Guide to Advance Payments

1. Date of publication

This guide was published on November 22, 2019.

2. Application, purpose and scope

The purpose of this guide is to help departments meet the requirements for issuing advance payments, as set out in the Directive on Payments.

This guide provides details on the directive's requirements. It does not contain any additional requirements, but it does contain references to relevant legislative requirements. Examples are included for illustrative purposes and may not apply to all departments or situations.

Advance payments are the result of contractual requirements or an agreement. Chief financial officers should ensure that procurement officers:

- know the legislative and policy requirements

- are familiar with the guidance material on advance payments

The guidance in this document applies to advance payments for goods and services provided under various forms of contracts or agreements. Although the same concepts apply to advance transfer payments, refer to the Directive on Transfer Payments for the detailed requirements for advance transfer payments.

3. Definition of an advance payment

Advance payment: A payment made by or on behalf of Her Majesty before the work, delivery of the goods, or rendering of the service has been completed.

When is a payment an "advance payment"?

A payment is considered to be an advance payment only when it is issued before any goods have been received or before any services have been rendered. A payment made after partial completion of the work or when a specific milestone is met is considered a progress payment, not an advance payment.

Appendix A contains a decision tree for determining whether an advance payment is appropriate.

What is the difference between an early payment and an advance payment?

An early payment is a payment issued after the goods have been received or the services have been rendered but before the due date on the invoice.

What is the difference between a loan and an advance payment?

Even though an advance payment sometimes has similar characteristics to those of a loan, an advance payment is not a loan.

A loan is a financial asset of the government that is represented by a promise by a borrower to repay a specific amount, at a specified time or times, or on demand, usually with interest. In other words, a loan must be repaid. For details on loans, refer to the Directive on Public Money and Receivables.

An advance payment is a payment that is made by the government to a supplier in anticipation of the receipt of a good or a service. In short, when the government issues an advance payment to a supplier, the supplier is expected to eventually deliver a good or render a service. The supplier does not repay the amount of the advance payment.

What is the difference between an accountable advance and an advance payment?

An accountable advance is a sum of money advanced to a person from an appropriation for which the person is accountable. Accountable advances include travel advances, relocation advances, and the establishment of a change or petty cash fund. Only payments that meet the criteria set out in section 4 of the Accountable Advances Regulations qualify as accountable advances.

The main difference between an accountable advance and an advance payment is the source of the issuing authority. The authority to make an accountable advance derives from the Accountable Advances Regulations. The authority to make an advance payment derives from the terms of a contract or agreement.

The Chief financial officer and the departmental financial policy team can provide advice on whether an accountable advance or an advance payment is appropriate in a specific situation. Consultation with the department's legal services unit may also be required.

For details on accountable advances, refer to:

4. Fundamental principles

The requirements for advance payments set out in the Directive on Payments are based on two fundamental principles:

- advance payments are issued only in exceptional circumstances

- advance payments do not exceed the expected value of the goods or services to be received in that fiscal year

These principles are described in detail in Table 1.

| Fundamental principle | Key requirement | Rationale |

|---|---|---|

| Issued in exceptional circumstances only | Directive on Payments, subsection 4.1.1 Advance payments are to be made under exceptional circumstances only and when:

| Usually, the government pays for goods or services once the goods have been delivered or once the services have been provided. When it pays for goods or services after it has received them, it can better ensure that the agreement was respected and can better manage its cash needs. When the government pays in advance, it takes on greater risk and has fewer recourse options if the agreement is not respected. It also incurs additional financing and interest costs, and undertakes additional administrative burden. |

| Do not exceed the expected value of the goods and services received during that fiscal year | Directive on Payments, subsections 4.1.2.2 and 4.1.3 Advance payments in a given fiscal year relate to and do not exceed the reasonably expected value of the work performed or goods and services received during that year. Advance payment amounts that exceed the expected value of work performed or goods and services received during that fiscal year are to be recovered immediately. | Parliament appropriates funds annually to deliver programs to Canadians. Funds voted for a specific fiscal year are expected to be used for goods and services received in that same fiscal year. Departments cannot use advance payments to spend money that would otherwise lapse at the end of the year. |

4.1 Exceptional circumstances

Advance payments can be considered in exceptional circumstances only. Contractors are generally expected to finance their work from their reserves or through commercial financing based on the anticipated payments from the contracting authority for full or partial completion of the work.

“Exceptional circumstances” indicates that an advance payment is the least preferred method of payment for the Crown. The Crown’s standard approach is to issue payment after the receipt of goods or services. The advantages of paying at or after the receipt of goods or services, along with some of the risks of paying in advance, are outlined in Table 1.

Ultimately, an advance payment should be considered only when there is no other reasonable alternative. Before agreeing to an advance payment, departments should explore other possibilities. For example, they could seek out other suppliers that will accept payment after they have delivered the goods or services, or they could negotiate progress payments as specific milestones are met. For details on progress payments, refer to the Supply Manual, section 4.70.30.15.

Although the Crown's standard approach is to pay for goods and services after it has received them, in some industries or segments of industries, advance payments are an entrenched tradition or practice. For example, advance payments are the norm for subscriptions, flights and training. In cases where paying in advance is an entrenched tradition or practice, advance payments are acceptable, because no other reasonable alternative exists.

Documented in contract or agreement

Under subparagraph 34(1)(a)(ii) of the Financial Administration Act, if, under the terms of a contract, a payment is to be made before the completion of the work, delivery of the goods or rendering of the service, the appropriate minister, or another person authorized by that minister, should certify that the payment is in accordance with the contract. In other words, it is the contract that provides the legal basis for certifying the advance payment. An advance payment clause should therefore be documented in a contract or in an agreement.

A contract must contain an advance payment clause in order for a manager to exercise certification authority under section 34 of the Financial Administration Act before issuing the advance payment. Contracts or agreements that could contain advance payment clauses include the following (this list is not exhaustive):

- a goods or services contract

- a lease

- a training or conference registration form (online or paper format if the completed form constitutes a legally binding obligation)

- terms and conditions of an online purchase agreement (if the purchaser binds himself or herself to the terms and conditions once they have completed the transaction, for example by clicking on "I agree")

4.2 Fiscal year alignment of advance payments

In accordance with the principles of annual appropriations and the basis on which funds are appropriated by Parliament, advance payments in a particular fiscal year must relate to and cannot exceed the reasonably expected value of the work performed or goods and services received during that fiscal year. Specifically:

- advance payment clauses are not to be used to avoid lapsing funds at the end of the fiscal year or as a way to carry funds forward from one fiscal year to the next

- advance payments cannot be made in one fiscal year under a contract or agreement that does not start until the next fiscal year

- where advance payments are made for extraordinary start-up costs that a contractor expects to incur, the payment in each fiscal year cannot exceed the contractor's expenditure in that same fiscal year

If it is necessary to issue an advance payment in one fiscal year to cover the cost of goods or services to be received in a future fiscal year (for example, large fuel purchase made several years in advance of intended consumption), approval of exceptions to the Directive on Payments must be sought from the President of the Treasury Board. Refer to section 8 of this guide for details

Quick reference: advance payment essentials

- Use advance payments in exceptional circumstances only. Always plan to pay for goods and services after the goods have been delivered or after the services have been rendered. If payments are required before work has been completed, consider using progress payments first.

- Make sure that advance payments are documented in the contract or agreement so that managers can exercise certification authority under section 34 of the Financial Administration Act.

- Do not issue advance payments that exceed the expected value of goods or services to be received during the fiscal year, unless exceptions to the Directive on Payments have been granted.

- Never use advance payments to avoid lapsing funds at the end of a fiscal year or as a way to carry funds forward to a future fiscal year.

5. Advance payment clauses in contracts

The Contracting Policy provides details on considerations and requirements for including advance payment clauses in contracts. In particular, advance payment clauses must respect:

- the principles of parliamentary control, as set out in section 3.2 of The Parliamentary Financial Cycle

- the requirements of the Financial Administration Act

- the provisions of the appropriation acts themselves

- the requirements of the Directive on Payments

Before negotiating an advance payment clause and including it in a contract, a department should:

- make sure that it has a compelling business rationale for issuing an advance payment

- assess the risks associated with paying for the goods and services before it has received them (for example, viability of the supplier and risk of non-performance of the contract)

- consider the financing and interest costs to the Crown

- consider how any excess advance payment would be identified and how it would be recovered in cases where the advance payment exceeds the value of goods and services received in a fiscal year

In addition, contracting authorities should consider including advance payments in a contract only if:

- adequate security for the payment is ensured (in other words, means are in place to mitigate potential losses to the Crown. This could include mechanisms to recover or refund any advance payments made if the contract is not fulfilled.)

- the Crown receives value that is commensurate with the amount of the payment

- the department has adequate funds

- one of the following circumstances exists:

- the economic advantage to the Crown clearly outweighs the financing and interest costs associated with the advance payment

- the contractor would suffer hardship or could provide financing only with difficulty or at rates considered to be uneconomical in relation to prevailing chartered bank prime lending rates

- the value of the contract is considered to be beyond the contractor's assessed financial capabilities

- there is to be a long duration for contract performance

- the industry or segment of industry has an entrenched tradition or practice of receiving advance payments from the purchaser (for example, subscriptions, flights and training)

Remember, even if all the above conditions are met, advance payments are not necessarily warranted. Advance payments are to be issued in exceptional circumstances only. The Crown's preferred approach is always to issue payment after goods and services are received.

When determining the frequency of advance payments and the time frame for recovering excess advance payments, the objectives should be to:

- limit the Crown's exposure to risk

- minimize the financing costs

- minimize the gap between when the advance payment is issued and when the goods and services will be received

When an excess advance payment is identified, it must be recovered immediately or, if applicable, applied to the subsequent advance payment.

Quick reference: advance payment clauses

Address the following when negotiating and finalizing an advance payment clause in a contract or an agreement:

- Is there a compelling business rationale for paying in advance? What are the financing and interest costs to the Crown?

- What risks are associated with paying in advance? Is the supplier viable in the long term? Is there a risk of non-performance?

- How frequently should advance payments be issued? Are they aligned with the Crown's fiscal year? Will they be made close to when goods and services will be received? What are the risks to the Crown?

- How will excess advance payments be identified and recovered?

6. Advance payments to other government departments

The requirements in the Directive on Payments for advance payments for goods and services also apply to payments made under interdepartmental agreements.

Usually, the department that receives the goods or services pays the department that provides the goods or services once the goods have been delivered or the services have been rendered.

Advance payments:

- can be issued to other government departments only in exceptional circumstances

- must be documented in an interdepartmental agreement

- cannot exceed the expected value of goods and services to be received in that fiscal year

The agreement should include requirements for:

- regular reconciliations of the advance payment against the value of goods and services received

- any excess advance payments to be returned by the end of the fiscal year

Advance payments between departments apply only in situations where one department is providing goods or services to another department, which pays for them in advance. The deposit of funds into an OGD (other government department) suspense account is not an advance payment. OGD suspense accounts are used when a department is administering a program on behalf of another department. For details on OGD suspense accounts, refer to the Directive on Charging and Special Financial Authorities and the Guide to Internal Charging and Special Financial Authorities.

7. Authority to approve advance payments

Given the linkages between contracting and advance payments, chief financial officers should ensure that procurement officers are aware of the legislative and policy requirements and all associated guidance material on advance payments. Furthermore, departmental managers and procurement officers should consult with departmental subject matter experts on contracts and agreements that contain advance payment clauses.

7.1 Expenditure initiation and commitment authority

Expenditure initiation and commitment authority (section 32 of the Financial Administration Act) is exercised for advance payments in the same way it is for all other types of payments. The proposed expenditures should be reviewed against the unencumbered balance, and the commitment should be recorded in the department's financial system. Refer to the Guide to Delegating and Applying Spending and Financial Authorities for guidance on exercising spending and financial authorities.

7.2 Contracting authority

According to subsection 8(1) of the Government Contracts Regulations, any contracting authority (transaction authority) may enter into a contract that provides for making advance payments. In other words, as long as the contract provides for advance payments, the individual who has been delegated contracting authority can authorize an advance payment.

Treasury Board approval

According to subsection 8(2) of the Government Contracts Regulations, if Treasury Board approval is required for entry into a contract, the amounts and the times of the advance payments must also be approved by the Treasury Board.

In these cases, the Treasury Board submission seeking approval to enter into the contract must also seek Treasury Board approval of the amount and the times of any advance payments made under the contract:

- The proposal paragraph of the submission should reference a table in the submission that clearly identifies the amount(s) and the timing (the month and the year) of the advance payment(s).

- The rationale section of the submission should include the rationale for making an advance payment, as well as the proposed method and timing for recovering any excess advance payment(s).

7.3 Certification authority

Before certifying an advance payment for the provision of goods and services, the delegated manager should ensure that the contract or agreement contains the terms for such a payment. If there is no written contract or agreement, the delegated manager cannot provide certification under section 34 of the Financial Administration Act, which means that the advance payment cannot be issued. Refer to the Guide to Delegating and Applying Spending and Financial Authorities for guidance on exercising spending and financial authorities, including guidance on account verification and certification.

Quick reference: authority to approve advance payments

- Departmental managers, financial policy analysts and procurement officers should consult with each other when advance payment situations arise.

- Advance payments must be documented in a contract or agreement and approved by the appropriate authority:

- If the contract does not require Treasury Board approval, the timing and amounts of advance payments can be approved by the individual who has delegated contracting authority.

- If the contract requires Treasury Board approval, the timing and amounts of advance payments also require Treasury Board approval.

- For additional guidance on exercising spending and financial authorities, refer to the Guide to Delegating and Applying Spending and Financial Authorities.

8. Seeking approval of exceptions to issue multi-year advance payments

As stipulated in the Directive on Payments, advance payments in a given fiscal year must relate to and cannot exceed the reasonably expected value of the work performed or the goods and services received during that year.

Before issuing a multi-year advance payment, the department must obtain approval from the President of the Treasury Board for the following exceptions:

- exception to subsection 4.1.2.2 of the Directive on Payments to allow the department to make advance payments that exceed the goods or services reasonably expected to be received in that particular fiscal year

- exception to subsection 4.1.3 of the Directive on Payments to allow the department to recover any excess advance payments given to the contractor in the following fiscal year under the terms of the contract or agreement

With respect to multi-year contracts and agreements, every effort should be made to align the payment schedule with the government's fiscal year. If such alignment is not possible, approval of exceptions to the Directive on Payments is required.

A department's request for approval of exceptions to the Directive on Payments should clearly present the rationale for the exception. The request should indicate why the advance payment cannot be aligned with the government's fiscal year and what controls the department has put in place to limit the Crown's exposure to risk and make sure that any excess advance payment will be identified and recovered promptly.

Requests for approval of exceptions to the Directive on Payments to allow for multi-year advance payments should be limited to situations where the advance payment relates to and does not exceed the reasonably expected value of the work performed or the goods and services received in the following fiscal year. In other words, such requests should be made only in situations where the advance payment spans no more than two fiscal years. Although all requests for multi-year advance payments will be reviewed and considered, exceptions seeking to make a multi-year advance payment spanning more than two fiscal years generally present higher risks and should be avoided whenever possible.

9. Other considerations

9.1 How to account for advance payments

When accounting for an advance payment on a cash basis, the advance payment must be charged against the appropriation when it is issued.

When accounting for an advance payment on an accrual basis, the advance payment must be recorded as a prepayment and expensed when goods and services are received.

For detailed instructions on recording prepayments, refer to the Financial Information Strategy Accounting Manual, specifically, subsection 3.4, Prepayments (including Prepaids and Deferred Charges).

9.2 Tax considerations for advance payments

Paying for goods and services in advance can have an effect on taxes, such as the applicability and collection of taxes on advance payments. For details, refer to the Guide to Collecting and Paying Federal and Provincial Sales Taxes.

9.3 Other administrative details

Chief financial officers should ensure that controls are in place to monitor advance payments. Monitoring should include regular reconciliation of advance payments against the value of the goods or services received. Regular monitoring is critical to promptly recovering advance payment amounts that exceed the expected value of the work performed or the goods and services received during that fiscal year.

If a contractor does not deliver the goods or services for which an advance payment has been made, the manager, in consultation with the department's legal services unit, should review the terms and conditions of the contract and take the necessary action to recover the advance payment. According to the Government Contracts Regulations, paragraph 18(1)(e), every construction, goods or services contract is deemed to include a provision whereby if there is an act of default under the contract, the contractor agrees to immediately return any advance payment and agrees that the contracting authority may terminate the contract.

Refer to Appendix B for a process map that shows the steps involved in issuing an advance payment.

10. References

Legislation

- Accountable Advances Regulations

- Financial Administration Act, sections 2, 7, 26, 32 to 34, 37.1 and 38

- Government Contracts Regulations, sections 2, 8, 9 and 18

Related policy instruments

- Contracting Policy

- Directive on Charging and Special Financial Authorities

- Directive on Payments

- Directive on Public Money and Receivables

- Directive on Transfer Payments

- Financial Information Strategy Accounting Manual(subsection 3.4, Prepayments (including Prepaids and Deferred Charges)

- Guide to Delegating and Applying Spending and Financial Authorities

- Guide to Internal Charging and Special Financial Authorities

- Guideline on Accountable Advances

Supply Manual

Other relevant documents

11. Enquiries

Members of the public may contact Treasury Board of Canada Secretariat Public Enquiries if they have questions about this guide.

Individuals from departments should contact their departmental financial policy group if they have questions about this guide.

Individuals from the departmental financial policy group may contact Financial Management Enquiries for interpretation of this guide.

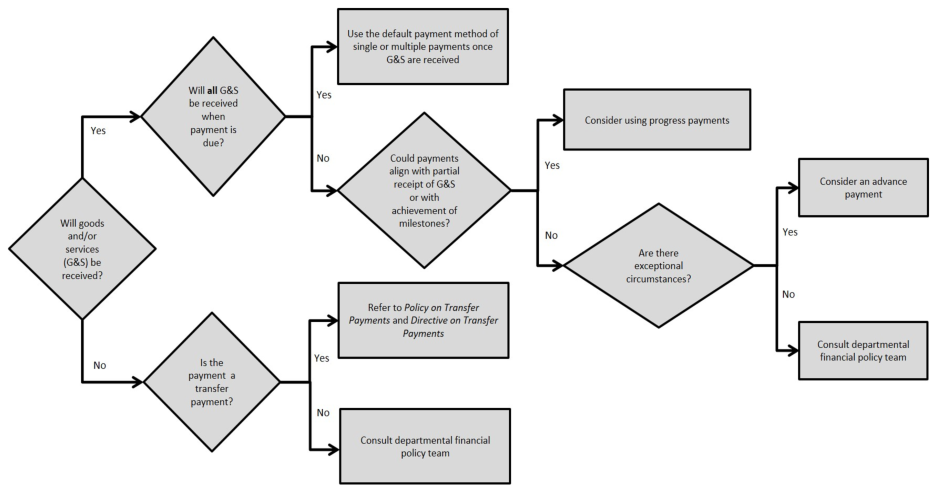

Appendix A: Decision tree

This decision tree is intended to help individuals determine which method of payment to include in a contract.

Figure 1 - Text version

A tree diagram showing the questions to ask to determine which method of payment to include in a contract

The first question is “Will goods and/or services (G&S) be received?”

If the answer to this question is yes, the next question is “Will all G&S be received when payment is due?”

- If all G&S will be received when payment is due, use the default payment method of single or multiple payments once G&S are received.

- If all G&S will not be received when payment is due, the next question is “Could payments align with partial receipt of G&S or with achievement of milestones?”

- If the answer to this question is yes, consider using progress payments.

- If the answer to this question is no, the next question is “Are there exceptional circumstances”?

- If there are exceptional circumstances, consider an advance payment.

- If there are not exceptional circumstances, consult your departmental financial policy team.

Returning to the initial question in the decision tree, “Will goods and/or services (G&S) be received?”, if the answer is no, the next question is “Is the payment a transfer payment?”

- If it is a transfer payment, refer to the Policy on Transfer Payments and the Directive on Transfer Payments.

- If it is not a transfer payment, consult your departmental financial policy team.

Reminder

An advance payment must be made only under exceptional circumstances when the payment is considered essential to achieving program objectives and when no other reasonable alternative exists. Advance payments are not to be used to avoid lapsing funds at the end of a fiscal year or as a way to carry funds forward from one fiscal year to the next.

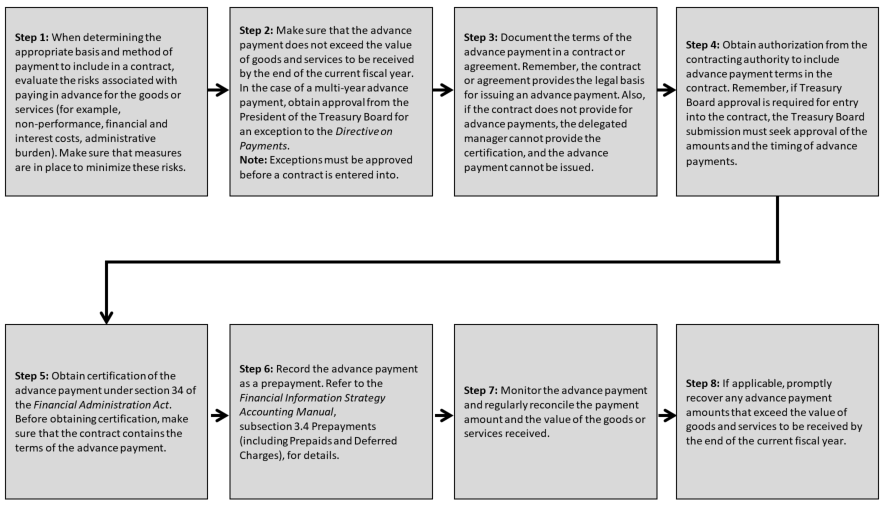

Appendix B: Process map

This process map is intended to help departmental managers, procurement officers, financial officers and financial policy teams when considering including provisions for advance payments in a contract or when issuing an advance payment.

Figure 2 - Text version

The figure shows the steps to follow when considering including provisions for advance payments in a contract or when issuing an advance payment.

Step 1: When determining the appropriate basis and method of payment to include in a contract, evaluate the risks associated with paying in advance for the goods or services (for example, non-performance, financial and interest costs, administrative burden). Make sure that measures are in place to minimize these risks.

Step 2: Make sure that the advance payment does not exceed the value of goods and services to be received by the end of the current fiscal year. In the case of a multi-year advance payment, obtain approval from the President of the Treasury Board for an exception to the Directive on Payments.

Note: Exceptions must be approved before a contract is entered into.

Step 3: Document the terms of the advance payment in a contract or agreement. Remember, the contract or agreement provides the legal basis for issuing an advance payment. Also, if the contract does not provide for advance payments, the delegated manager cannot provide the certification, and the advance payment cannot be issued.

Step 4: Obtain authorization from the contracting authority to include advance payment terms in the contract. Remember, if Treasury Board approval is required for entry into the contract, the Treasury Board submission must seek approval of the amounts and the timing of advance payments.

Step 5: Obtain certification of the advance payment under section 34 of the Financial Administration Act. Before obtaining certification, make sure that the contract contains the terms of the advance payment.

Step 6: Record the advance payment as a prepayment. Refer to the Financial Information Strategy Accounting Manual, subsection 3.4 Prepayments (including Prepaids and Deferred Charges), for details.

Step 7: Monitor the advance payment and regularly reconcile the payment amount and the value of the goods or services received.

Step 8: If applicable, promptly recover any advance payment amounts that exceed the value of goods and services to be received by the end of the current fiscal year.