtained either in Part III of the Estimates or directly from the departments or agencies providing the services (e.g. accommodation provided by PWGSC; contributions covering the employer's share of employees' insurance premiums paid by the Secretariat (this excludes revolving funds); workers' compensation coverage provided by HRSDC; and legal services provided by JUS);

- the costs of centrally managed funds, principally the EBP payments that are made by the Treasury Board on behalf of federal government employees; and

- amortization costs for the capital assets used directly and indirectly in producing the outputs — for guidance on the valuation and amortization of physical assets, please review the Treasury Board Accounting Standards.

Another cost particular to revolving funds is the interest paid on the drawdown. The financing rate to apply should be the current Consolidated Revenue Fund lending rate that is published by the Department of Finance Canada.

It is important to consider all the circumstances before deciding on relevant costs. For example, if the incremental cost of a new service is being considered, the existing departmental infrastructure may have the capacity to support this service without incurring any new capital investment costs. In this case, capital is not a relevant cost.

To ensure that no relevant costs are overlooked it is important to develop a matrix or table that lays out all the possible relevant costs. A template of such a table follows on a subsequent page; it demonstrates the identification of relevant costs for several different purposes. Departments are encouraged to add to the template to meet their own needs.

Consultations should take place between the managers responsible for the cost objects being costed, appropriate members of the DCFO organization, and managers of those areas that generate the categories of costs being considered (i.e. the direct program managers, program support managers, and IS managers).